Axios Macro

November 15, 2022

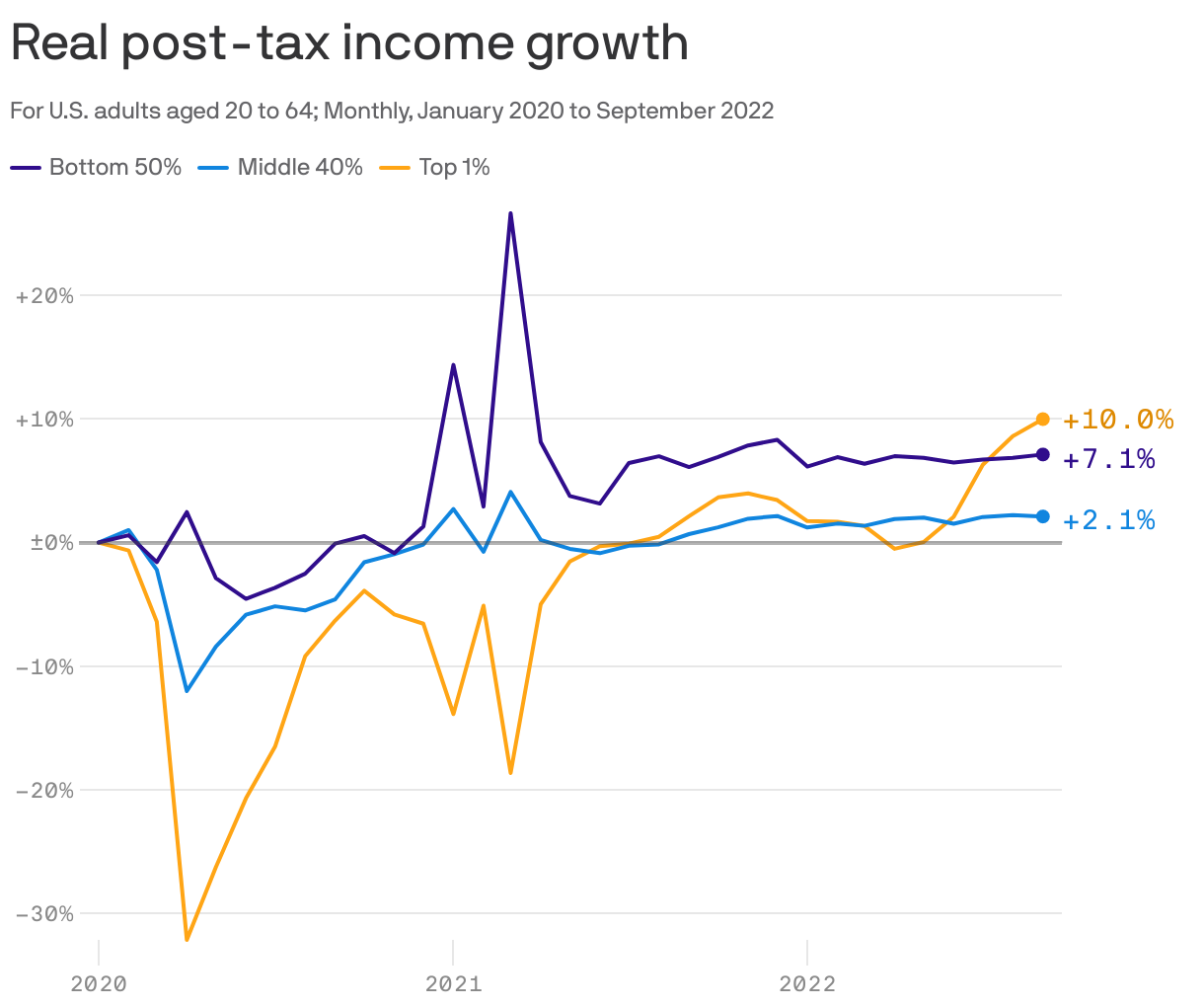

1 big thing: Pay growth beneficiaries

The working class has seen notable inflation-adjusted income gains since the pandemic hit, recent data suggests.

Why it matters: The aftermath of the COVID-19 recession has been characterized, in part, by strong pay gains for lower-wage workers. That's a break from decades of sluggish income growth for the bottom half of households.

The intrigue: During the years-long recovery from the 2008 recession, the middle class experienced modest income gains. But the bottom and top of the distribution saw gains stall.

- What's happening now is the opposite: The top and bottom are seeing big gains. But the middle class? Less so.

Details: University of California, Berkeley economists Thomas Blanchet, Emmanuel Saez and Gabriel Zucman revealed those findings in a paper updated this month.

- They are behind Realtime Inequality, whose data we cite in the above chart. The project aims to provide growth statistics by income group.

What they're saying: Booming wage growth for the bottom 50% of Americans since the pandemic caused "a reduction in wage inequality among the bottom 99%, a break from the trend prevailing since the early 1980s," the authors write.

Flashback: When COVID hit, incomes for the bottom 50% were boosted by expanded unemployment benefits, stimulus checks and other fiscal support.

- When those measures disappeared, income growth declined from the peak. But income growth continued. That's a reflection of the strong labor market and higher wages for lower-wage workers, Zucman notes.

What to watch: The Fed is actually looking to cool wage gains to bring pay bumps in line with the level "that's sustainable and consistent with 2% inflation," chair Jerome Powell said earlier this month.

