Axios Crypto

December 16, 2022

🇺🇸 1 big thing: No financial privacy on the chains

Illustration: Sarah Grillo/Axios

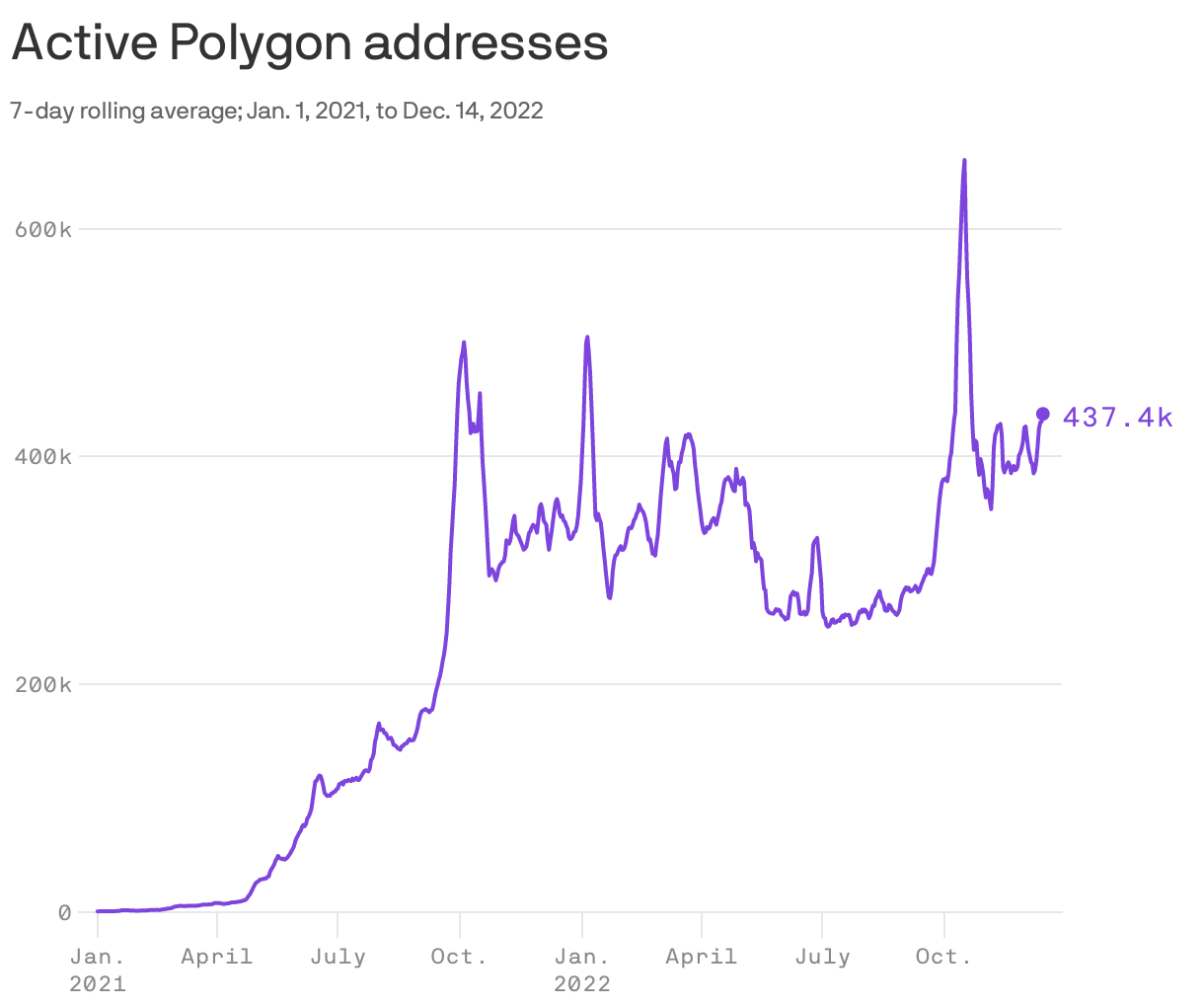

🍊 2. Charted: Polygon is getting YUGE

Open embedded content from datawrapper.dwcdn.net

Open embedded content from datawrapper.dwcdn.netThe blockchain chosen by the company that won the right to license former President Trump's image for an NFT series was Polygon, Brady writes.

