Axios Pro Rata

July 13, 2024

1 big thing: Alternative assets ❤️ ESG

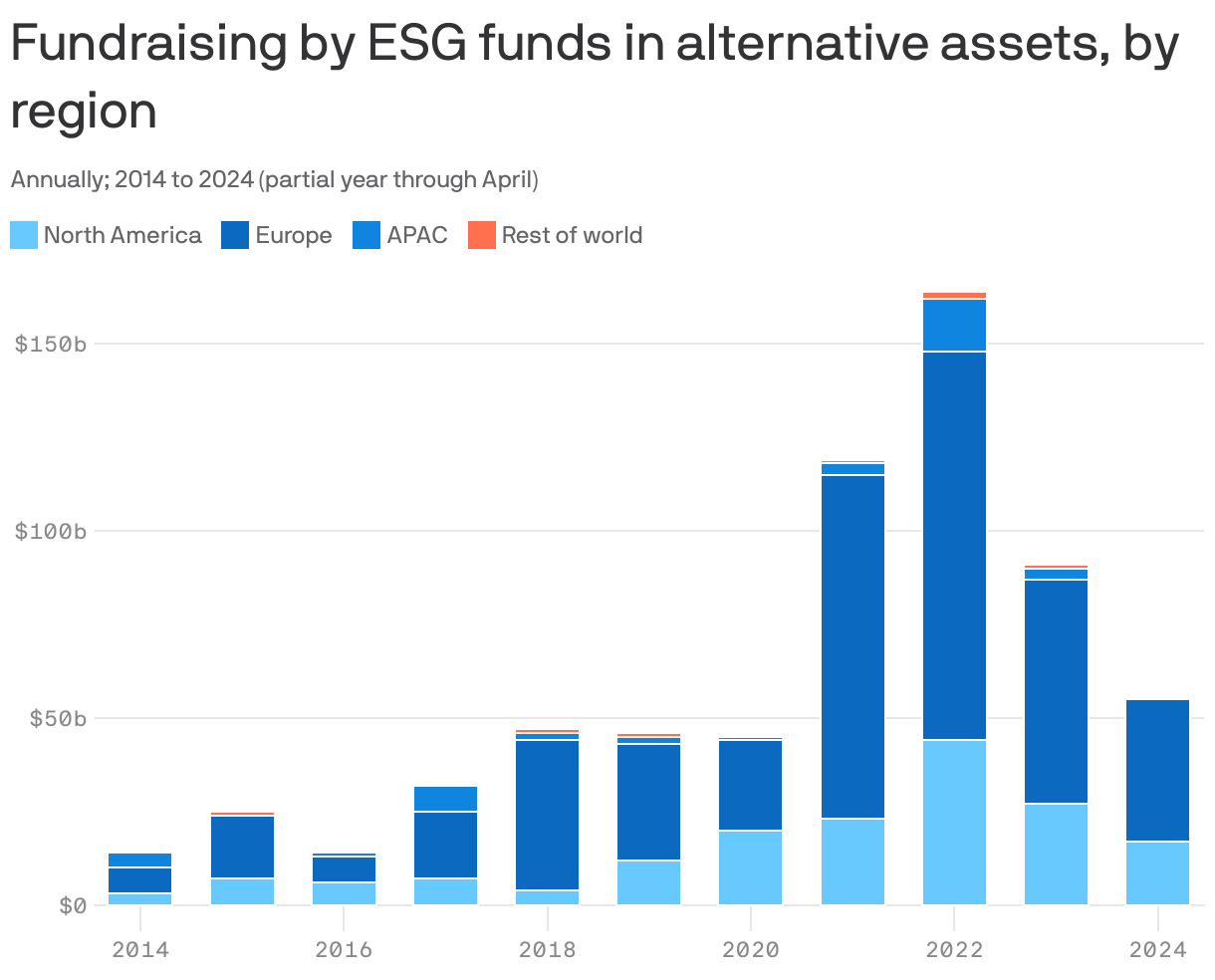

ESG funds in alternative assets have raised $55 billion as of April, on pace with 2022's record of $163 billion, per Preqin data.

Why it matters: ESG-focused initiatives across the business world tend to be de-emphasized amid downturns or lessened pressure to support them.

By the numbers: ESG in alternative assets had a notable growth spurt beginning in 2021 — with a total of $282 billion raised in 2021 and 2022 across 528 funds, compared with $226 billion raised by 629 funds in total over the previous seven years.

- And although 2023 totals dropped below $100 billion, fundraising levels were still higher than before 2021.

Zoom in: ESG funds made up 21% of all private capital raised this year as of April.

- As of April, European limited partners make up 44% of all impact investors and 43% of all climate investors, while North American LPs represent 33% and 41%, respectively.