The bottom line: Stagnant pay gains among the working class were a "robust feature" of the 2008 recession, the authors write.

- The opposite has been true for the pandemic-era recovery.

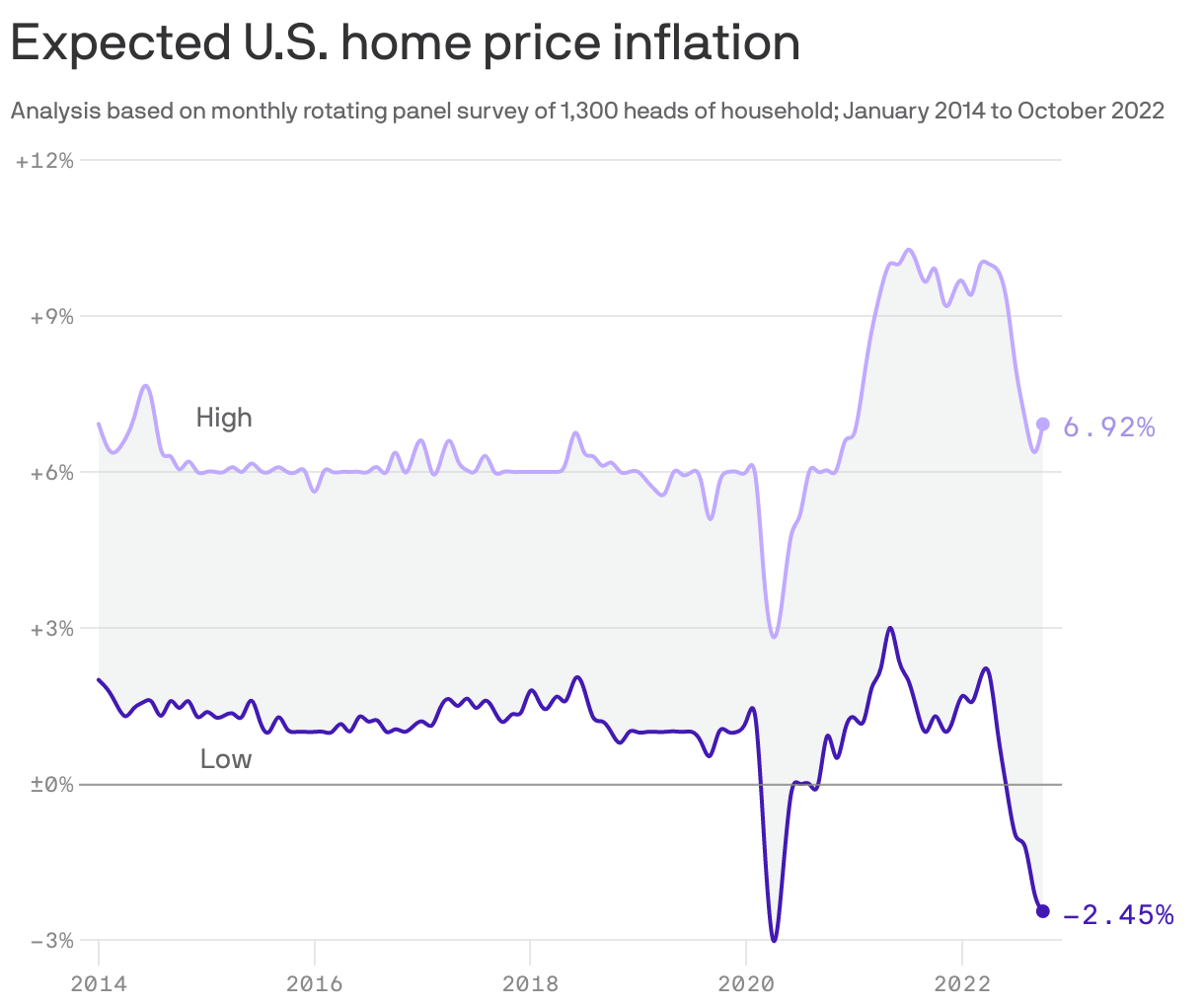

2. Home price uncertainty

Historically, housing has been the main asset that middle-class Americans use to build their wealth. Right now, however, it's more volatile and unpredictable than ever.

Why it matters: If you ask Americans — as the New York Fed does every month — how much home prices are going to rise in value over the next year, they're generally pretty consistent. Around 50% of the answers fall in a roughly 4.5-point range, between 1.5% and 6%.

- But now, that range has more than doubled to 9.4 points — a clear sign of uncertainty and doubt.

Between the lines: It's very uncommon for Americans to predict an outright decline in house prices. But now a growing number are doing just that.

- The bottom 25% say prices are likely to fall by at least 2.45% over the next year.

- By contrast, the top 25% think that prices are likely to rise by at least 6.92%.

The big picture: The price of everything, including housing, tends to go up during times of high inflation.

- For homebuyers, however, the cost of buying a home (in terms of monthly mortgage payments) can be going up even if the value of the home, in dollar terms, is going down — which means it's no wonder that forecasts are so febrile.

The bottom line: "Safe as houses" isn't very safe right now.

Axios Macro

Stay ahead of the curve on the most important economic developments with reporting and analysis on how business, policy, and markets collide.