Axios Markets

June 24, 2021

1 big thing: The "coiled spring" economy

Economic growth could be hot for much longer than expected as shortages continue to push out the unsatisfied demand for goods and services, writes Axios Markets correspondent Sam Ro.

Why it matters: The current blistering pace of growth has been spurred by the rapid reopening of the economy, a phenomenon some experts say can't last.

Yes, but: Economists tell Axios that while growth may slow, it’ll still be unusually strong for a while because so many people and businesses are holding off on purchases — either because stuff isn’t available or prices are just too high.

What they’re saying: BofA economist Ethan Harris says the U.S. economy is like "a coiled spring."

- "This is good news for the period ahead," Harris wrote in a report. "While a lot has been made of the temporary inflation pressures, there is much less discussion of the temporary constraint on real activity. However, you can't have one without the other."

- "There are only so many people that can go to Disney World in a given day," Renaissance Macro economist Neil Dutta tells Axios. Yes, even the happiest place on earth is turning people away.

By the numbers: Dutta says we should look at vendor lead times, or the amount of time it’s taking to deliver goods, to gauge just how backed up companies are with orders they can't fill right away.

- Average supplier delivery times have lengthened to record levels, according to a Markit PMI report released Wednesday. This data goes back to 2007.

- This confirms similar findings from the May ISM manufacturing report, which has data going back to 1987.

- Arbor Data Science’s Ben Breitholtz analyzed regional Fed surveys and concluded supplier delivery times may be at their highest level since 1951.

Also: Harris and SGH Macro Advisors economist Tim Duy argue the surge in job openings clearly represents unfulfilled demand.

- "In the last two months 837,000 people have been added to payrolls, but the number of job openings has jumped by 1.76 million," writes Harris in an email to Axios. "Unsatisfied new demand for workers is growing more than twice as fast as hiring!"

The bottom line: For months we’re going to keep getting reports that’ll underestimate the full strength of America’s consumers and businesses.

- "Effectively, as the economy hits more supply side constraints, our metrics of growth soften," says Duy. "But it shouldn’t be confused with a typical demand side slowdown."

