Axios Generate

July 25, 2018

1 big thing: Visualizing IEA's renewables warning

Let's revisit a topic I just grazed a week ago — the International Energy Agency's fear about inadequate global investment on renewable power projects.

Why it matters: A new IEA commentary offers a cogent look at why the Paris-based agency says the growth in global investment is lagging behind that's needed to meet international climate targets.

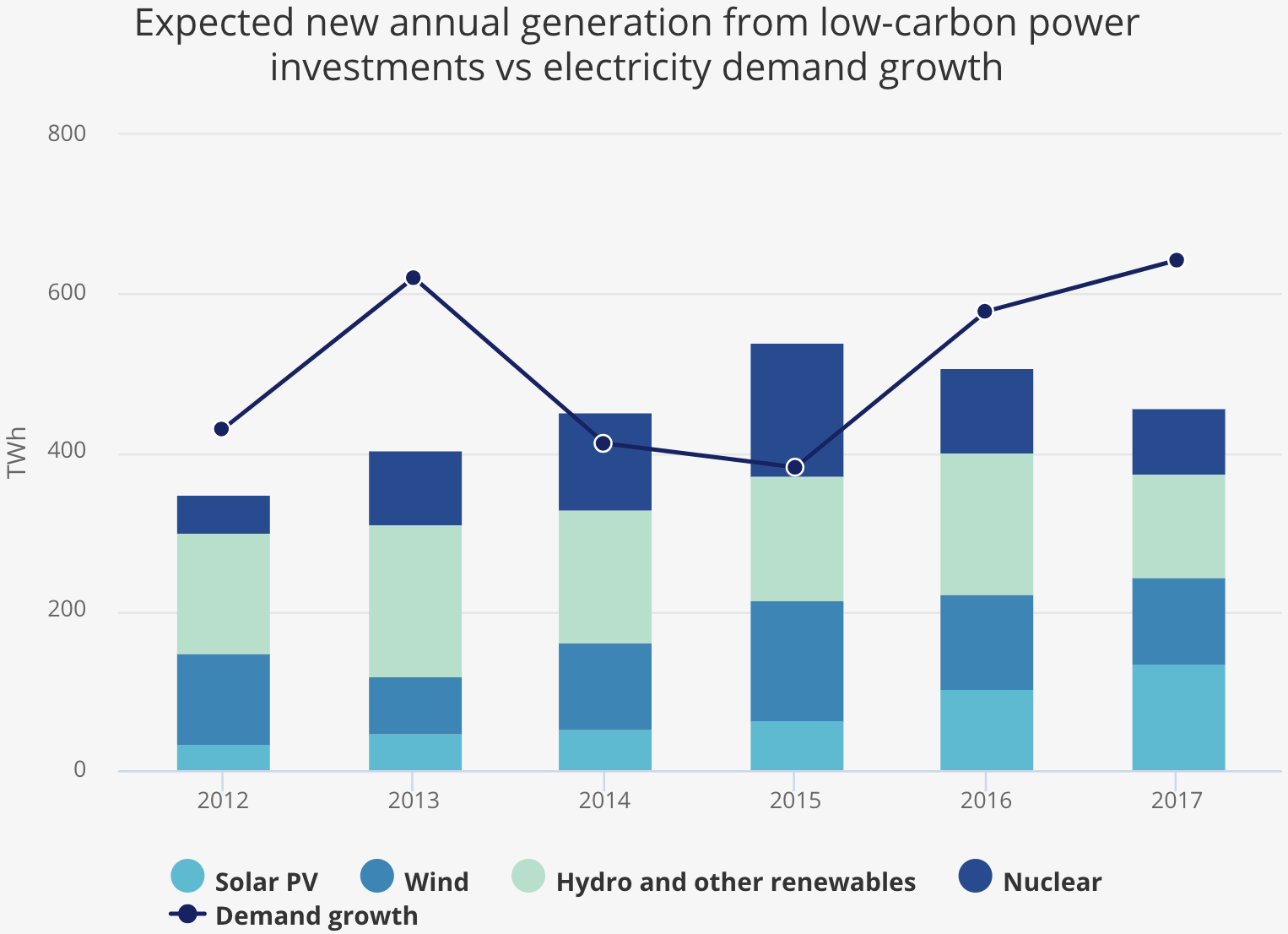

The details: Last year, notes IEA analyst Michael Waldron, was on the surface a good year for renewable power, which was two-thirds of all power generation investment amid a big expansion of solar installations and record offshore wind growth.

Yes, but: The total renewables investment still declined by 7% compared to 2016, and new capacity additions grew by only a modest 2% thanks to a slowdown in onshore wind and hydro coming online.

- And from a climate standpoint, looking at zero-carbon energy overall, it's happening alongside a steep decline in new nuclear investments.

Check out the chart above, which shows...

- "Putting all low-carbon power generation investments together, their expected new annual output fell by 10% in 2017, the second straight year of decline, and did not keep pace with demand growth," Waldron notes.

