Axios Markets

July 17, 2025

👁️ Blink and you'd miss the market's swift sell-off, then rebound, after reports that President Trump might fire Fed chair Jerome Powell.

- Today: what the market response to a Powell firing could actually look like.

- Plus: why the bond market seems unbothered by a possible Fed shake-up.

💰 Situational awareness: Goldman Sachs had the highest trading revenue in history in an extremely volatile quarter. As you read on, remember headline risk doesn't have to equal portfolio risk.

All in 975 words and 3.5 minutes.

1 big thing: How markets might react to a Powell firing

If Trump fires the Fed's Powell, it would likely bring a period of short-term market volatility — along with higher long-term borrowing costs, as the Fed would be viewed as more subject to a president's whims.

The big picture: Trump appears to be itching to push out the Fed chief he originally appointed, perhaps by claiming that an over-budget building renovation constitutes legal cause.

- Paired with efforts to staff the Fed with more overtly political loyalists, that could remake what has been a bedrock of U.S. financial assets for decades — a central bank that is removed from the day-to-day political maw.

State of play: In the immediate aftermath of a Powell firing, there would be a period of deep uncertainty around who was in charge of the world's most powerful central bank.

- Would Powell be able to stay in his job while pursuing legal challenges? And how long would it take those legal challenges to be resolved one way or the other? Nobody really knows, because this hasn't happened before.

- Presumably, vice chair Philip Jefferson — not particularly well-known to financial markets — would temporarily lead the Board of Governors, while New York Fed president John Williams would lead the policy-setting Federal Open Market Committee. (By tradition, the New York Fed chief is vice chair of the committee.)

Zoom out: Short-term volatility is one thing. The bigger question strategists are weighing is how markets might price in a new monetary regime under more direct White House control.

- A strong possibility is that a new Fed chair aligned with Trump's desires to cut short-term interest rates might end up delivering a much steeper yield curve — lower short-term rates paired with higher long-term rates.

By the numbers: The 30-year U.S. Treasury bond yielded 5.01% at Tuesday's close, and prices of comparable inflation-protected securities imply that investors anticipate 2.35% annual inflation over that time horizon.

- If investors come to believe that any Fed chair who displeases the president will be fired, they could lose confidence that inflation will hover at that low level, driving long-term bond rates up.

What they're saying: The long end of the Treasury yield curve "already has an elevated fiscal deficit and upside to consumer price pressures coming from tariffs to worry about," wrote ING's Padhraic Garvey, Francesco Pesole and Chris Turner in a note.

- "Adding front-end rates that are arguably too low for the economy risks adding permanence to the higher inflation prints," they add. "The outcome then is a much steeper curve, with front-end yields lower and longer-term yields higher."

- They argue that it would generate a flight away from the U.S. dollar and toward the euro, Japanese yen, and Swiss Franc.

The bottom line: If Trump follows through with his threats, expect a period of volatility, paired with cheaper short-term borrowing and higher long-term borrowing costs.

2. How stocks could tumble

Stock investors started selling at 11:15am ET yesterday when Bloomberg reported that Trump was likely to fire Powell soon.

Why it matters: The nearly 1% decline is a mild premonition for equity investors of what's to come if the Fed chair is really ousted.

What they're saying: "It will be several orders of magnitude worse, should the White House ever truly move to fire Powell," Joe Brusuelas, chief economist at RSM US, tells Axios.

- Firing the central bank chief sets the stage "for further diversification away from dollar denominated assets," Brusuelas later added in a note.

Between the lines: Stocks are dollar-denominated assets.

- While stocks recovered their losses yesterday, the dollar did not.

- This could be an indication that investors are temporarily OK with the risk/reward profile of equities, but they're gradually moving away from the dollar.

- Over time, that alone could be a drag on equities.

What we're watching: The market's swift rebound mirrors a vibe that crosses conversations with sources: Wall Street sentiment surrounding a potential Powell removal appears to be shifting.

- Mohamed El-Erian, Queens' College president and former Pimco CEO, posted about whether Powell is exposing the central bank to threats by staying in the post within a hostile administration.

- The TACO trade could be shifting to the Trump-is-right trade, a narrative that would be bolstered by market resilience in the face of a Fed chair firing.

