Axios Macro

August 01, 2025

1 big thing: Job growth stalls out

America's remarkably resilient labor market was a mirage. Hiring came to a screeching halt in the last few months, suggesting more underlying economic weakness than it seemed.

Why it matters: It's rare that a single report drastically shifts our understanding of the economy's health, but that's what happened today at 8:30am ET.

- As of 8:29am, the official data pointed to a steady-as-can-be job creation through June, and analyst forecasts had it continuing in July.

- Now, the largest two-month negative revisions on record — second only to May 2020 — point to a virtual flatlining of job creation in May and June. The July number also came in softer than expected.

- The result: An average of only 35,000 jobs were added per month from May through July. That's the weakest non-pandemic three-month job creations since 2010.

Between the lines: Policymakers who have been assuming that the economy is chugging along fine will suddenly need to rethink their assumptions.

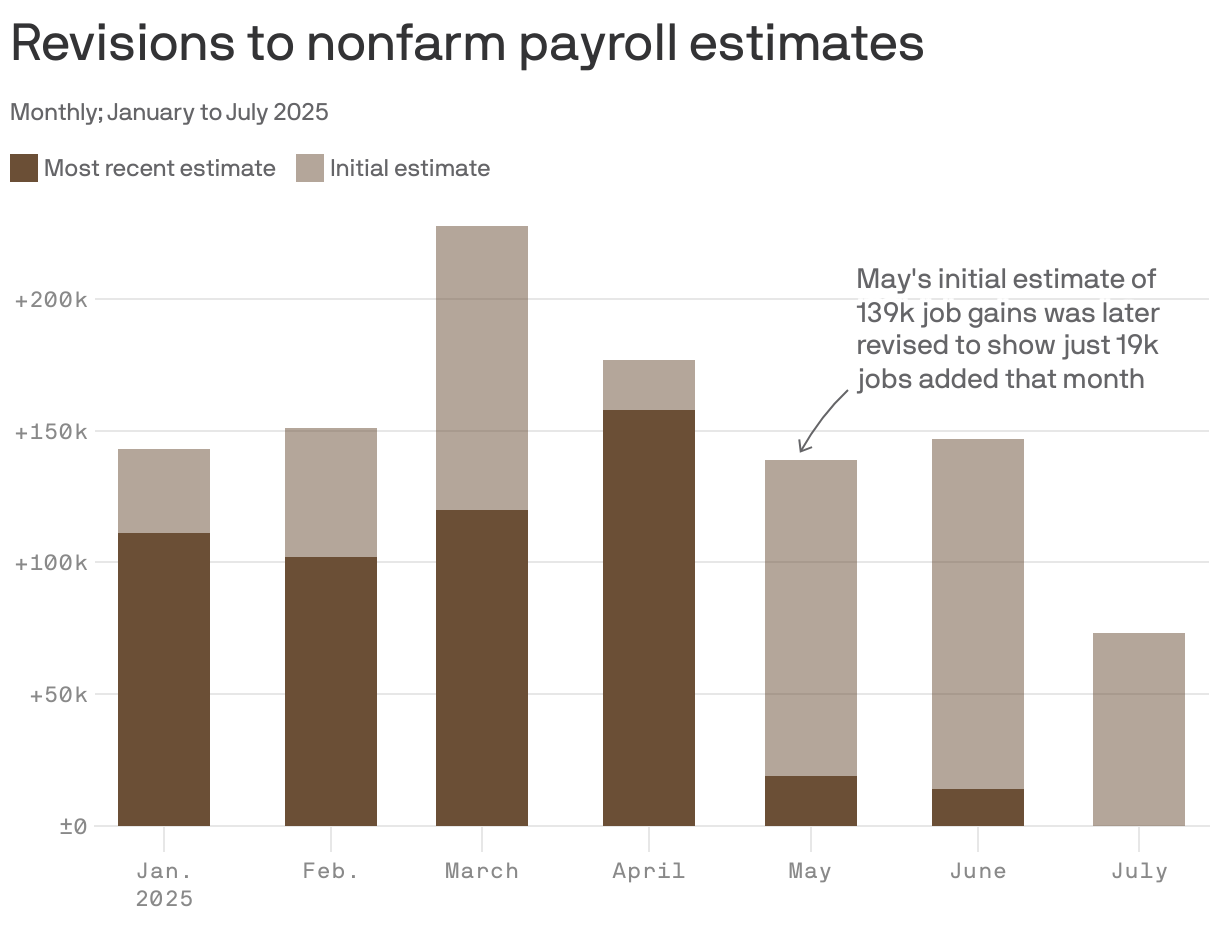

By the numbers: The economy added just 73,000 jobs in July. But the real shocker is the massive downward revision to prior months' data that shows employment has barely budged since April.

