Axios Markets

July 30, 2022

1 big thing: It's stopped making sense

Photo illustration: Annelise Capossela/Axios. Photos: FPG, Heritage Art/Heritage Images via Getty Images

2. Regulator sympathy for crypto evaporates

Illustration: Aïda Amer/Axios

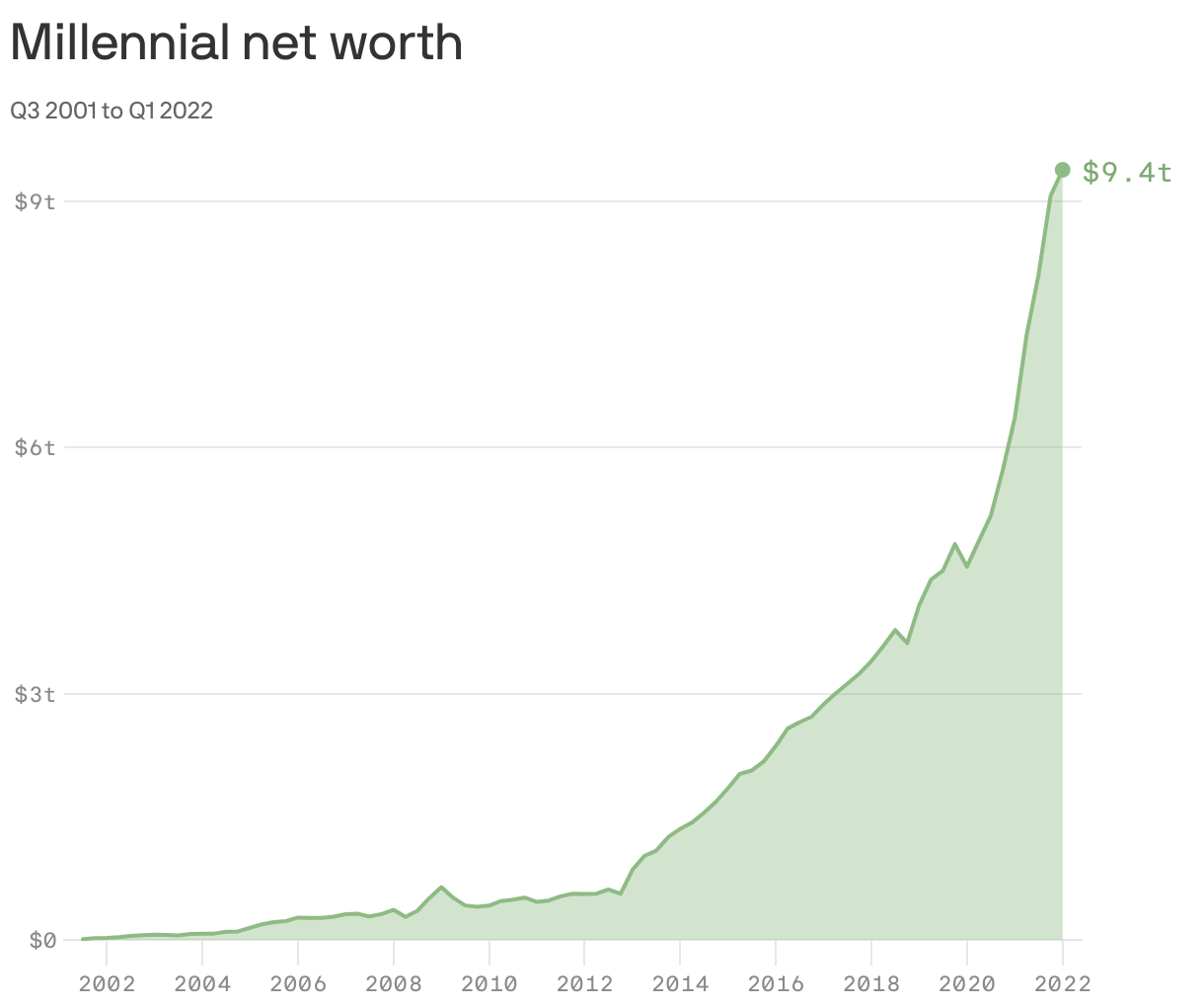

3. The first $10 trillion is always the hardest

Millennials are twice as rich as they were before the pandemic.

Why it matters: The recession arrived when millennials — anybody born between 1981 and 1996 — were feeling burned out and doomed. Student loans were stretching as far as the eye can see, and millennial wealth was just a fraction of what previous generations had managed to accumulate at the same age.

- The pandemic changed everything. Student loans payments were paused, government stimulus checks started pouring in, the stock market soared, and house prices spiked.

Where it stands: Millennials had an average of $127,793 in net worth in the first quarter of 2022.

- When Boomers were the same age, in 1989, their net worth (in 2022 dollars) was a comparable $136,786, according to Kali McFadden, a data research manager at LendingTree.

The catch: While millennials' wealth has risen very quickly in percentage terms, it's still tiny compared to other generations in absolute terms. While millennials gained $4.8 trillion of wealth in two years, Generation X gained $16.4 trillion, and now have some $42 trillion in total.