- Infrastructure and private equity dominate ESG fundraising, with the former also dominating assets under management and the funds currently in market.

- This year, climate-focused funds have pulled ahead of impact funds both in terms of number of funds raised and total capital raised.

- Established managers dominate fundraising, although first-time managers have gained some ground since taking only 7% of capital in 2021.

The intrigue: ESG remains a divisive topic in the investment world, with skeptics questioning whether the sector can generate returns on par with their peers (see final numbers).

Between the lines: Despite the controversies, ESG remains a significant factor for investors.

- In a June survey by Preqin, 24% of 67 respondents said they have turned down otherwise attractive opportunities because of ESG standards, 36% said they would, and 40% said they have not.

Yes, but: ESG consideration is not uniform across all alternative assets.

- 50% of infrastructure investors reported having an ESG policy, as did 45% of private equity investors, 19% of hedge funds, and 14% of venture capitalists, to name a few from the survey's results.

The bottom line: ESG investing is subject to investors' whims, but it's nevertheless becoming more entrenched in alternative assets.

2. Early-stage exits

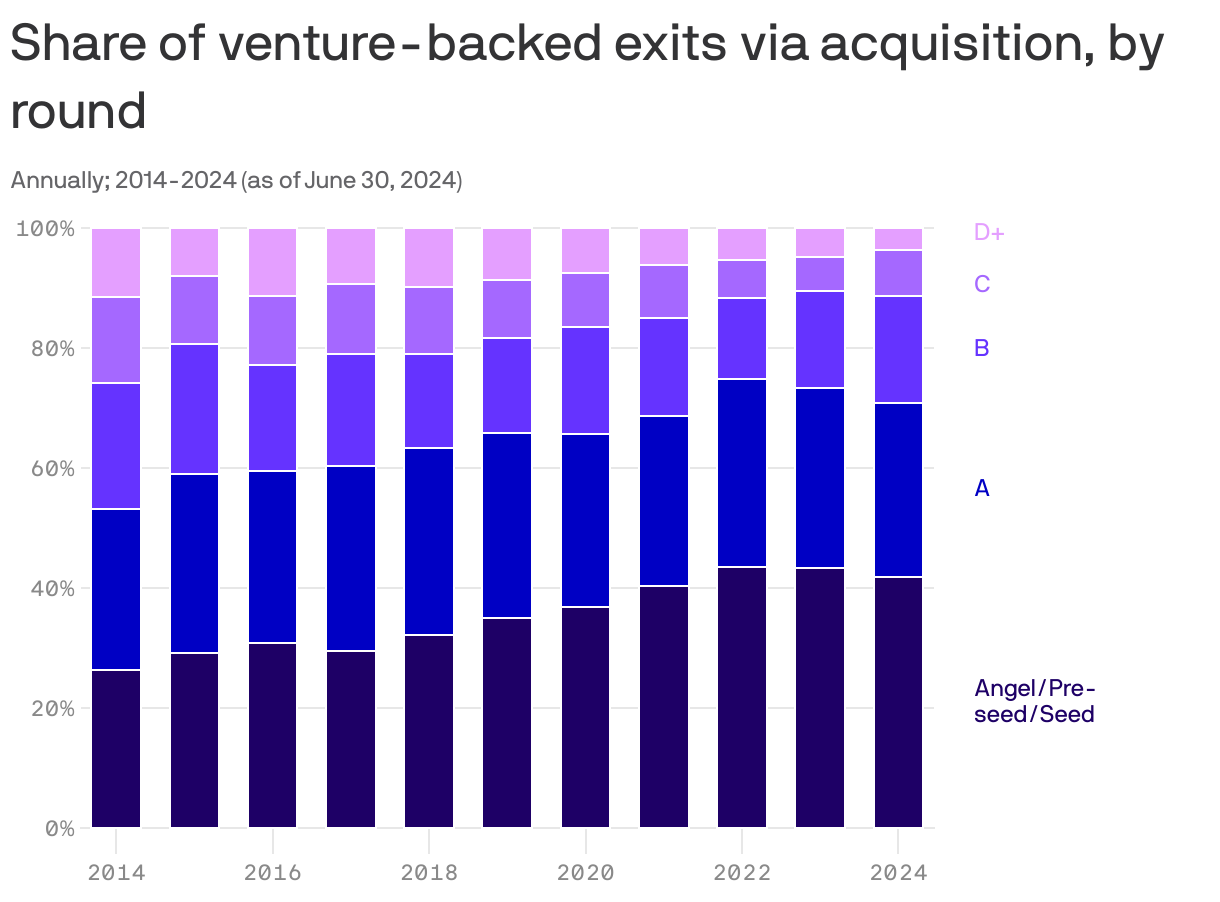

Most acquisitions of U.S. venture-backed companies so far in 2024 have been of early-stage startups, according to PitchBook.

