Axios Crypto

February 10, 2023

🦑 1 big thing: Kraken settles

Illustration: Aïda Amer/Axios

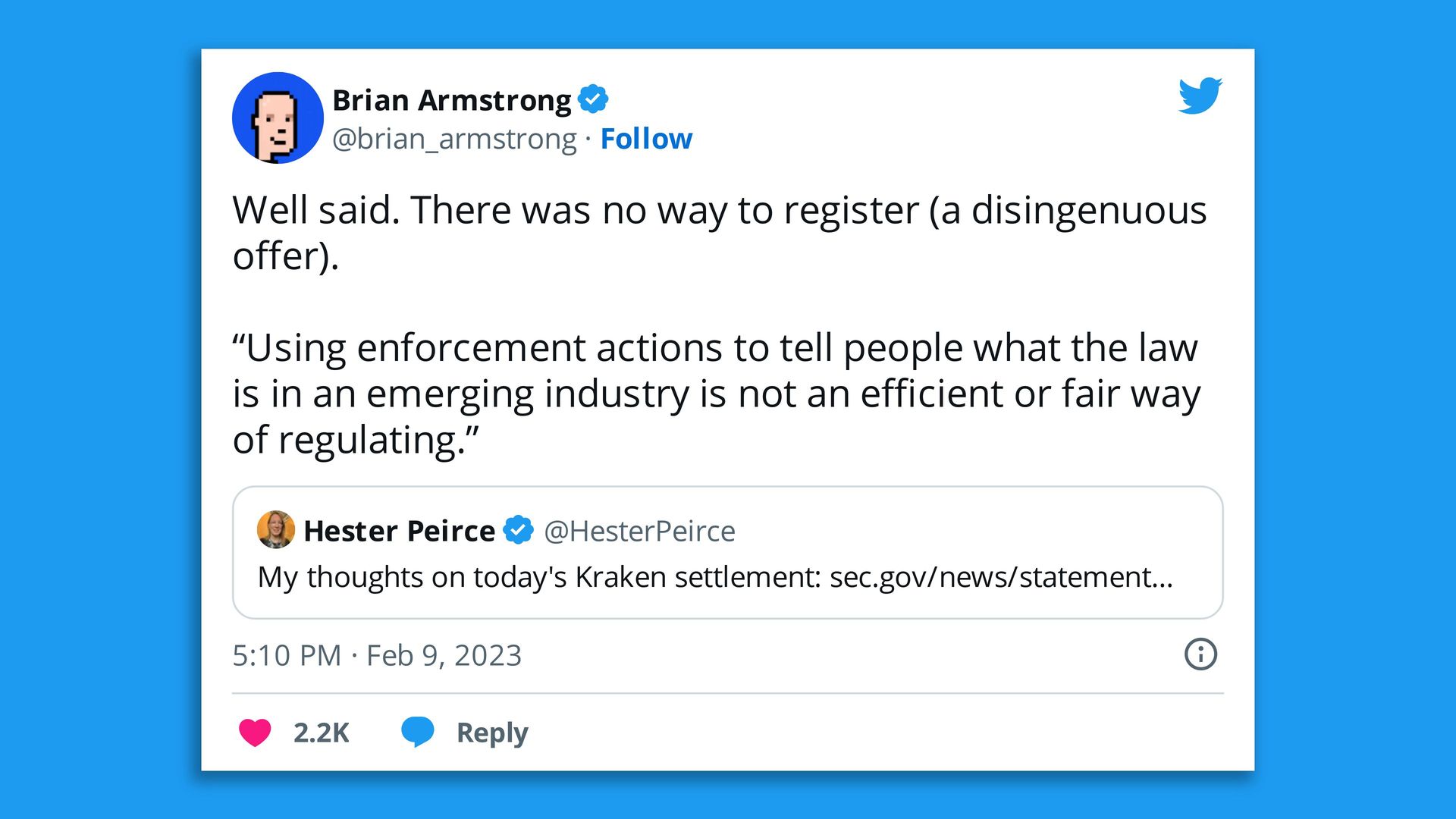

🪰 2. Culture hash: Dissenters

Screenshot: @brian_armstrong (Twitter)

