Axios Pro Exclusive Content

"Lithium, nickel ... cobalt do not just magically appear"

Nov 1, 2022

Stop us if you've heard this before: Geopolitical turmoil, supply chain disruptions, inflation and breakneck demand for batteries are threatening to undercut the transition to electric-everything.

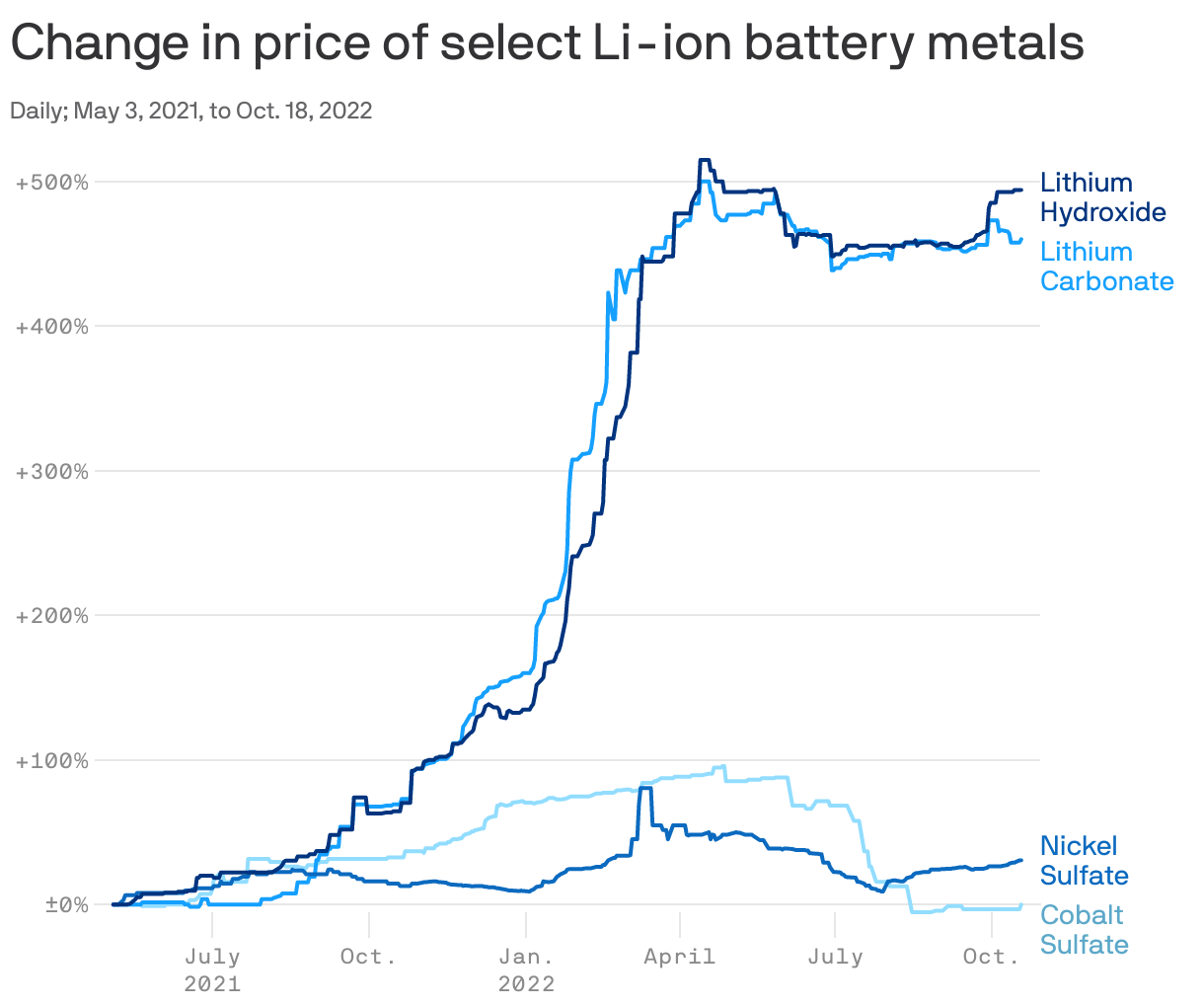

Why it matters: A new report from S&P Global Mobility puts hard numbers on how the upheaval is affecting investment — specifically soaring prices that aren't expected to subside any time soon.