Why it matters: Small startup M&A is taking over amid tepid IPO activity and persistent challenges in acquiring late-stage companies

By the numbers: In the first two quarters of this year, acquisitions of startups at the pre-seed, seed, and Series A stages accounted for just over 70% of all M&A.

Yes, but: As PitchBook notes, this M&A activity is providing "little relief to VC."

- Acquisitions of venture-backed companies have netted only $19.4 billion so far this year — short of the levels during the pandemic's boom times, and nowhere near the public listing values of recent years.

Between the lines: "It's not just large M&A that has disappeared; it is also middle market add-ons that would provide a decent return to recycle capital back to LPs," notes PitchBook.

- PitchBook posits that it's due to the relatively strong valuations taking pressure off the best companies to exit, leaving only the weaker businesses, and hesitation by public companies to make acquisitions that would be harder to explain to investors.

3. Zoom in: AI venture investing

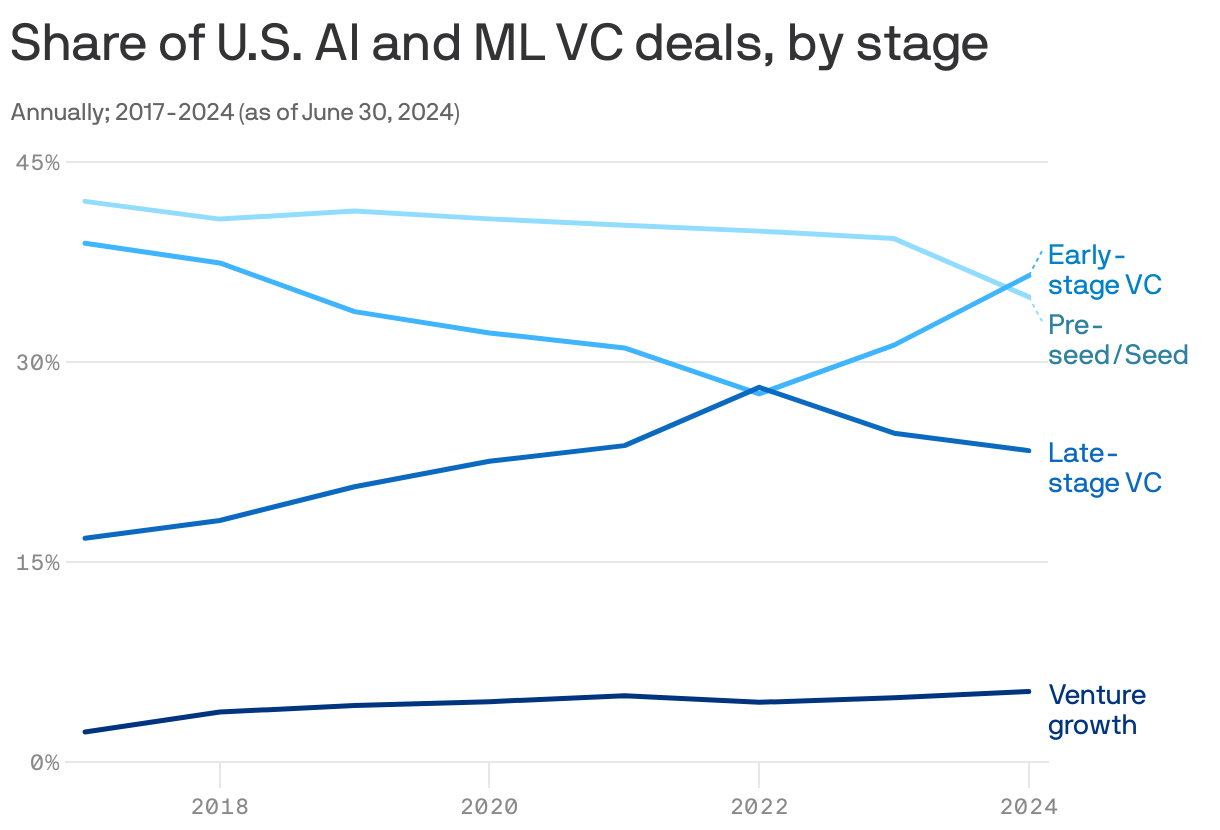

VCs are increasingly more interested in early-stage startups led by AI researchers than in companies that were born before the generative AI boom, according to PitchBook.

Why it matters: "Doing AI before it was cool" may not be as persuasive an argument to VCs.

By the numbers: Early-stage deals have accounted so far in 2024 for 36.5% of all AI & machine learning VC deals, up from just over 31% last year. It's now the biggest category.

