Axios Markets

January 12, 2026

🚨 The Federal Reserve's independence has been a red line for many investors. That line is in danger of being crossed.

- Federal prosecutors have opened an investigation into Federal Reserve chair Jerome Powell over the central bank's recent renovation.

- In a video message, Powell suggested the investigation was actually about the independence of the central bank, adding that he would continue to do the job the Senate confirmed him to do "without fear or favor."

- Futures are sinking, gold hit a record high and the dollar is under pressure.

Today: Two other ways the Trump administration is throwing its weight around in ways that impact markets. Let's get into it. All in 1,236 words in 4 minutes.

1 big thing: How Trump's "quantitative easing" could impact investors

There's a giant player in the financial markets who's changing the rules of the game. His name is President Trump.

Why it matters: In pursuing an affordability agenda, the president is making policy moves that investors have not accurately priced in.

What they're saying: "You are on the receiving end of policy — I don't think the market realizes this," Mohamed El-Erian, economist and advisor, tells Axios.

- "Affordability is driving not just policy outcomes, but will increasingly drive market outcomes."

State of play: Trump instructed Fannie Mae and Freddie Mac late Thursday to buy $200 billion in mortgage-backed securities in an effort to lower mortgage rates.

- On Friday, 30-year mortgage rates dipped below 6% for the first time since August of 2022 as the market priced in a possible buying spree.

- "It's like quasi-QE," said Calvin Yeoh, portfolio manager at the hedge fund Blue Edge Advisors, per Bloomberg, comparing the Fannie-Freddie buying to the Federal Reserve's purchases as part of its quantitative easing program. "It boosts demand for borrowing further out the curve."

- "What the market likes more than anything else is a non-commercial buyer, this notion that someone will buy regardless of price," El-Erian says.

- While it's unclear if Friday's moves lower in yields will stick, El-Erian believes the yield on the bench 10-year Treasury will be lower than it would have otherwise without the potential Fannie/Freddie purchases.

Zoom out: A common refrain on Wall Street is that Washington policy tackles the demand side of problems that are often supply-driven. Take housing:

- Right now, there's a lack of affordable housing.

- Increasing MBS purchases in an effort to lower rates could shave 10 to 15 basis points off a mortgage, according to strategists, but in return, there could be a swell of demand from buyers who are eager for lower rates.

- That demand swell could in turn lead to higher prices.

- The U.K. offers a cautionary tale: Efforts to make mortgages cheaper for first-time buyers there fueled demand, which inflated prices, leaving affordability worse off.

Threat level: The "nightmare outcome is they only try to operate on the demand side that pushes prices up, inflation as a whole goes up, and then you have a Fed that's on the wrong side of the inflation equation," El-Erian says.

Yes, but: Over the last year, rates have fallen, but demand didn't pick up.

- People are holding onto homes longer and the economic vibes are weird, so fewer people are buying.

What we're watching: Whether more bond buying is coming.

- While $200 billion in purchases is relatively small for the $9 trillion MBS market, if the administration or the Fed indicate a willingness to buy more, that "could have a major impact on mortgage costs," El-Erian says.

- Administration officials have repeatedly told Axios that more details on the policy would come from Trump's speech at Davos.

The bottom line: It's a stock picker's market, and the winners and losers across asset classes are increasingly being defined by policy coming out of Washington.

2. Trump gets more creative when it comes to financing

President Trump wants to spend. He also wants, where possible, to avoid congressional interference and bigger deficits. Enter the balance sheet.

The big picture: The president is going through the couch cushions of government — $200 billion from Fannie Mae and Freddie Mac for mortgage bonds, $20 billion from a Treasury fund for Argentina — to advance his policy priorities.

- Critics say it's nontraditional at best, and autocrat-adjacent at worst.

What they're saying: "The executive branch is getting very creative using the pockets of money at their disposal with no congressional oversight," Ed Al-Hussainy, portfolio manager at Columbia Threadneedle, tells Axios.

- On a call with clients, BCA research strategists compared the latest Trump policies to those of New York City Mayor Zohran Mamdani and Chinese leader Xi Jinping.

- It's "communism with capitalist characteristics," Al-Hussainy says.

State of play: Here's how government money has been used in unconventional ways:

- The Treasury's Exchange Stabilization Fund was tapped to underwrite a currency swap with Argentina.

- Administration officials floated the use of unspecified pools of capital to backstop oil assets tied to Venezuela and to potentially purchase Greenland.

- Now, Trump is directing Fannie Mae and Freddie Mac to buy $200 billion worth of mortgage-backed security (MBS) in an effort to lower rates.

The other side: "The American people gave President Trump a resounding Election Day mandate to smash Washington, D.C.'s broken status quo and actually put Americans and America First," White House spokesperson Kush Desai tells Axios.

- "That includes advancing an America First agenda to turn the page on Joe Biden's affordability crisis and safeguard our national security without needlessly blowing taxpayer money."

Between the lines: Investors should assume Trump will keep looking for ways to access capital to achieve his goals without getting congressional approval, Peter Tchir, head of macro for Academy Securities, said on a call with clients.

- "I would not think that they will stick to traditional methods to accomplish their goals. They've said what they want. The market seems to be ignoring them," Tchir said.

Threat level: The "ultimate win" for Trump? Tapping the balance sheet of the Federal Reserve to use as he pleases, Al-Hussainy says.