- There were 19,000 jobs added in May, not the 144,000 gains that were initially reported. In June, the economy added 14,000 jobs, well below the initial estimate of 147,000 jobs.

- The unemployment rate ticked up as well, to 4.2% from 4.1%, though that keeps it in the low, narrow range where it has been all year.

What they're saying: "Today's report, coupled with sharp downward revisions to the prior two months, makes it clear: job growth has stalled," Olu Sonola, head of U.S. economic research at Fitch Ratings, wrote in a note.

- "The labor market has now shifted from a low-hiring, low-firing environment to one characterized by virtually no hiring."

The intrigue: The economy is in the midst of population shifts as the Trump administration cracks down on immigration. That might help explain the huge revisions; people who are deported, or who stay away from their workplace to avoid raids, do not show up on payrolls.

- It also might explain why hiring is stalling but the jobless rate didn't deteriorate nearly as much; companies can't hire workers who are not available.

- The labor force participation rate, the share of adults with a job or looking for one, is 62.2% as of July — a half-percentage point lower than the same period a year ago.

Flashback: In response to a question from Neil earlier this week, Federal Reserve chair Jerome Powell said that the unemployment rate might be a more reliable indicator of the labor market's health.

- "The main number you have to look at now is the unemployment rate," Powell said on Wednesday, and added that demand for workers has slowed but so has the number of workers the economy needs to add to keep the unemployment rate steady.

For the record: "This jobs report isn't ideal," Council of Economic Advisors chair Stephen Miran told CNN this morning.

- But, Miran said, "it's all going to get much, much better from here," pointing to more certainty on fiscal and trade policy.

The bottom line: The labor market is showing big cracks that were all but invisible just weeks ago.

2. The case of the missing job growth

To understand what's causing weak job creation, it helps to unpack which sectors have decelerated most.