Between the lines: The shift in investment activity is likely driven by multiple factors, including the growing number of researchers leaving established AI companies and Big Tech, VCs' preference for investing earlier at lower valuations, and their desire to write checks for the latest AI tech.

📚 Due Diligence

🧩 Trivia

🧮 Final Numbers

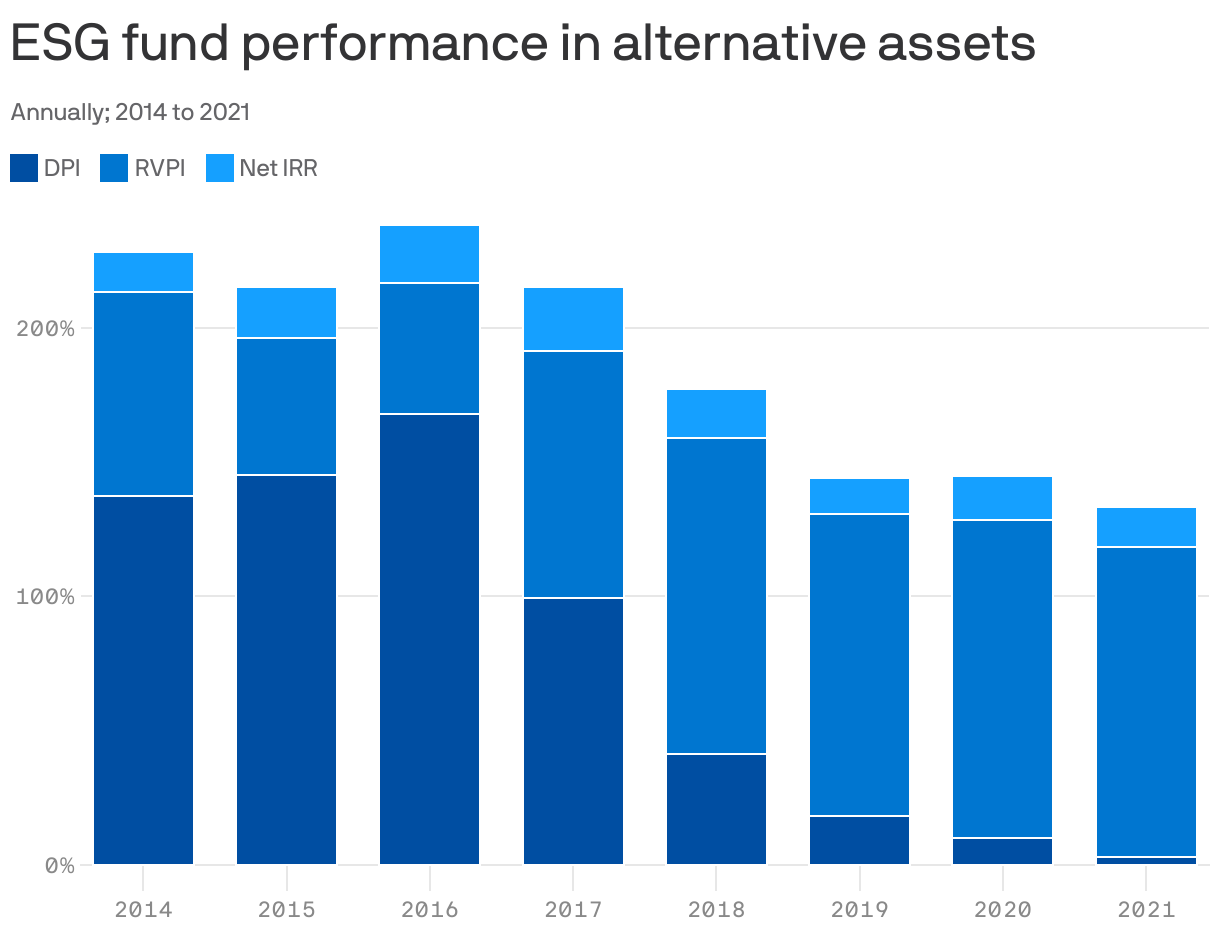

Whether ESG-focused investments can produce great returns remains a hotly debated question, but a recent analysis of alternative assets by Preqin suggests they can.

By the numbers: The mean internal rate of return (IRR) for ESG funds is 13.5% and the median IRR is 12%, compared with a mean of 15% and median of 12.3% for non-ESG funds.

Yes, but: There are some caveats, namely that Preqin analyzed more than 10,000 non-ESG funds, but only 215 ESG funds.

- ESG funds also tend to be much younger, putting them at a disadvantage given the longer-term nature of alternative assets.

The bottom line: Take the above with a big grain of salt, though it's still a notable data point to consider in the debate over ESG's investment merits.

Axios Pro Rata

Dan Primack’s briefing on VC, PE & M&A for dealmakers.