- Polygon stands on its own, but it was built to complement Ethereum. The two chains interoperate as easily as is technically possible, and they run similarly.

Driving the news: Above and beyond the recent series of presidential collectibles, Polygon is generally growing, despite the crypto downturn.

By the numbers: Active addresses depends on what buzzy releases are attracting users, so it varies a lot. At the height of the bull market, daily active addresses was about 215,000 to 300,000 each day.

- These days, a typical day is more like 330,000 to 420,000 active addresses.

- Unique addresses are also up 40% since the market crashed in May.

Of note: Polygon is much, much cheaper to use than Ethereum. Everything still costs something, but it's so much less that users are more likely to experiment and play on it.

The bottom line: The market is in terrible shape but that doesn't mean users have completely left.

🗽 3. The hardest state for crypto biz is harder now

Adrienne Harris, superintendent of the New York State Department of Financial Services. Photo: Christopher Goodney/Getty

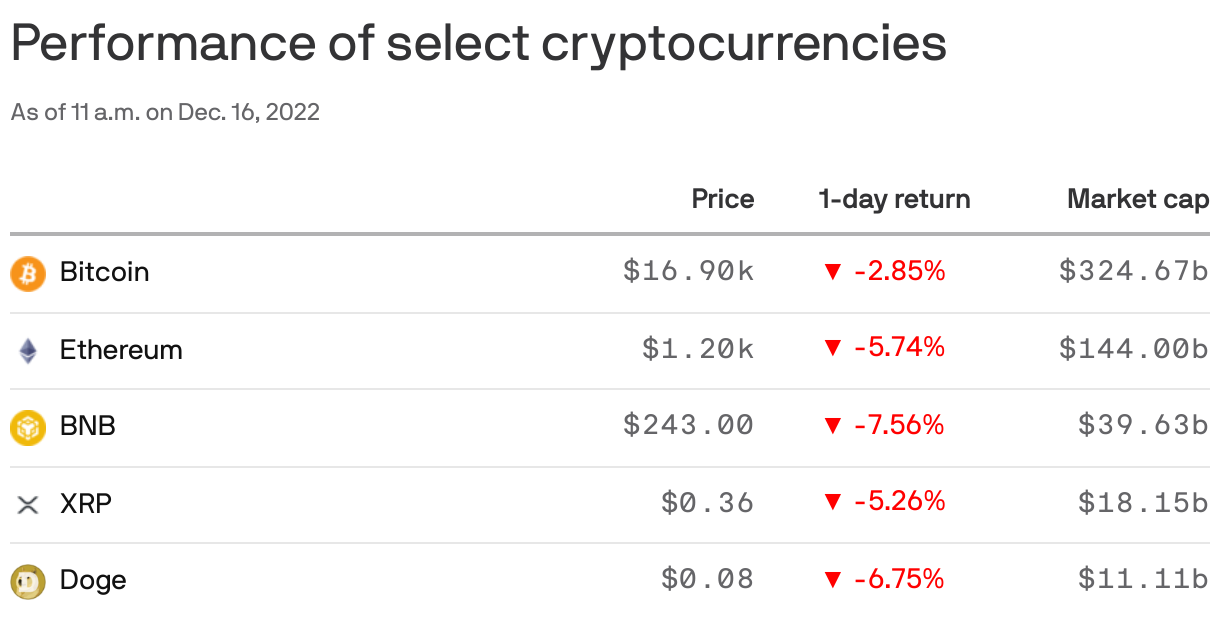

🛼 4. Catch up quick

Top coins

Open embedded content from datawrapper.dwcdn.net

Open embedded content from datawrapper.dwcdn.net🍻 5. Culture hash: New York's bitcoin bar

Does that sign look familiar? PubKey bar in New York. Photo: Crystal Kim/Axios

Axios Crypto

Brady Dale covers crypto and blockchain impacts on markets and regulation.