Axios Crypto

June 24, 2025

Good morning! Pro Rata's Dan Primack has an intriguing story on the defunct venture fund that won big on Circle's IPO, and, meanwhile, we turn to the states.

- 📬 Email: [email protected]

Today's newsletter is 1,282 words, a 5-minute read.

1 big thing: Red and blue ATM regulation

/2025/06/24/1750771738235.gif?w=3840)

States across the U.S. are rolling out tough laws that cap deposits and tighten oversight on cryptocurrency ATMs, seeking to cut off a favorite tool of scammers and extortionists.

Why it matters: The kiosks are the easiest way for ordinary people to turn cash into crypto, and their use by fraudsters has surged over the last few years, especially with scams targeting older Americans.

The latest: This month, the Illinois legislature sent SB2319 to Gov. JB Pritzker, who called for such legislation early in the year.

- Among other things, the law would require crypto ATM operators to include details on every receipt — such as the blockchain address where funds are sent — that would help law enforcement with any future fraud investigation.

- Sen. Dick Durbin (D-Ill.) tried to amend a related measure into the legislation the Senate just passed on stablecoins, but the effort failed.

How it works: Cryptocurrency provides criminals with a way to receive money that a third party can't roll back, because it works like cash. Once a person has a digital token, it's theirs.

- So, whether they have managed to put a padlock on all of a person's digital files or persuaded them that they are the IRS and needed payment sent ASAP, scammers often turn to cryptocurrency.

- That's why a new law signed yesterday in Rhode Island would require big warnings about the irreversibility of crypto transactions on every kiosk.

Between the lines: These kiosks have popped up all over the country, and fraud losses have grown along with them.

- Reported losses tied to schemes involving crypto kiosks jumped nearly 10x from 2020 to 2023, the FTC reported last September. And the FBI reported $247 million in losses tied to the fraud complaints involving kiosks in 2024.

State of play: In response, states have passed bills with different mixes of protection for consumers making their first (and probably last) crypto transaction using one of these ubiquitous kiosks.

- Vermont passed a law in May. It puts a daily limit on use for these machines — pulling back the throttle on how much criminals can gouge victims.

- Nebraska stamped a law in March that establishes a licensing system for crypto ATM operators. Nebraska has been eager to bring crypto business to the state.

- Arizona, which also enacted a bitcoin reserve fund, established a law in May that requires refunds on fraudulently induced transactions.

Zoom out: AARP, which has been urging state legislators to pass these bills, says that they have endorsed 12 bills that have passed.

Cities have also honed in. The City of Spokane, Washington, voted to ban all crypto kiosks on June 16. And crypto ATMs have been a topic in Minnesota cities including St. Paul, Stillwater and Forest Lake.

Follow the money: Crypto ATMs — which allow crypto holders to convert their digital assets into cash, and vice versa — can be a strong business. Bitcoin Depot, one operator, reported a margin of 20% on $33 million in profits for the first quarter.

The bottom line: This is a trend that's reaching red and blue states.

