Axios Macro

June 18, 2025

1 big thing: Exclusive — CEO sentiment at five-year low

Economic sentiment among America's top CEOs plunged to the lowest level since 2020, according to a new survey by the Business Roundtable, first seen by Axios.

Why it matters: Chief executives have not been this sour on the economy since the once-in-a-century pandemic, with significant downgrading expectations for hiring, investment and sales growth.

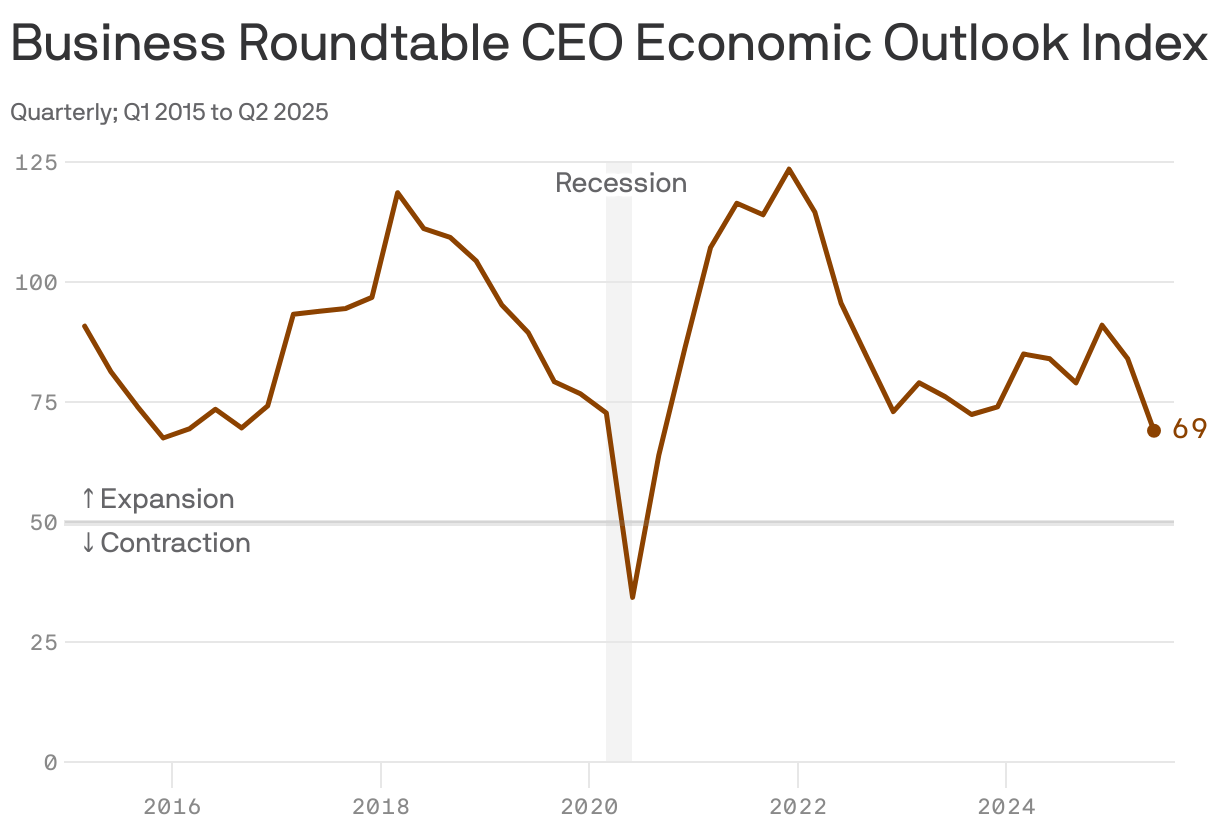

- The Business Roundtable's CEO Economic Outlook Index fell by 15 points in the second quarter to 69, a drop that brings the index well below its historical average of 83.

- The previous survey was conducted in March before President Trump's "Liberation Day" announcing large-scale tariffs. Since then, the trade war has been de-escalated and the stock market recovered, yet CEOs still feel worse about the economy.

Between the lines: The index is above the level that suggests an economic recession is underway. But the survey is troubling for what it signals about the labor market that has so far been resilient, helping buffer the broader economy.

- For months, it's been a "no hire, no fire" labor market with sluggish hiring rates and low layoffs.

By the numbers: Business Roundtable's survey shows risks that this period might be coming to an end.

- The employment subindex plummeted for the second straight quarter — this time, by almost 19 points, with more than 40% of CEOs expecting to shrink their workforces in the next six months.

- That is up from the roughly 30% who envisioned cutting payrolls in Q1. This time last year, just over 20% planned to decrease employment.

- It's difficult to know how much of that slump is related to softer economic projections as opposed to, say, AI-related workforce adjustments.

A subindex for capital expenditures — investment in new buildings, equipment, technology and more — fell roughly 15 points, with fewer executives planning to increase spending.

- That came alongside a more than 10-point drop in sales expectations, with a smaller cohort of CEOs expecting higher revenues.

What they're saying: "Driving this quarter's decline in the Index is broad-based uncertainty, arising substantially from an unpredictable trade policy environment," Joshua Bolten, the Business Roundtable's CEO, said in a release seen by Axios.

- "Extending and enhancing tax reform is critical, but it is not sufficient. American businesses also need the Administration rapidly to secure deals with our trading partners that open markets, remove harmful tariffs and provide certainty for investment," Bolten said.

- The group surveyed 169 of its members in the first two weeks of June, when the U.S.-China trade truce was at risk of breaking down before top Trump officials met with their Chinese counterparts.

Flashback: CEOs had economic euphoria in the early years of Trump's first term, largely on the back of tax cut expectations.

- In the comparable period in 2017, the CEO Economic Outlook Index hit a multiyear high. One year later, it was coming off the highest level ever.

The bottom line: That's no longer the case. Uncertainty about trade and other policies is weighing on the CEO class, which has generally been hesitant to publicly criticize the Trump White House — and trumping any excitement about the prospect of extended tax cuts.

- "The quarter's survey results signal that Business Roundtable CEOs are approaching the next six months with caution," Cisco CEO Chuck Robbins, who chairs the group, said in a release.

- Robbins said the results "underscore the urgent need for Congress to pass pro-growth tax legislation that preserves our globally competitive tax system."

2. New housing market warning

Axios Macro