Axios Markets

August 26, 2023

1 big thing: The problem with homeownership

Illustration: Aïda Amer/Axios

2. The downsides of financialization

Illustration: Aïda Amer/Axios

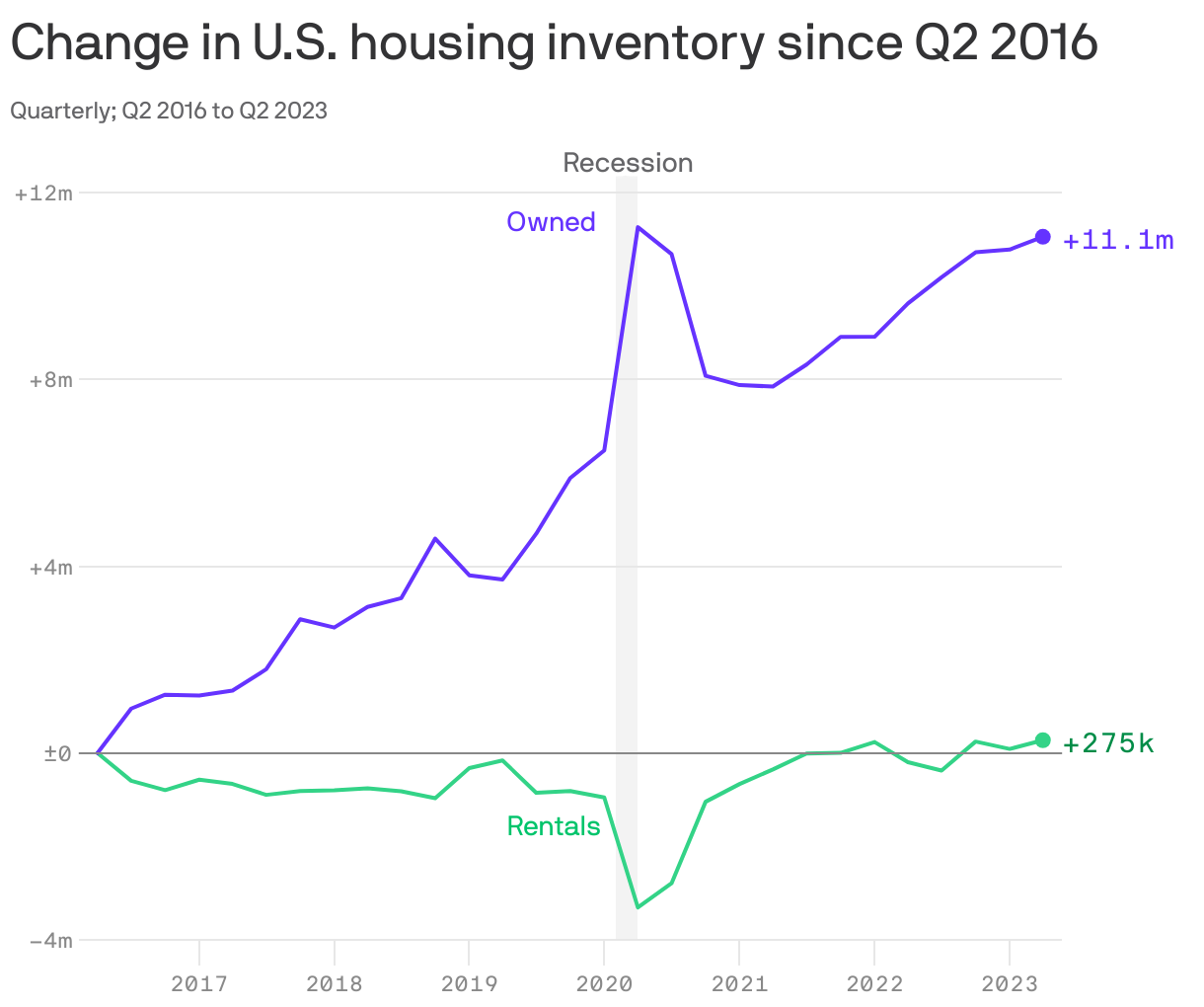

3. The rental stagnation

Over the past 7 years, the total number of renter-occupied housing units in America has increased by just 275,000, per the Census Bureau.

- Meanwhile, the number of owner-occupied housing units has increased by 11,055,000.

4. A record-setting IPO

Landing a prestigious (and lucrative) underwriting mandate on a big IPO is the kind of thing that equity capital markets bankers live for.

- In the case of the IPO of chipmaker Arm, however, the honor is being shared among a record 28 different banks.

What they're saying: "Equity underwriting — a sexy, 'franchise' part of investment banking — has become commoditized," writes former ECM banker Craig Coben.

- Increasingly, coveted IPO mandates just go to whichever bank has been lending the most money to the company in question.

- After all, says Coben, big institutional investors "don't care who the underwriters are."

5. Building of the week: Maestro pavilion, Shanghai

Photo: Reed Photographic

Axios Markets

Stay on top of the latest market trends and economic insights