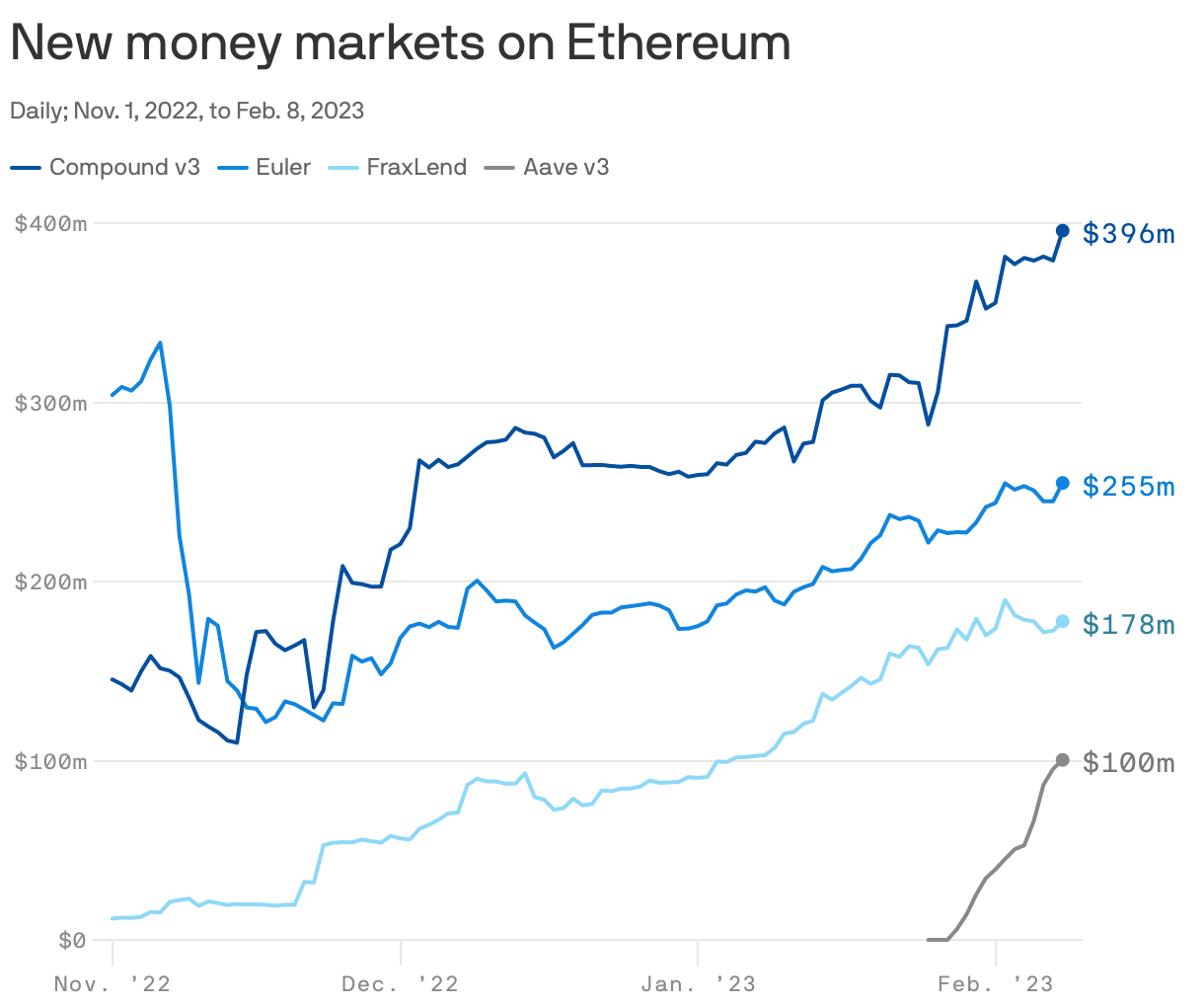

🏧 3. Charted: Lending on chain

There are many blockchains and lots of applications for lending and borrowing cryptocurrency, but Ethereum remains the home for decentralized finance (or DeFi), Brady writes.