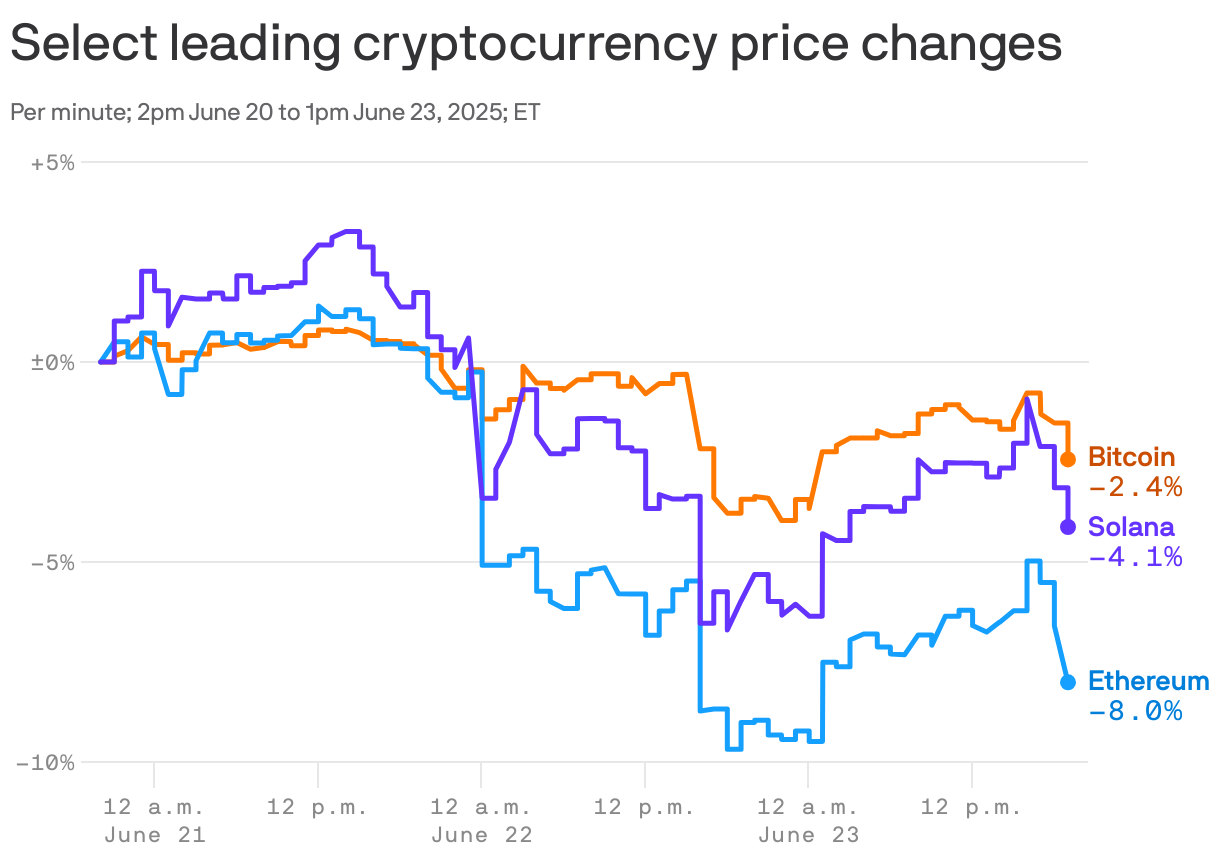

2. Charted: Bitcoin shrugs at Middle East bombings

It was surprising to see how little bitcoin price reacted to the news that the U.S. had bombed Iran's nuclear facilities.

- Price dipped as news came out of the bombing and again as Iran promised to respond.

Yes, but: Oil price response was also muted, and that's much more closely tied to the region.

Zoom in: Bitcoin had the weakest reaction overall. It briefly dipped below the $100,000 mark during the weekend, but was back over by yesterday.

The latest: Yesterday afternoon, as Iran initiated retaliatory responses against U.S. bases, major cryptocurrencies actually rose in value.

- Traders likely viewed those responses as a sign that Iran would not initiate a protracted campaign.

- Bitcoin is trading around $105,350 as we send this.

3. Reputational risk, REKT

The Federal Reserve has removed "reputational risk" from its manuals explaining how its staff should assess the soundness of banks.

Why it matters: This is not only a nail in the coffin for the unofficial government effort critics dubbed "Operation Chokepoint 2.0," it will also make it harder for any other such efforts to be quietly implemented by a future administration.

Catch up fast: This year, as the Congress started digging into the question of banks discriminating against crypto firms, a clear policy tool emerged as a means to execute a campaign against an industry: reputational risk.

- Sen. Cynthia Lummis (R-Wyo.) had a placard printed for a Senate banking committee meeting where she showed the concept spelled out in a Fed manual, its "Account Access Implementation Handbook."

The big picture: Prudential regulators have broad discretion to ask tough questions about the riskiness of financial products, in dollars and cents terms.

Yes, but: They also had this loose category called reputational risk, where they could raise questions like, for example: "Would serving this industry make the bank look less trustworthy, making other customers want to leave it?"

- Customers leaving is, after all, a systemic question. A bank can't handle too many people leaving too quickly.

- But as hearings we covered early on illuminated, there was a lot of leeway for interpretation.

What they're saying: "This change does not alter the Board's expectation that banks maintain strong risk management to ensure safety and soundness and compliance with law and regulation," the Fed wrote in its statement yesterday.

What's next: The Fed also announced it plans to train staff to make sure they are clear on the policy change.

4. Fiserv's stablecoin

Another major firm has entered the stablecoin economy, the payments giant Fiserv.

Why it matters: Fiserv is a 40-year-old firm wired into the economy of 100 countries, directly serving thousands of merchants and a slew of global financial institutions.

- Stablecoins look set to go mainstream this year, with the U.S. Congress finally taking action to create clear rules for the instruments.

Driving the news: The $96 billion company announced its intention yesterday to launch its own stablecoin, FIUSD.

- "We're working to get into the arena by helping customers that we already work with be able to access digital assets as a form of payment," Sunil Sachdev, Fiserv's embedded finance lead, tells Axios.

Between the lines: Fiserv is looking to give its customers more options for payment and treasury management.

How it works: FIUSD will run on the Solana blockchain, accessible to regular people and institutions alike.

- Under the hood, it will run on existing stablecoin infrastructure, likely either Circle's USDC or Paxos' USDG (or both).

- Fiserv will rebrand these tokens to FIUSD to give its customers confidence, but it will also add some features to the token that will work well with its existing system.

- Particularly, it plans to wrap more data into each transaction with FIUSD, which they believe will make it more useful for their customers.

Fiserv also announced plans to make FIUSD interoperable with PayPal's PYUSD. Sachdev explained that this basically means "convertibility."

- The blockchain-based stablecoin USDS, of the Sky Network, does something similar with Circle's USDC, via what it calls its "peg stability module."

What we're watching: If the FIUSD plan works well, Fiserv won't stop here. Tokenized deposits are a likely next step. After that, they could get into on chain services.

The intrigue: What's attracted most companies to the stablecoin space is seeing the dramatic profits issuers generated off the massive reserves that insure its peg.

- That's not Fiserv's plan, so far. By using other companies' stablecoins, they are passing on the opportunity to earn those returns if FIUSD becomes popular.

The bottom line: "We're not looking to make money off of yield," Sachdev said.

- "We want to unlock commerce with stablecoins."

The latest: Mastercard announced today it would use Fiserv's new stablecoin.

This newsletter was edited by Pete Gannon and copy edited by Carolyn DiPaolo.

Editor's note: The 1 big thing in Tuesday's newsletter last week was corrected to reflect that Donald Trump Jr. and Eric Trump (and not President Trump) were listed as shareholders in Dominari as of April 15 (not at the end of last year).

Sign up for Axios Crypto