Axios Crypto

May 15, 2025

1 big thing: 💳 Mastercard's master plan

2. State of play: Stablecoin legislation

3. Charted: Ethereum leveled up

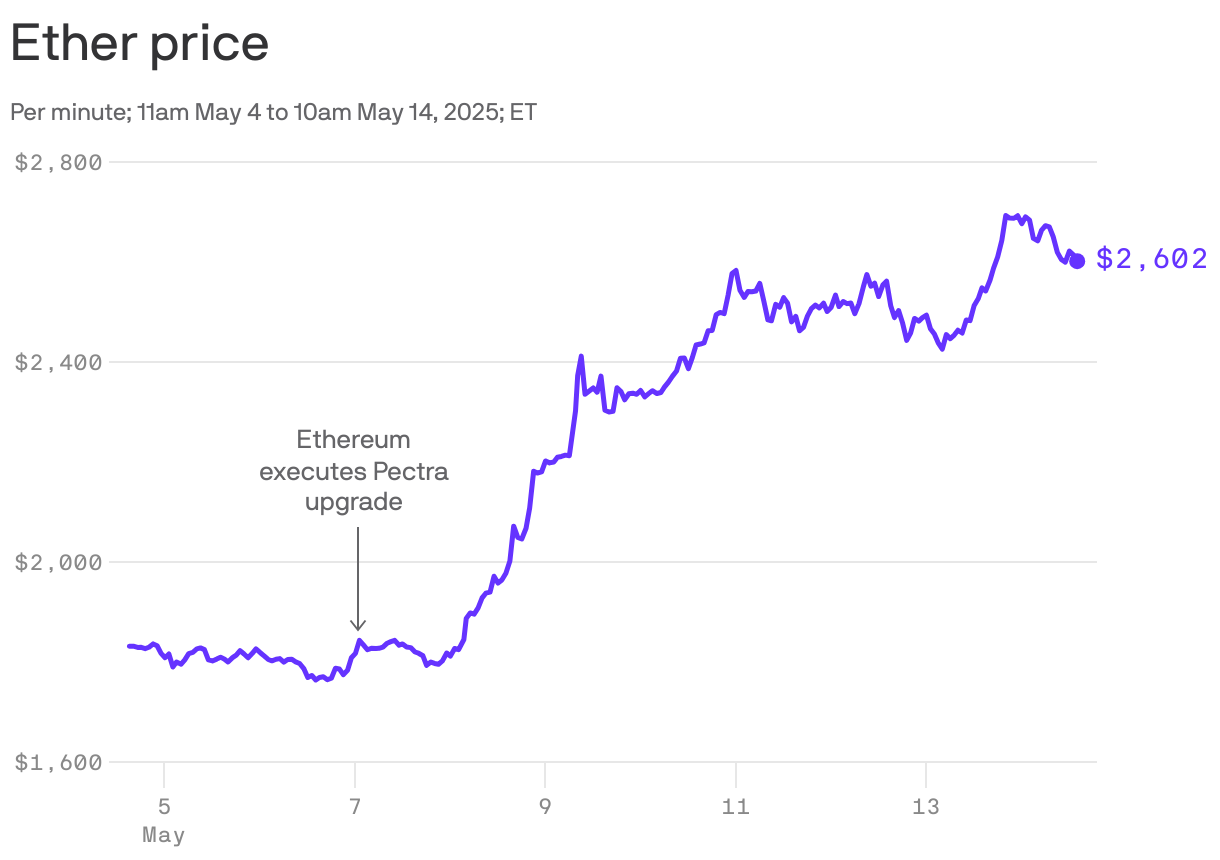

We haven't focused on coin prices too much in these pages lately, but it would be crazy to ignore the fact that Ethereum's coin, ether (ETH), is up like 40% in recent days.

The big picture: The second-largest blockchain has been adapting to what its most avid users want and is working to drive value back to the core change.

Between the lines: I like to say that you never know what changes prices in this world, but it's pretty clear that the recent Pectra upgrade on Ethereum did it, and the increased value has held now for a week (which in crypto time is months).

- Pectra did a bunch of wonky things mostly for superusers, such as making staking more flexible and improving how layer-2 blockchains communicate with Ethereum proper.

- Long story short: It's working.

Zoom out: Another topic we haven't covered here, but that this fits into: The leadership at the Ethereum Foundation has changed.

- Ethereum isn't a company, so no one is 100% in charge, but the Ethereum Foundation is sort of the chief cat herder for the blockchain.

- It's re-focusd on projects and evolution in Ethereum that will drive value to its investors rather than aiming for pie in the sky, utopian dreams.

By the numbers: ETHBTC, the ratio of ETH price to that of bitcoin, is down 46% over the last year.

- But it's up since Pectra.

- Since BTC effectively functions as an index of the whole crypto market, Ethereum fans would hope that their coin at least goes up at roughly the same rate as bitcoin, but it's been just the opposite for a while now.

4. Catch up quick

5. By the numbers: $21 million in losses

Axios Crypto