Axios Capital

March 26, 2020

1 big thing: Keep it shut

Illustration: Sarah Grillo/Axios

Bonus: Jerome Powell's straight talk

Photo illustration: Sarah Grillo/Axios. Photo: Scott Olson/Getty Images

2. Thank you, markets

Illustration: Sarah Grillo/Axios

Bonus: The government makes markets work

Markets would have collapsed over the past couple of weeks if it weren't for the "whatever it takes" attitude of the Fed.

- The Fed's muscle memory from 2008-09 kicked in, and almost every financial crisis program was resuscitated. (Similarly, one big reason for the success of Hong Kong and Singapore in navigating this crisis is that their own memories of SARS and H1N1 kicked in very quickly.)

- Banks didn't need to be rescued this time around because after the financial crisis they were forced to take on much more capital. America's banks now have more than $1.7 trillion of "tier 1" capital — basically the amount of losses that they can easily absorb without going insolvent.

- The banks' strength has made them an important part of the government's rescue package. They are being asked to lend trillions of dollars of bailout money to small- and medium-size businesses across the country, with the loans guaranteed by the government.

Go deeper: Axios' Dion Rabouin looks at the Fed's extraordinary actions.

3. Why we need corporate welfare

Illustration: Sarah Grillo/Axios

4. Nothing can stop the stock ETF juggernaut

The week ending March 18 was one of the bloodiest in stock market history, with the S&P 500 dropping more than 12.5% and the Dow shedding 3,654 points.

- Every asset class saw outflows, per the Investment Company Institute, with investors withdrawing more than $153 billion from mutual funds and ETFs combined. Of that, the majority ($114 billion) came from bond funds, but another $12 billion left equity funds.

- The single exception — the one asset class that saw inflows, rather than outflows — was domestic equity ETFs. That's overwhelmingly S&P 500 index funds, along with their close brethren.

- By the numbers: The $9.1 billion that flowed into such funds vastly exceeded the $2.6 billion average weekly inflow during 2019.

Why it matters: Actively managed mutual funds have been hemorrhaging cash for years, and bond funds are the first place that Americans look for money when they need it in a crisis. But the set-it-and-forget-it gospel of investing passively in stocks for the long run seems to be impervious even to the threat of a second Great Depression.

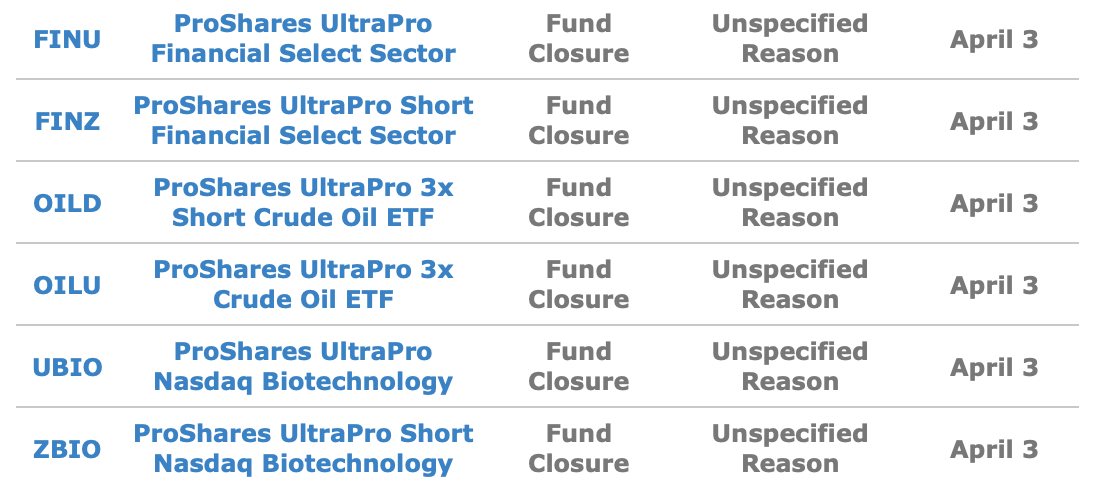

5. Goodbye and good riddance

One group of ETFs that won't be missed is the leveraged and inverse ETFs designed as gambling vehicles for day-traders.

- If you want to bet that a certain sector is going up or down on a certain day, these funds provide an easy and leveraged way to do so. But far too many investors hold them for much longer than a day, which is a recipe for disaster.

- The recent stock market volatility has wiped out a whole swath of these funds. I'm picking on the six here just because they come in pairs: the long ETFs and the short ETFs are both going out of business at the same time.

6. Coming up: Shaken consumer confidence

Illustration: Eniola Odetunde/Axios

7. Building of the week: The Javits Center

Photo: Noam Galai/WireImage

Axios Capital

Learn about all the ways that money drives the world