Axios Generate

January 02, 2018

Greetings from Spokane, Wash., where I'm wrapping up my holiday visit. I hope everyone had a great holiday season!

My latest Harder Line column looks at the top 8 issues I'm watching in 2018. What are you watching? Let me know at [email protected]. After the column, my colleague Ben Geman is going to get you up to speed on the rest of the news.

1. 8 big things to watch in 2018

Washington does not have a coherent strategy on energy and climate change, and that puts these issues all over the map, literally. Here are the headlines for issues I'm watching this year:

1. Gritty details of Trump's deregulatory efforts

2. Rubber meets the road on trade battles

3. Electricity market mayhem gets real

4. The roads from Paris and Kigali

5. Carbon tax battles heat up

6. Hunger Games of transportation

7. Oil prices hovering upward

8. Saudi Aramco IPO

Go deeper: Click in the Axios stream here to read why I'm following these issues.

2. Tax law's effect on big oil starts emerging

Breaking Tuesday: BP announced that the complicated new U.S. tax law would cause a one-time $1.5 billion hit to its upcoming Q4 earnings.

- But longer term, the steep reduction in the corporate rate from 35% to 21% would be positive for future earnings, the U.K.-based multinational with extensive U.S. operations said Tuesday.

Why it matters: The announcement is among the early signs of how the big new tax law will affect the energy sector.

ICYMI: Last week, Royal Dutch Shell similarly said that it expects the new law, notably the lower corporate rate, to be "favorable to Shell and to its U.S. operations," but also warns of a near-term hit.

- It didn't provide a specific figure, but said: "[O]n the basis of the third quarter 2017 financial statements, Shell would have incurred an estimated charge to earnings of $2.0 to 2.5 billion primarily driven by a re-measurement of its deferred tax position to reflect the lower corporate income tax rate."

* * *

State of the market: Via Reuters, "Oil prices posted their strongest opening to a year since 2014 on Tuesday, with crude rising to mid-2015 highs amid large anti-government rallies in Iran and ongoing supply cuts led by OPEC and Russia."

Hmmmmm: Last week the U.S. Energy Information Administration reported that total U.S. production was slightly over 9.75 million barrels per day in the week ending Dec. 22.

- This is actually 35,000 barrels per day less than the prior-week average, signaling the first weekly dip since Hurricane Nate took a bunch of Gulf of Mexico production temporarily offline in mid-October.

- We'll be watching to see if it's a blip or something more.

3. Tea leaves on solar trade decision

Get smart: My colleague Jonathan Swan has an inside look at White House trade policy deliberations overall. He reports that White House economic adviser Gary Cohn and Treasury Secretary Steven Mnuchin are trying to moderate Trump's hawkish impulses.

Don't forget: The White House faces a late January deadline to decide whether to impose tariffs (or perhaps some other form of restrictions) on imported solar panel equipment.

Why it matters: Two distressed panel makers pushing for tariffs say they're needed to protect the domestic panel sector from low-cost imports — including heavy volumes from Chinese-owned companies. However, the wider industry is lobbying against tariffs due to worries about impact on new projects.

The big question: If President Trump does take action on solar imports, will the penalties be large enough to badly squeeze the economics of new projects and significantly slow solar power's U.S. growth?

4. What Trump's climate tweet says (or doesn't say) about 2018

ICYMI: On Dec. 28, Trump waded back into the topic of climate change with a tweet that appeared to use the chill in the eastern U.S. to question the reality of global warming.

- The tweet got tons of media attention, and Amy noted in her piece that it "shows he's still openly mocking mainstream climate change science, even without directly questioning it."

Be smart: As Amy points out, what the administration does is more important, and not always consistent, with the missives that Trump fires off on Twitter.

- While abandoning his predecessor's emissions policies and curbing the availability of some information, the Trump administration has yet to launch the direct, frontal assault on mainstream climate science that some conservatives have clamored for.

