Axios Macro

June 27, 2024

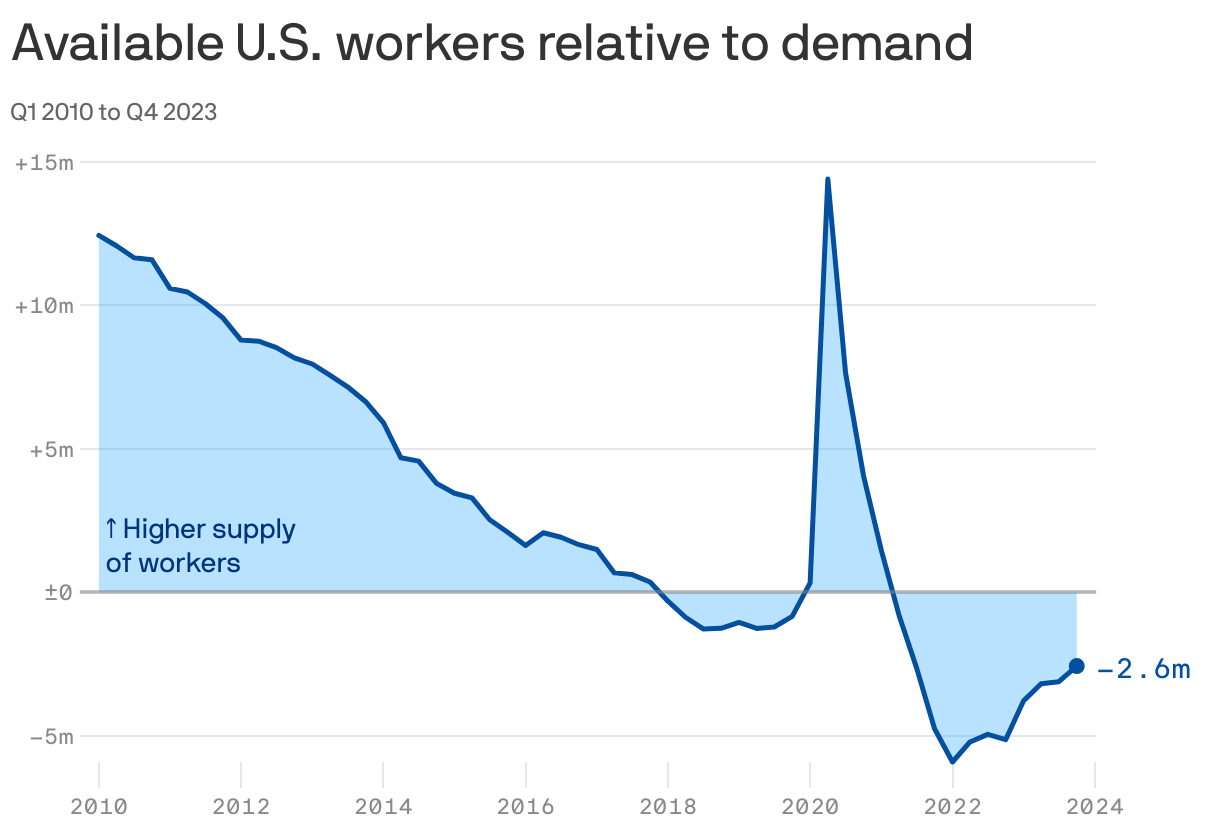

1 big thing: Labor scarcity is the new normal

The core economic fact of the 2010s was that there were not enough jobs. The key to understanding the economy of the 2020s is that there aren't enough workers.

Why it matters: Labor shortages that first emerged in the pandemic aftermath are likely to stick around, a new report from the McKinsey Global Institute finds — along with the benefits it entails for workers, headaches it causes for employers, and strains on inflation and growth.

- Businesses will have to figure out how to generate the same output with fewer workers — a big risk for U.S. economic growth, if new technologies like generative AI don't deliver.

- It is part of a global phenomenon, the McKinsey researchers find, warning that tight labor markets around the world were not merely a blip but a long-term trend that will continue as the Baby Boom generation ages out of the workforce.

What they're saying: "The surplus of unemployed people or job seekers has dwindled to historic lows across the global economy," Anu Madgavkar, co-author of the report, tells Axios.

- "This is a profound change. It means all of the assumptions that businesses have made — that they could grow relatively easily by hiring people — are being challenged," Madgavkar adds.

Where it stands: The U.S. job markets have loosened some since 2022, thanks to chilled demand and immigrants entering the workforce. But even so, the unemployment rate stands at 4%, lower than in any month from December 2000 through 2017.

By the numbers: McKinsey found that the number of open jobs per available worker in the U.S. increased by more than seven times between 2010 and 2023.

- Without higher worker participation or efforts to boost productivity, "many advanced economies will struggle to exceed—or even match—the relatively muted economic growth of the past decade," the report warns.

The intrigue: Tight labor markets mean workers can demand higher wages, particularly in sectors like health care, construction and leisure and hospitality where shortages are most acute.

- "In a way, this ultimately forces businesses to focus on productivity to sustain higher wage costs," Madgavkar says. "If the output or the value added per worker goes up, it's possible to sustain that higher wage without feeling the pinch."

What to watch: It's unclear what role generative AI will play in the years ahead to help boost productivity. But the technology might be embraced faster than would otherwise be the case with persistent worker shortages.

- McKinsey says AI adoption might create a new type of shortage: Routine work will be commoditized faster, while creative cognitive work will soar in demand — and skills will need to adjust.

- "Can human beings make that leap? Some certainly can," Madgavkar says. "It boils down to employers and the education system to make that happen— that's really the big challenge going forward."

Axios Macro