2. Catch up quick

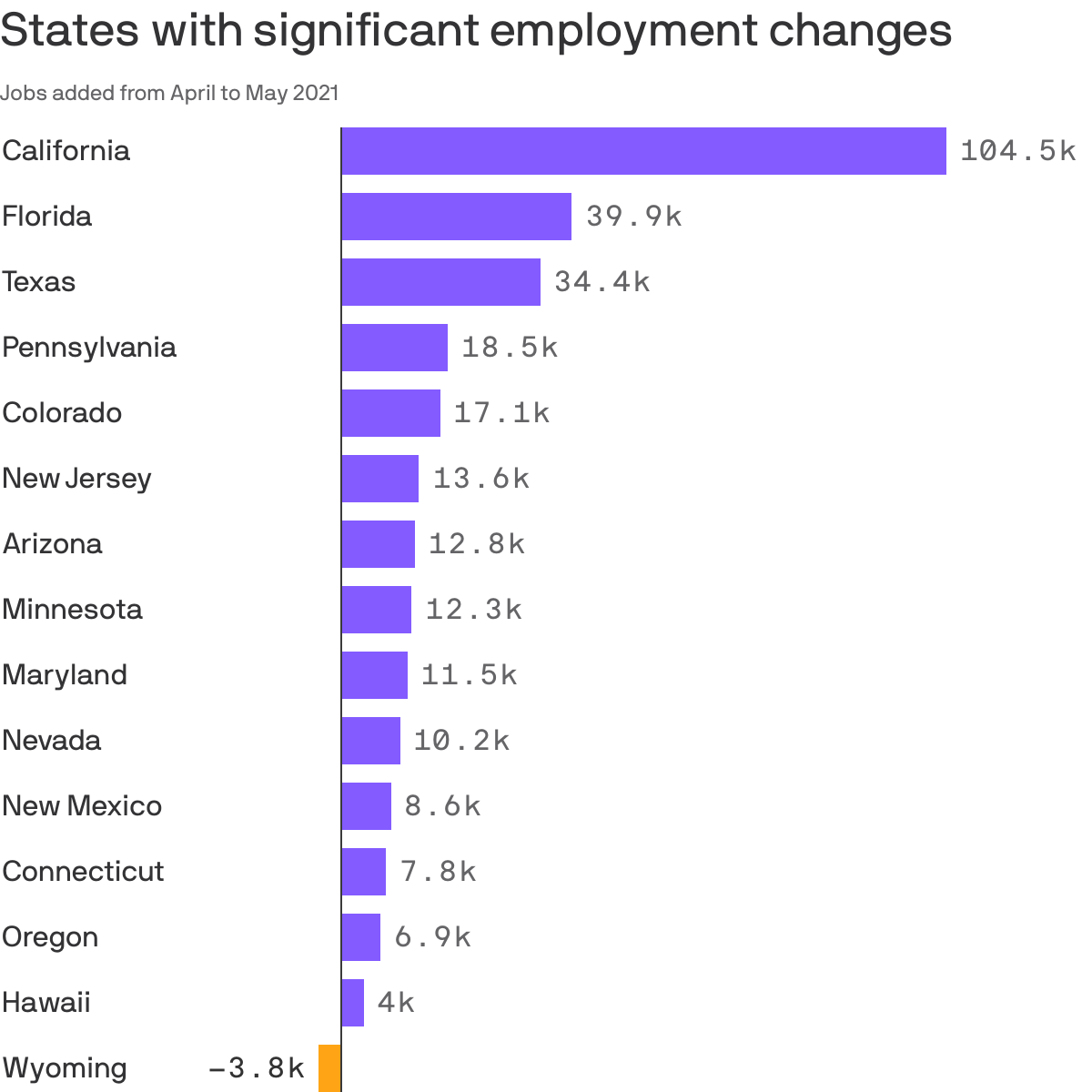

3. Employment increased in just 14 states in May

The challenge of finding qualified workers to fill open jobs is illustrated by the fact that just over a quarter of states saw employment increase in May, writes Sam.

Why it matters: The closely watched national employment report released on June 4 — which showed U.S. employers added 559,000 jobs in May — does not capture how uneven the labor market recovery has been.

By the numbers: According to new data dropped by the Bureau of Labor Statistics on Wednesday, just 14 states reported a statistically significant increase in jobs during the period.

- Wyoming was the only state to shed jobs in May.

Be smart: A lack of job creation would be much worse if it were the result of a lack of demand for workers. But all signs suggest demand is strong and it’s the supply of labor that’s lagging.