What to watch in 2018: Two key indicators will be if EPA administrator Scott Pruitt will move ahead with his planned "red team, blue team" exercise on climate science; and, if resistance to mainstream climate science will spread further within the administration.

- As the Washington Post noted recently, there has not (yet) been any effort to alter the climate research and pronouncements of NOAA and NASA, which provide key data and other research on the topic.

5. Shale's near-term and long-term projections

A few bits and pieces on what promises to be a huge story in 2018 and beyond: the U.S. shale boom.

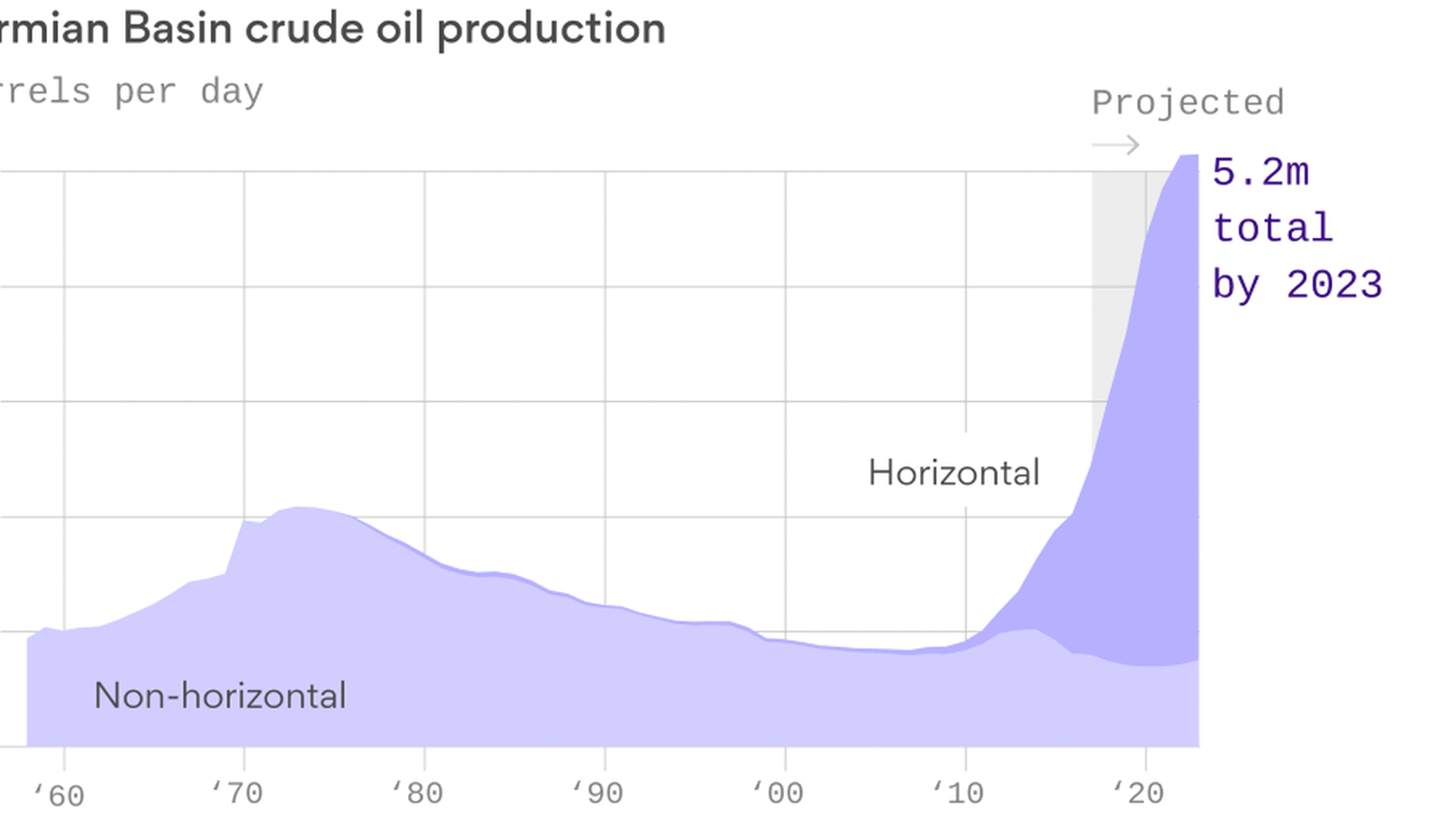

New record: A report from the consultancy IHS Markit released over the holidays concludes that the Permian Basin in Texas and New Mexico last year soared past the region's 1973 production peak to reach more than 815 million barrels of oil production, far above the '73 total of 790 million.

- Check out the chart above: It shows how the marriage of fracking and horizontal drilling enabled production to keep climbing, even during the price doldrums of 2014–2015. They see the Permian's boom helping to push total U.S. production to 10.5 million barrels per day this year, well past the prior record.

Industry's view: A few days ago the Dallas Fed released its latest quarterly survey of 132 oil-and-gas companies (a mix of E&P and service companies) active in their jurisdiction. A few takeaways:

- 2018: On average, respondents expect WTI to be $60-per-barrel at the end of this year. (Editor's note: The average forecast from 15 big investment banks polled by the Wall Street Journal is that WTI will average $54 this year).

- Longer-term projection: The average expectation for average WTI prices in the next 3–5 years is $66 per barrel. This would be enough to support expectations of continued production growth.

- Active U.S. oil rigs: 51% expect the number of active U.S. oil drilling rigs to be higher in 6 months, 46% predict it will be the same as current levels, and 3% see a drop.

- Capital spending: Just over half the execs polled expect their capital spending to rise slightly this year, another roughly 20% expect significant increases, while very few forecast decreases.

Go deeper: The New Yorker published a big feature on the Texas oil-and-gas surge that began almost a decade ago, looking at the environmental problems accompanying it and the economic impact of boom-and-bust cycles.

