Axios Macro

November 10, 2025

1 big thing: The problem with a 50-year mortgage

The Trump administration has an idea to make buying a house more affordable — using the government's control over the mortgage finance system to offer home loans that can be paid off over a much longer time.

The big picture: The arithmetic of loan amortization, however, means that buyers taking out a 50-year mortgage would lose a key advantage of the more traditional loan product, while not saving that much month-to-month.

- With a traditional mortgage loan, a homeowner steadily pays down debt and builds equity. A 50-year mortgage would involve very little paydown of debt over the first couple of decades.

- The 50-year loan would likely carry a higher interest rate than widely available 30-year mortgages, limiting the savings on the monthly payment.

Driving the news: "Thanks to President Trump, we are indeed working on The 50 year Mortgage — a complete game changer," wrote Federal Housing Finance Agency director Bill Pulte on X over the weekend.

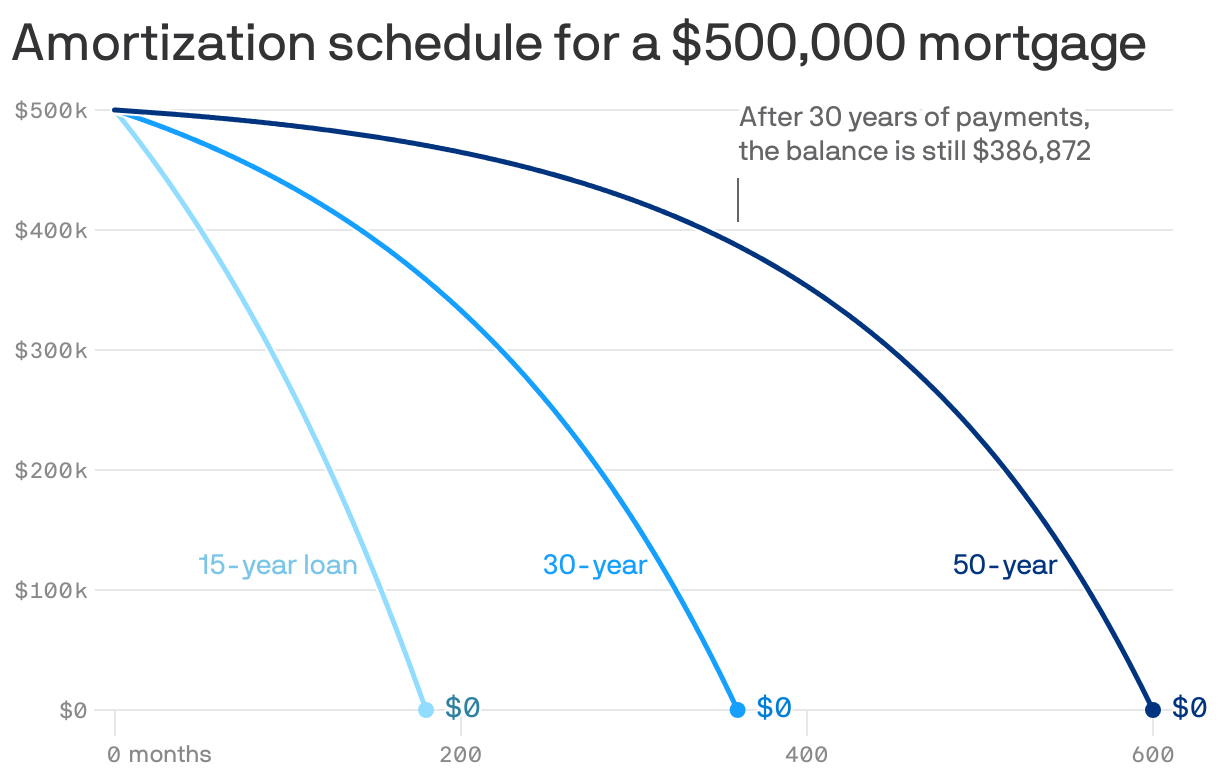

By the numbers: Consider someone taking out a $500,000 home loan. The current rate on a 30-year mortgage is 6.22%, per Freddie Mac. For these calculations, let's assume that a 50-year loan's interest rate exceeds the 30-year by the same margin that the 30-year rate exceeds a 15-year rate.

- That translates to a 6.94% rate on the 50-year loan — which would then have a monthly payment of $2,985, only $83 less than the 30-year mortgage.

Zoom in: In the early decades of the loan's repayment, the 50-year borrower's payments would almost entirely go to interest, paying down the debt much more slowly.

- After five years, for example, the 30-year borrower would have paid off $33,481 of the loan balance, versus $6,707 for the 50-year borrower.

- After three decades, when the 30-year mortgage is fully paid off, the 50-year borrower would still owe about $387,000.

Between the lines: One of the benefits of a traditional mortgage loan is that it incorporates forced saving, as you gradually grind down your debt. The 50-year loan lessens that benefit.

- A person who buys a house in their 30s stands to own it free and clear as they hit retirement age. Or if they sell sooner, they will have accumulated equity that they can use toward their next home.

- A 50-year product would more closely resemble an interest-only mortgage, where there is no amortization of the balance for some defined period, like the first five or seven years of the loan term.

Reality check: An interest-only loan can make sense for certain borrowers, such as those with lots of deferred compensation or a lumpy income. But it carries significant risk for both the borrower and the lender, as the world learned the hard way in 2007-2008.

- The risk is that a 50-year mortgage product would have the same downsides.

The bottom line: If the administration succeeds in introducing this product, borrowers who take a 50-year loan will find themselves paying down debts much more slowly than those who use conventional loans, while saving only a little on their monthly payments.

2. A possible reopening data dump

Axios Macro