- Lately, a lot of the standard bearers of lending have been making new versions of their savings-and-loan protocols.

- Some of them have been adding features. Others are taking them away. More on all that below.

Of note: Aave v3 is the biggest of all of these protocols, but only if you add in other blockchains.

- Aave decided to test its latest version on other chains first, only just arriving on Ethereum late last month.

By the numbers: There is just about a billion dollars in these four "small" projects. This time in 2020, all of DeFi broke $1 billion for the first time (entirely on Ethereum).

- Today, DeFiLlama puts DeFi at $47 billion, across multiple blockchains.

🐣 4. The new and interesting money markets

Illustration: Shoshana Gordon/Axios

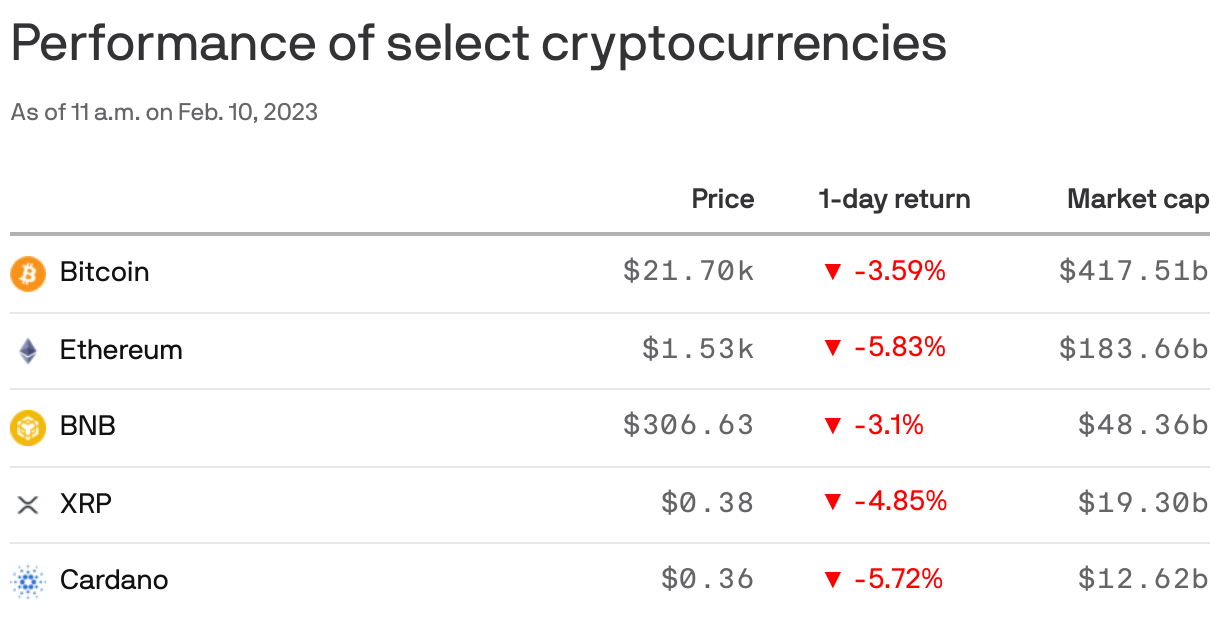

🪃 5. Catch up quick

Top coins

Axios Crypto

Brady Dale covers crypto and blockchain impacts on markets and regulation.