Axios Pro Rata

September 18, 2021

It's mid-September already — and I'm still trying to work out whether the summer of last year actually happened...

- As always, feel free to send me tips or comments by replying to this email or on Twitter @imkialikethecar.

- Playing on my Spotify: a whole lot of Doja Cat (mainly her newest album, "Planet Her").

Today’s Smart Brevity™ count is 1,158 words, a 4-minute read.

1 big thing: Income-sharing agreements on a quest for legitimacy

Illustration: Annelise Capossela/Axios

Income-sharing agreements (ISAs) were hatched more than 60 years ago by Milton Friedman, but the financing instrument is still trying to establish its legitimacy.

Why it matters: ISAs, which let borrowers get cash upfront and repay it later via a portion of their future earnings, have been hailed as a solution to the college debt crisis.

- Proponents argue that ISAs not only better align incentives between the schools and the students, but also help graduates avoid crushing debt if their degrees don’t lead them to lucrative careers.

- Critics, however, say they lack the proper protection for borrowers and can lead to unfair repayment burdens.

Driving the news: Two organizations that issue and manage ISAs recently moved to comply with lending regulators, emphasizing their actions as a positive step for the industry.

- Earlier this month, nonprofit Better Future Forward entered into a consent decree with the Consumer Financial Protection Bureau to settle charges that it had violated various lending laws, and agreed to make certain changes to its practices.

- In August, Meratas was granted a conditional license by the California Department of Financial Protection and Innovation to manage ISAs in the state, the first such license granted by the agency.

What they’re saying: "We don’t agree with their findings, but we really think the [CFPB] is the right entity to regulate this, and we think it’s important to work with them," Better Future Forward founder and CEO Kevin James tells Axios.

How it works: "Coding bootcamps"— programs that aim to teach basic computer programming skills to students — have embraced ISAs.

- Many say that ISAs make their programs accessible to students without the means to pay upfront while acting as an incentive for schools to ensure that graduates are professionally successful.

- Some colleges, like Purdue University, have also begun to offer ISAs as an alternative to traditional loans.

Yes, but: ISAs still operate in a regulatory gray area.

- Laws governing lending (like the Truth in Lending Act) generally don’t discuss ISAs specifically, leaving companies and regulators to interpret how they apply.

- This leads to disagreements. For example, while the CFPB deemed Better Future Forward’s ISAs to be loans, the organization views them as a distinct type of legal obligation. Still, James says he is eager to work with the CFPB on applying its lending disclosure requirements to ISAs going forward.

- State and federal lawmakers have introduced various bills, but there has been little further action.

Moreover, ISAs have been criticized for being predatory and locking borrowers into repaying unfair portions of their earnings.

- "It was hard for the consumer to really know if it was a good deal or a bad deal," Upstart co-founder Paul Gu tells Axios. His company was initially a marketplace for ISAs before pivoting to traditional loans.

- This is due in part to the fact that borrowers can't predict their exact future earnings and whether they'll end up "overpaying" if they're highly successful.

The bottom line: With the interest in ISAs not going away, lawmakers and regulators won't be able to ignore them for much longer.

2. The trouble with coding bootcamps

Illustration: Sarah Grillo/Axios

ISAs have become most popular as a way to finance "coding bootcamps," but they’ve also added to the criticisms faced by some of the educational programs.

What’s happening: In July, a group of former students of San Francisco-based Make School filed a lawsuit against the company, accusing it of misleading them about the true amount they’ll repay, and making them sign multiple ISAs.

- The students are also suing Vemo, the administrator of their Make School ISAs. A Vemo spokesperson told Axios: "We are committed to ensuring that all students have the most transparent and reliable information on ways to finance their postsecondary education pathway."

- Make School has since transferred its assets to a nonprofit.

The big picture: Coding bootcamp issues aren't limited to their use of ISAs.

- Make School has been fined by the California Bureau of Private Postsecondary Education for not having the required approval to operate, as have a number of other programs, including Lambda School. ISAs have been part of the licensing problem (they're not allowed by the agency).

- A number of the early coding programs also ran afoul of the BPPE back in 2014.

- These programs are also often criticized for overpromising when it comes to the jobs and careers their graduates can expect, the quality of the instruction (many hire their own alumni to teach), and for targeting prospective students from low-income backgrounds with unrealistic promises.

Author’s note: Before working as a reporter, I spent about seven months in 2013-2014 working in the General Assembly’s San Francisco office, which offered coding programs (though it didn’t use ISAs).

3. A timeline of education finance disruption

Illustration: Shoshana Gordon/Axios

Milton Friedman: The famed economist first described the income-sharing agreement in his 1955 essay "The Role of Government in Education":

- "Such a program would eliminate existing imperfections in the capital market and so widen the opportunity of individuals to make productive investments in themselves while at the same time assuring that the costs are borne by those who benefit most directly rather than by the population at large."

Yale: In the 1970s, the Ivy League university tested a modified version of ISAs, in part designed by Nobel Prize-winning economist James Tobin, in which students in a cohort would collectively pay back a portion of their earnings to pay off the group's entire balance.

- It left some students frustrated that they were paying more than their fair share to make up for peers who couldn’t make the payments.

Upstart: Founded in 2012, the San Francisco-based company started out as a marketplace for ISAs, matching investors with young people seeking upfront cash to finance their professional ambitions.