4. The floating rate debt play

Illustration: Aïda Amer/Axios

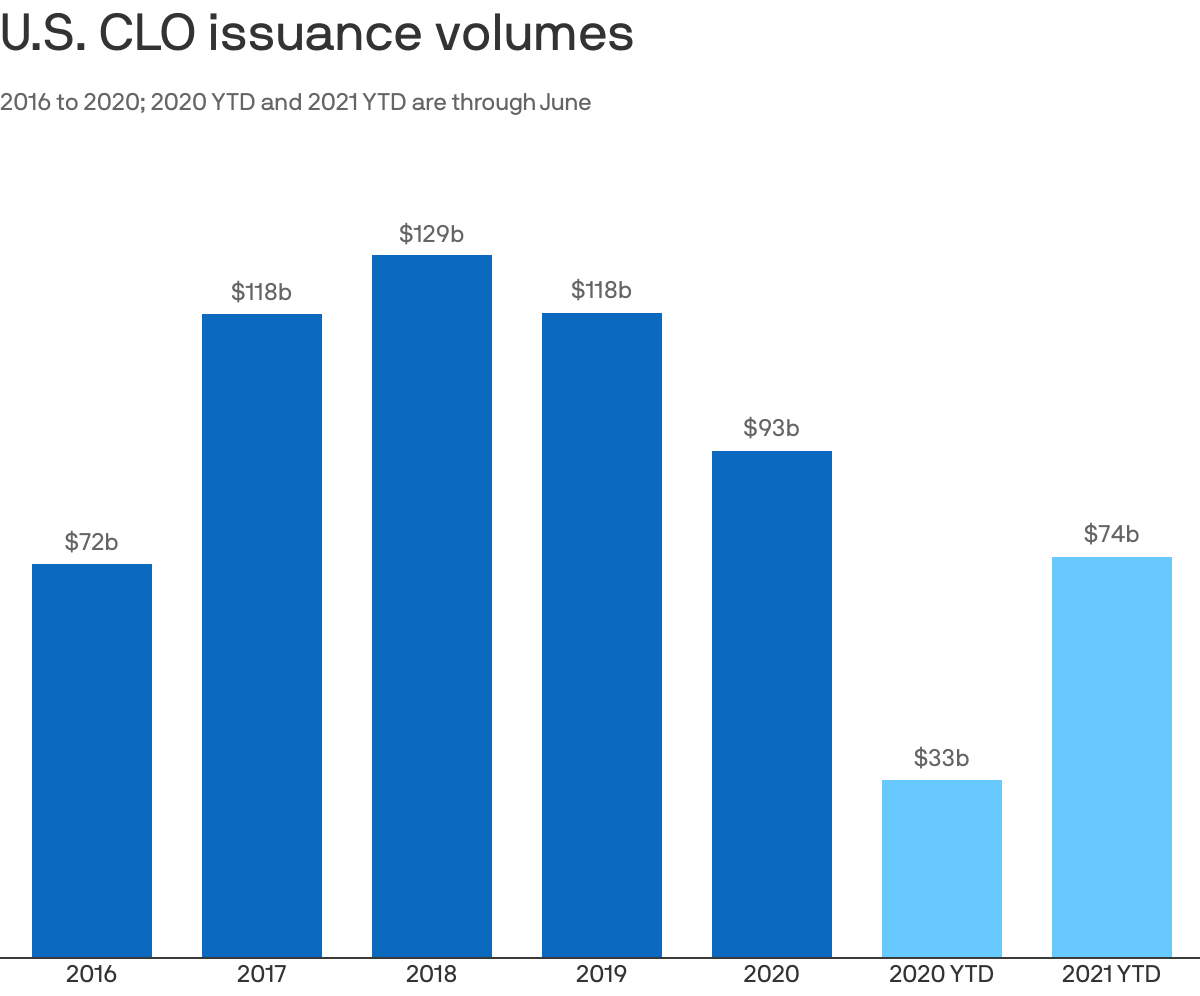

5. CLO investors are back

The global CLO market now totals about $993 billion, and it’s growing, according to analysts at JPMorgan. With record issuance expected this year, the CLO market is on pace to top the $1 trillion mark, Kate writes.

Why it matters: If you have money with an insurance company or a pension, chances are some of that is invested in CLOs.

- Some investors pulled back from the CLO market last year when they feared a wave of ratings downgrades for loans would hurt the value of the portfolios. But those ratings cuts never really came en masse, Bloomberg reported.

Driving the news: "We have seen big banks and foreign investors that buy CLOs come back into the market," says Maureen D'Alleva, head of performing credit at Angelo Gordon.

Case in point: Citizens Bank started up a CLO purchase program recently, Bruce Van Saun, CEO of Citizens Financial Group, tells Axios.

- Banks are sitting on record deposits. As Citizens’ cash started piling up, it looked for ways to diversify how it invested the funds. That's when, like many banks, it opted to begin purchasing the senior-most slices of CLOs.

How it works: CLOs buy hundreds of noninvestment grade loans, bundle them together, and then sell slices of the portfolio to investors.

The bottom line: CLO structures first came to prominence in the early 2000s. They survived the financial crisis, and the COVID-19 pandemic — and their growth shows no signs of stopping.

Go deeper: Here’s an explainer on how CLOs work. (Spoiler alert: It’s complicated.)

Axios Markets

Stay on top of the latest market trends and economic insights