The bottom line: Millennials are not yet rich, but at least they're finally on their way.

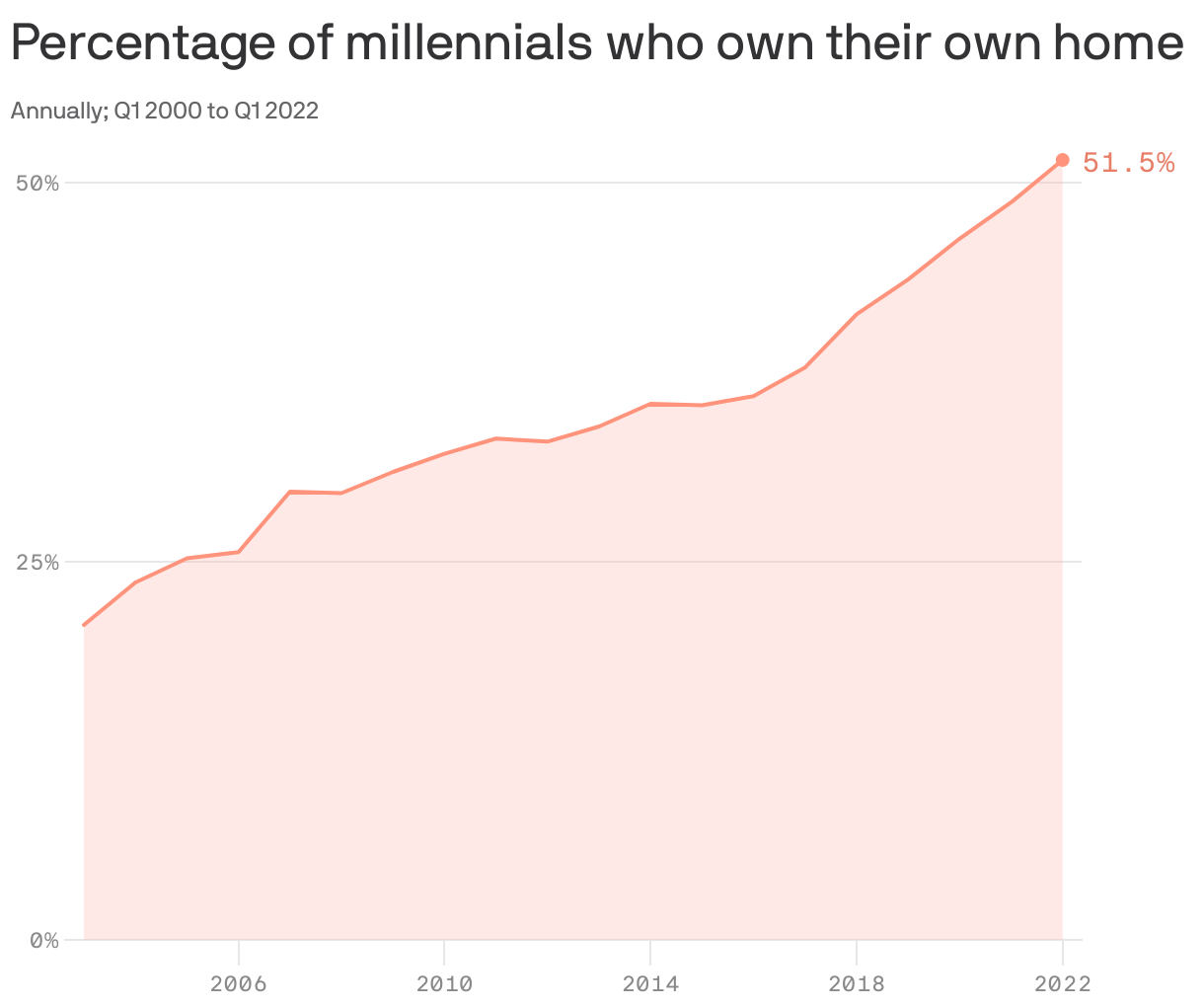

4. Millennial homeownership hits 50%

One of the key reasons that millennials saw their wealth rise so quickly during the pandemic is that they started their home-buying spurt just in time.

By the numbers: Between 2016 and 2022, millennial homeownership soared from 36% to more than 51%.

- The Census Bureau chart above actually understates the degree to which homeownership rose. That's because it only includes "householders" — people who have a mortgage or a lease in their own name. So in the earlier years, millennials in dorm rooms or living with their parents weren't even counted in the denominator.

How it works: Recent first-time homebuyers tend to be the most leveraged, magnifying returns in up markets.

- If you put down a 10% downpayment, and your house goes up in value by 50%, then the equity you have in your home goes up by six times.

The bottom line: Many millennials got onto the housing ladder just in time.

5. Building of the week: Balfron Tower, London

Photo: Sam Mellish / In Pictures via Getty Images

Axios Markets

Stay on top of the latest market trends and economic insights