Axios Markets

October 28, 2021

1 big thing: Why it's so hard to tax wealth

Illustration: Sarah Grillo/Axios

2. Catch up quick

3. Hertz's fight for relevance

A Hertz car rental counter in the Miami International Airport. Photo: Joe Raedle/Getty Images

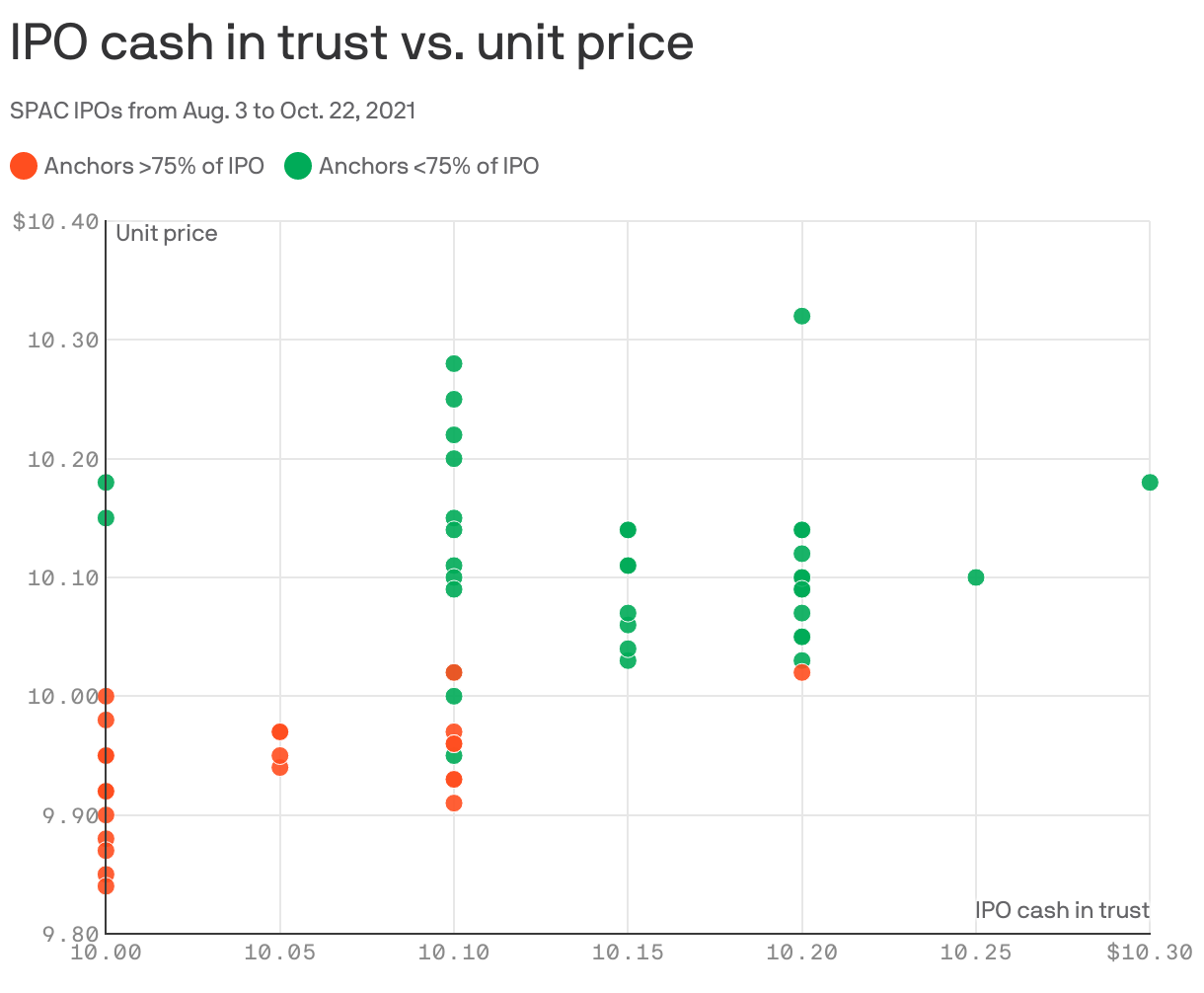

4. Anchors weigh down SPACs

Special purpose acquisition companies (SPACs) have increasingly turned to anchor investors to pull off IPOs — but it appears these backers tend to dump the stock soon after the offerings, Axios’ Kia Kokalitcheva writes.

Driving the news: Deals in which at least 75% of the capital came from anchors have underperformed those in which anchors made up less than 25%, according to SPAC Research.

Context: As we noted in September, one byproduct of a weakened demand for SPAC IPOs among investors has been the uptick in anchors, who make early commitments to buy large chunks of the IPO.

- Sponsors often offer anchors more favorable terms, like the opportunity to receive founder shares.

- The trend has some investors worried that it may be a sign of low-quality SPACs that need expensive sweeteners.

The bottom line: Anchors may be getting sweet deal terms, but it's not enough to hold on.

5. Companies are still loading up on equipment

The willingness of businesses to invest in themselves shows no sign of slowing.

Driving the news: Core capital goods orders rose 0.8% in September, beating economist expectations for growth of around 0.4%, government data out yesterday show.

Why it matters: It's a key measure of business spending on equipment, and strength here shows companies' willingness to invest in the future.

- September's rise is the biggest monthly increase since June.

The bottom line: The latest release “is consistent with our view that business capex will be much stronger over the next few years than during the previous economic cycle, boosting productivity growth,” Ian Shepherdson, chief economist at Pantheon Macroeconomics, wrote in a research note.

Axios Markets

Stay on top of the latest market trends and economic insights