- After three years, the company shifted to traditional loans, with co-founder Paul Gu telling Axios that ISAs turned out to be harder to explain to customers than initial buzz and media attention suggested.

Personal IPOs: As far back as 2008, individuals have been experimenting with "selling shares" of themselves and their future earnings, similar to an initial public offering.

- Even companies like HumanIPO have cropped up to enable this idea.

Income insurance pools: Companies like Pando Pooling, founded in 2017 by Stanford University alumni, have garnered buzz for letting baseball players pool their future earnings as insurance in case they don’t make it big.

- The idea is spreading to other groups of professionals like MBA students, where, again, it’s unclear early on who in the cohort will strike it rich.

📚 Due Diligence

- The Future of Investing Directly In People (The Information)

- Meet the Man Who Sold His Fate to Investors at $1 a Share (Wired)

- Because You’re Worth It (Slate)

- Lifting the Curtain on Income-Share Agreements (Insider Higher Ed)

🧩 Trivia

While Yale's ISA experiment was discontinued in 1978, the repayment obligations continued much longer.

- Question: What year did the whole thing finally end?

(Answer at the bottom.)

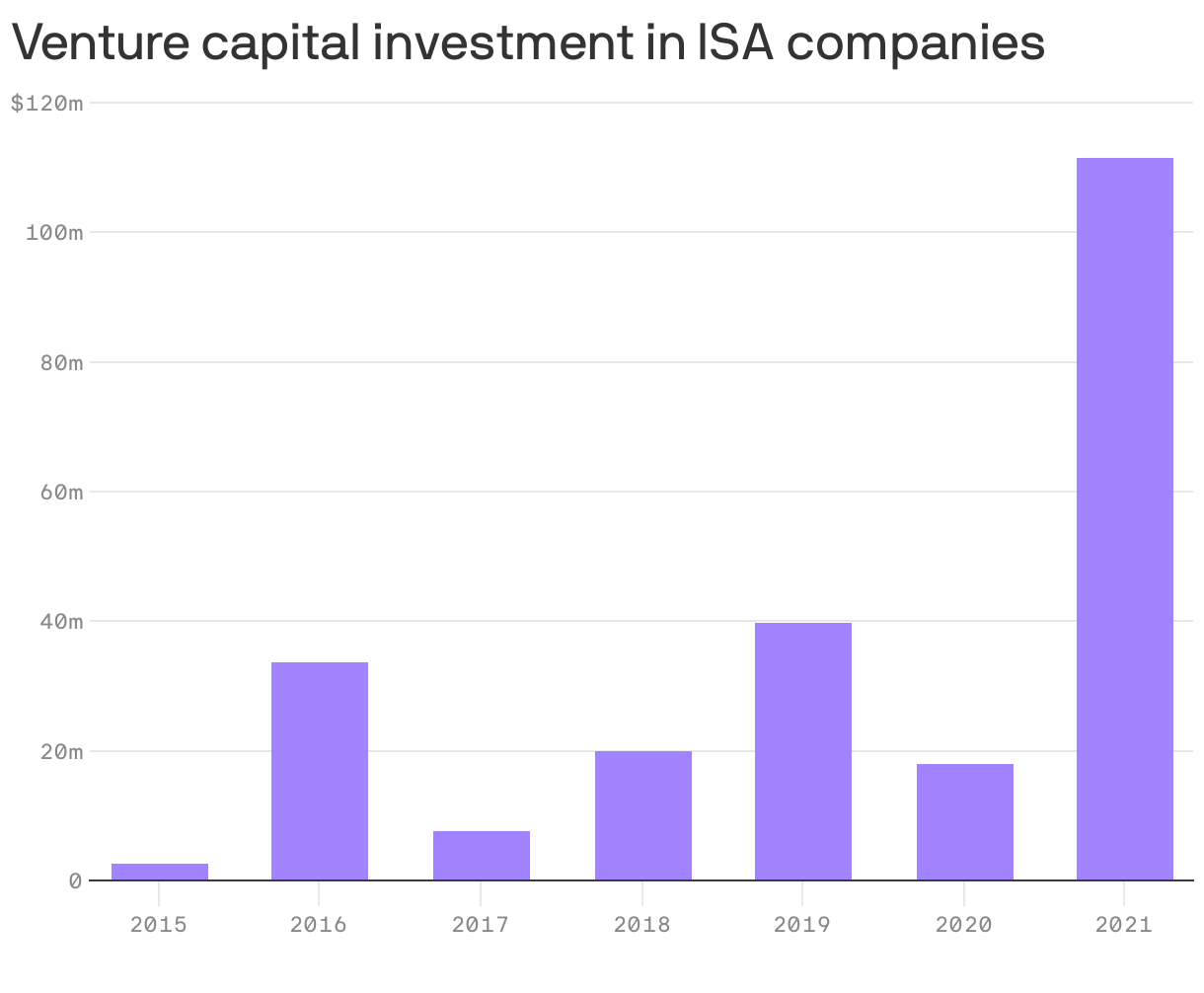

🧮 Final Numbers

🙏 Thanks for reading! See you on Monday for Axios Pro Rata's weekday programming, and please ask your friends, colleagues and lenders to sign up.

Trivia answer: 2001.

Sign up for Axios Pro Rata

Dan Primack’s briefing on VC, PE & M&A for dealmakers.