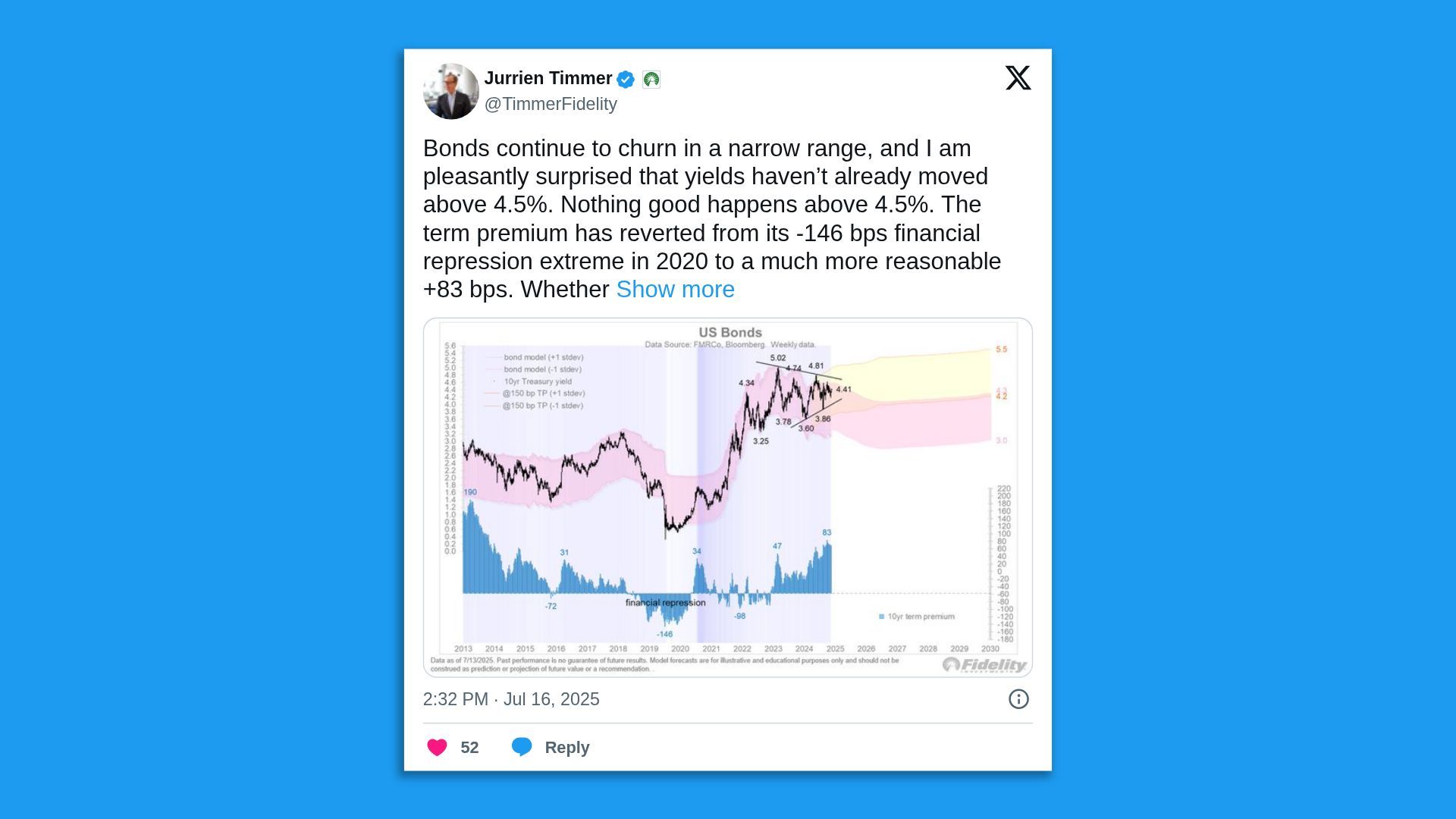

3. Beware 4.5% bond yields

Nothing good happens after 2am — or after bond yields climb above 4.5%, according to Jurrien Timmer, the director of global macro at Fidelity.

- Bond yields are holding steady and, for now, staying below the 4.5% threshold that some investors see as a danger zone for markets.

Why it matters: Longer-dated Treasury yields could tick up if investors lack confidence about the U.S. going forward.

- If yields climb, borrowing gets more expensive, rippling through everything from stock valuations to mortgage rates.

By the numbers: So far, the bond market has been calm in the face of inflation risks, deficit concerns and reports that the administration is attempting to eject Powell early.

- The 10-year yield hasn't pushed above 4.5%, despite rising debt and inflation risks.

- The term premium — a measure of how much extra compensation investors demand for holding long-term bonds — has risen from -1.46% in 2020 (an extreme low during the pandemic) to +0.83% now, a more "normal" level, Timmer wrote.

- If investors start to see U.S. debt as a riskier investment, that term premium could rise, pushing yields higher.

What we're watching: The next move in yields may depend not just on inflation, but on how the government decides to borrow money. We'll get clues when the Treasury's quarterly refunding announcement comes out Oct. 17, according to Timmer.

💭 Mady's thought bubble: I was living and reporting in Dubai when the Turkish lira crashed, thanks to President Recep Tayyip Erdogan replacing the central bank chief with someone who would be more dovish.

- I'm not saying we're Turkey. But seeing a currency crash like that firsthand taught me that replacing the head of a central bank is risky business.

⭐️ We're bringing Media Trends to life with Axios' inaugural Media Trends Live event in NYC on Sept. 18 featuring ESPN chair Jimmy Pitaro, Paramount Global chair Shari Redstone, Snap Inc. CEO Evan Spiegel and more. Find event info and purchase your ticket here.

Thanks to Ben Berkowitz for editing and Katie Lewis for copy editing.

See you tomorrow!

Sign up for Axios Markets