- "This spells a worrying trend for power sector-related CO2 emissions, which grew by 3% in 2017, on the back of a rise in China and India, where renewables deployment was large, but coal power filled the supply-demand gap."

The bottom line: Waldron puts the investment levels in the context of IEA's Sustainable Development Scenario, which is a future consistent with h0lding the global temperature rise under 2°C (the target of the Paris climate agreement).

- "[N]ew renewables generation needs to rise rapidly and global investment in renewable electricity needs to almost double to meet these goals, to nearly USD 550 billion per year by 2030," he writes.

2. BP and Shell signal support for carbon tax bill

3. The tail risk of the Iran escalation

Here's a question rattling around oil circles: Is the market taking Iran's threat to close a vital oil shipping chokepoint seriously enough?

Why it matters: It's a threat — which Iran has made more than once over the years — that's unlikely to happen and hugely consequential if it's carried out. It would send oil prices skyrocketing.

Driving the news: Iran in recent days has threatened to block the Strait of Hormuz, a narrow Persian Gulf channel that roughly 19 million barrels of oil from multiple nations passes through each day, or about 30% of seaborne supplies.

The threat has been part of the wider escalation of rhetorical threats and attacks between Iranian leaders and President Trump.

What they're saying: “While our military would clearly prevail over the Iranian military in a conflict, I think we ought not be complacent about how long that strait, that narrow strait, would be closed,” oil analyst Bob McNally of the Rapidan Energy Group said yesterday.

- McNally, speaking at a Senate hearing on oil, said it would take time to clear mines and have insurance companies resume shipping coverage. “That is a deadly serious issue for the oil market to consider,” he said.

- He later noted that U.S. strategic stockpiles could not be released at a rate even close to fast enough to make up for the shortfall.

The intrigue: A Financial Times column explores the topic, noting that the escalation of words between the presidents "has been met with a resigned shrug from the oil market," with little effect on prices.

Yet, FT energy editor David Sheppard cautions that the Hormuz threat needs to be taken seriously, even though it has long been seen as very unlikely:

"Though widely seen as an option of last resort for Iran, the frustration over the Trump administration’s withdrawal from the nuclear deal and fears they are pursuing a long-term policy of regime change may alter Tehran’s calculations. Relatively low probability events can have an outsized impact when they occur."

Go deeper: This Bloomberg column explores the details of Iran's capacity and planning to cut of the strait.

4. Climate and energy notes: CCS, Vatican, nuclear

5. Chart of the day

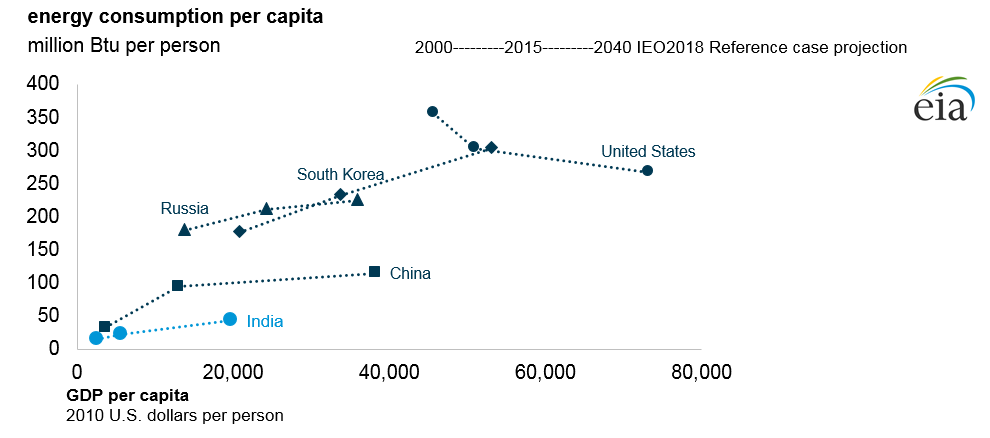

The Energy Information Administration yesterday released its latest long-term set of global energy forecasts called the International Energy Outlook.

This year's edition focuses specifically on trends and scenarios in India, China, and Africa.

Why it matters: The lines for India and China in the chart above are a helpful reminder about two dynamics...

- Those economies (and developing nations overall) are where the lion's share of energy demand growth is expected in the coming decades.

- But per-capita energy use remains far below U.S. levels, and will for the next several decades at least.

More broadly, the report explores how different trajectories for the economic and industrial mix in will affect energy use. That matters for the climate, too, because China is the world's largest greenhouse gas emitter and India is the third-largest. For instance, the report says when it comes to China...

- "Faster economic growth in China increases energy use, but the magnitude and rate depends on how quickly China transitions to a more service-oriented, personal consumption-based economy."

- "In the No Transition to services case, delivered energy consumption increases by 25% relative to the IEO2018 Reference case in 2040, compared with a 20% increase in the Fast Transition to services case."

Axios Generate

Untangle the energy industry’s biggest news stories