- This can have consequences.

- Look to Japan: Years of central bank bond-buying made government borrowing easy, and debt exploded as a result.

- When inflation arrived post-pandemic, the Bank of Japan had less wiggle room to respond, and the yen took a hit.

Yes, but: Treasury Secretary Bessent has criticized the Fed's use of the balance sheet as a crisis response tool.

The bottom line: In order to not increase the deficit or raise taxes, Trump is getting creative.

- Investors should take note and follow the money to determine how the executive spending could impact their investments.

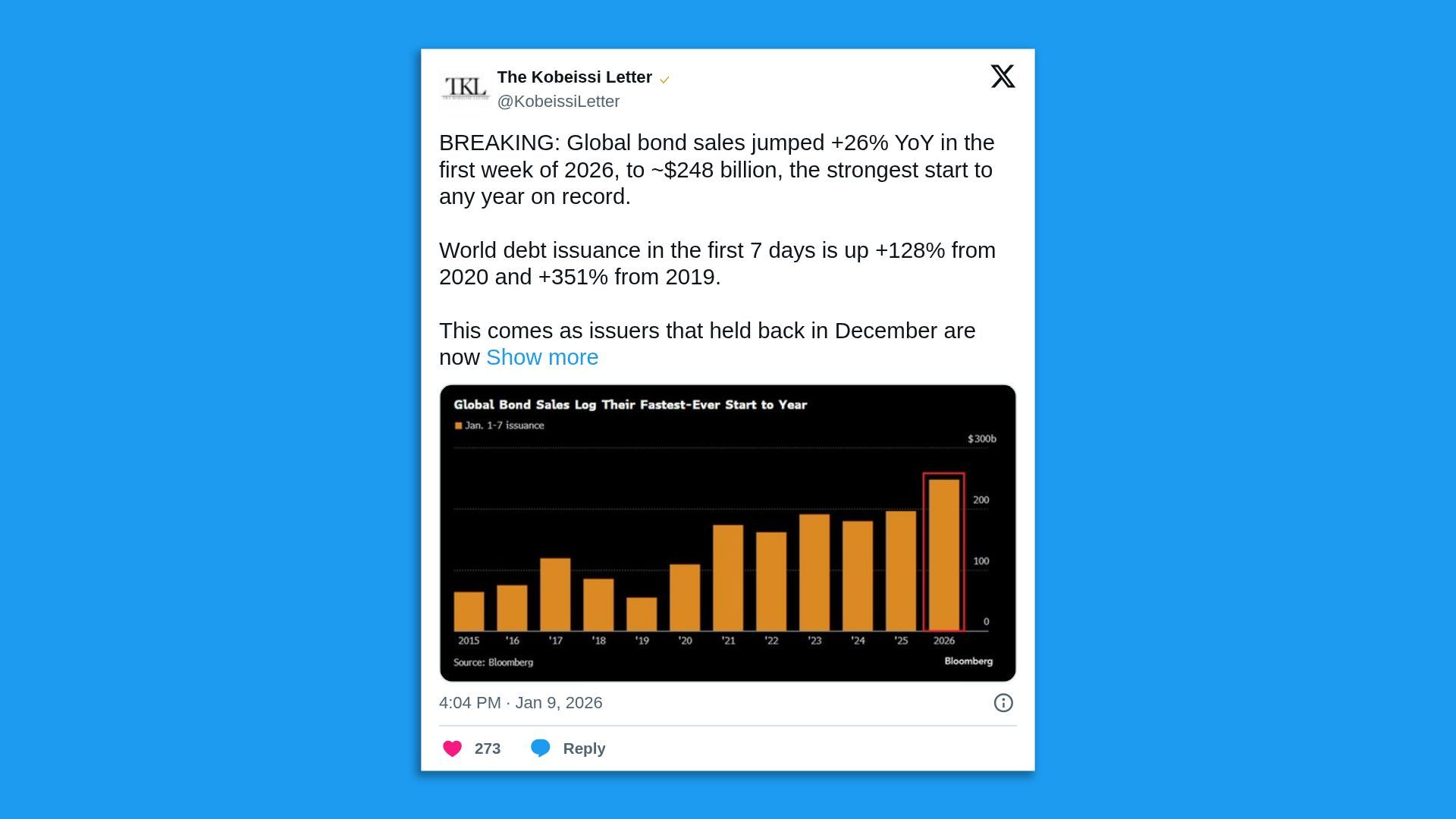

3. Bonds catch an early year bid

Global bond sales surged 26% in the first week of 2026 from a year ago, reaching roughly $248 billion— the strongest start to any year on record.

Why it matters: Early-year issuance is always busy, but this record pace signals urgency from borrowers and suggests markets are bracing for tighter financial conditions as 2026 unfolds.

By the numbers: Debt issuance in the first seven days of the year is 128% higher than 2020 and 351% above 2019 levels.

Between the lines: You can read the surge as optimism — or see it as issuers rushing to lock in funding before rates shift again.

Zoom in: Borrowers may be trying to get in front of a looming wave of AI-linked bond issuance, which investors expect could push borrowing costs higher as supply swells

Got tips? Email me at [email protected]. I would love to hear from you about anything that may be of interest for our investor audience.

Thanks to Jeffrey Cane for editing and to Carolyn DiPaolo for copy editing. See you tomorrow!

Sign up for Axios Markets