6. Good use of your holiday gift card (before it vanishes behind the fridge)

Good read: During our holiday newsletter hiatus, I finally had time to read Meghan O'Sullivan's book (pictured above) about how the shale boom is shaking up global oil-and-gas markets — a phenomenon that has broad and important geopolitical effects.

The boom benefits U.S. global posture and economy, but O'Sullivan warns that policymakers cannot be complacent and must take steps to harness its geo-strategic benefits while mitigating environmental risks.

Why it matters: The book offers a fascinating and lucid analysis — interspersed with interesting vignettes from O'Sullivan's globetrotting career as a Harvard energy and international affairs expert who served in the George W. Bush administration — of the many international and domestic effects of what she terms the "new energy abundance."

A couple of the interesting themes include:

- The energy abundance is putting new pressure on Russia. It won't end Europe's heavy use of Russian gas, but does alter the balance of power as European countries have more supply options and the increased LNG trade is creating more of a buyers market. It strengthens the hand of China, meanwhile, in Sino-Russian relations.

- Speaking of China, the book explores several ways it's affecting China's posture and policy. Here's one: The seismic shift from 10–15 years ago, when concern about growing competition for dwindling resources was all the rage, means there's less motivation for China to seek direct supply and equity deals with human-rights abusing regimes and shield them from international pressure. Instead, China is more comfortable relying on markets.

- Perhaps counter-intuitively, the bonanza of oil-and-gas could eventually increase overall global reliance on Middle Eastern supplies, because in a lower price environment, sources of oil in other parts of the world with high development costs are less attractive to produce.

- On climate change, she says the shale gas boom that has helped to lower U.S. emissions by displacing coal helped to bring the major 2014 U.S. emissions deal with China that paved the way for Paris a year later. Another interesting point: O'Sullivan warns that abandoning the Paris deal might ironically hurt the U.S. shale boom, because less global climate coordination could bolster coal internationally at the expense of U.S. LNG.

Go deeper: The New York Times reviewed the book last week.

Sign up for Axios Generate

Untangle the energy industry’s biggest news stories