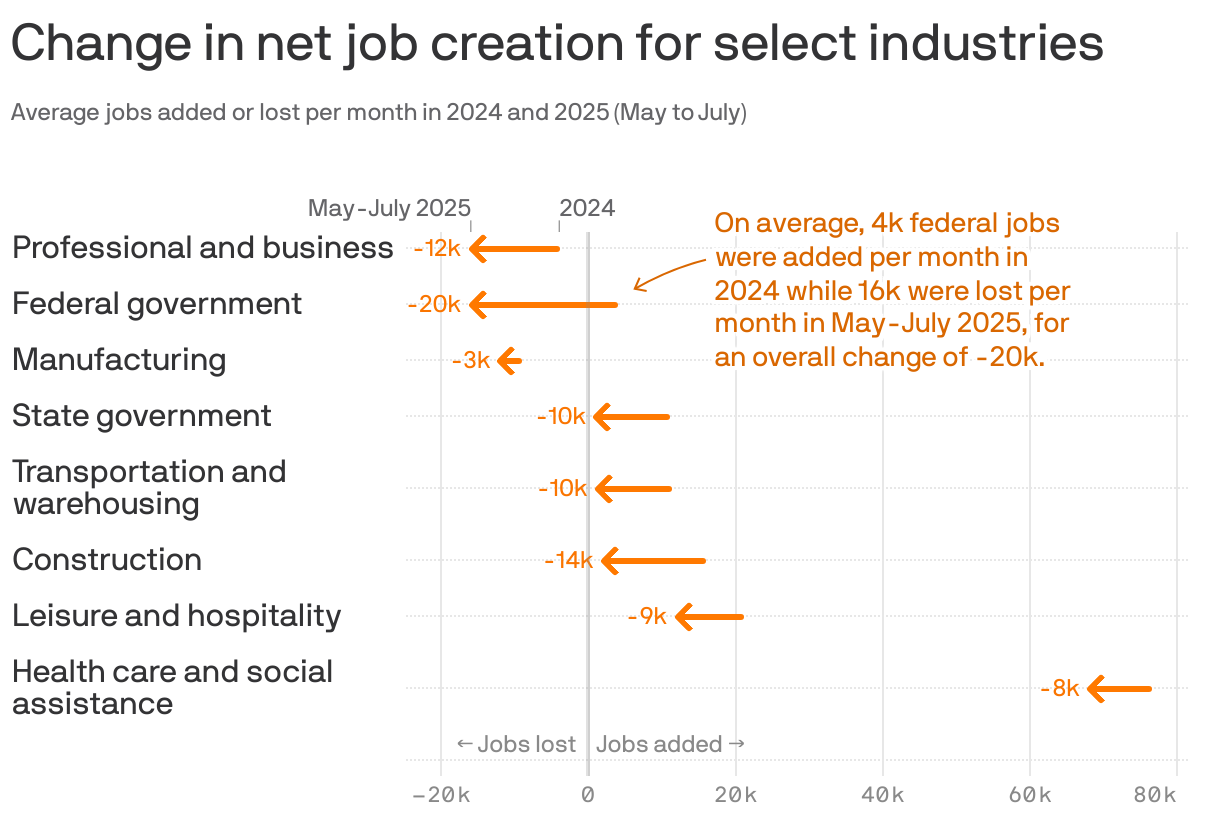

By the numbers: Last year, the economy added an average of 168,000 jobs a month. That has fallen to 35,000 over the last three months. But the slowdown is not even across sectors.

- Federal government employment bumped along, adding 4,000 jobs a month last year, but it has fallen by 16,000 a month this summer. That swing, reflecting DOGE cuts and other Trump administration cutbacks, is the single biggest source of deceleration.

State of play: The construction sector has also taken a major step back, going from adding 16,000 jobs a month last year to 2,000 a month this summer.

- It is somewhat harder to parse why construction employment is flatlining. Both more aggressive immigration enforcement and elevated interest rates are likely factors, putting pressure on the supply of workers and the demand for them.

- The leisure and hospitality sector — which includes restaurants and hotels, heavy users of immigrant labor — added 21,000 jobs per month last year. That dropped to just 12,000 this summer.

- Health care and state government employment, both big drivers of job growth in 2024, have also decelerated this summer, by 10,000 and 8,000 monthly jobs, respectively.

The intrigue: The hiring trend for U.S. manufacturers is fairly steady, despite the whiplash from President Trump's trade war.

- There is no sign of a boom from a shift to domestic manufacturing; but there is no sign of a bust as U.S. firms face higher tariffs on key inputs.

3. Fed dissenters may have a case of the told-ya-sos

At the Fed policy meeting that concluded Wednesday, governors Christopher Waller and Michelle Bowman dissented from the decision to leave rates unchanged, believing that a rate cut was justified. It looks like they had a point.

The intrigue: At 8am ET this morning — half an hour before the jobs report — Waller and Bowman issued statements explaining their dissents.

- It's clear they were worried about exactly the kind of labor market cracks that exploded into plain view with the new revisions.

What they're saying: Waller's statement says that "while the labor market looks fine on the surface, once we account for expected data revisions, private-sector payroll growth is near stall speed, and other data suggest that the downside risks to the labor market have increased."

- "With underlying inflation near target and the upside risks to inflation limited, we should not wait until the labor market deteriorates before we cut the policy rate," he continued.

- Bowman said that "the labor market has become less dynamic and shows increasing signs of fragility."

What's next: The odds of a rate cut at the next Fed policy meeting in mid-September skyrocketed after the weak numbers, and bond yields fell.

- The likelihood was 38% yesterday, per the CME FedWatch tool, but went up to 80% today.

- The two-year Treasury yield fell a whopping 0.19 percentage point.

The bottom line: Waller and Bowman didn't win the argument at the Federal Open Market Committee table this week, but the latest data only bolsters their concerns and means they're likely to win the day when the Fed next meets.

Axios Macro