Axios Crypto

November 08, 2022

💣 1 big thing: Binance to acquire FTX

Photo illustration: Gabriella Turrisi/Axios. Photo: Tom Williams/CQ-Roll Call, Inc via Getty Images

🔗 2. Bonus charted: FTT's fall

FTX's exchange token FTT tanked over the past 24 hours leading to today's announcement, Brady writes.

What is FTT: It grants its holders discounts on trading and a way to share in the revenue of the exchange.

- Its price was over $80 last September, but, lately, it has traded between $22 and $26, until just recently.

- The price collapse was kicked off by Binance announcing it would sell its FTT holdings.

- The price of FTT recovered modestly this afternoon on the news of a deal between the exchanges.

What's next: The fate of FTT holders remains to be seen.

- Binance also has an exchange token, BNB, the fourth largest cryptocurrency in the world.

🚧 3. OpenSea's royalty code

Illustration: Aïda Amer/Axios

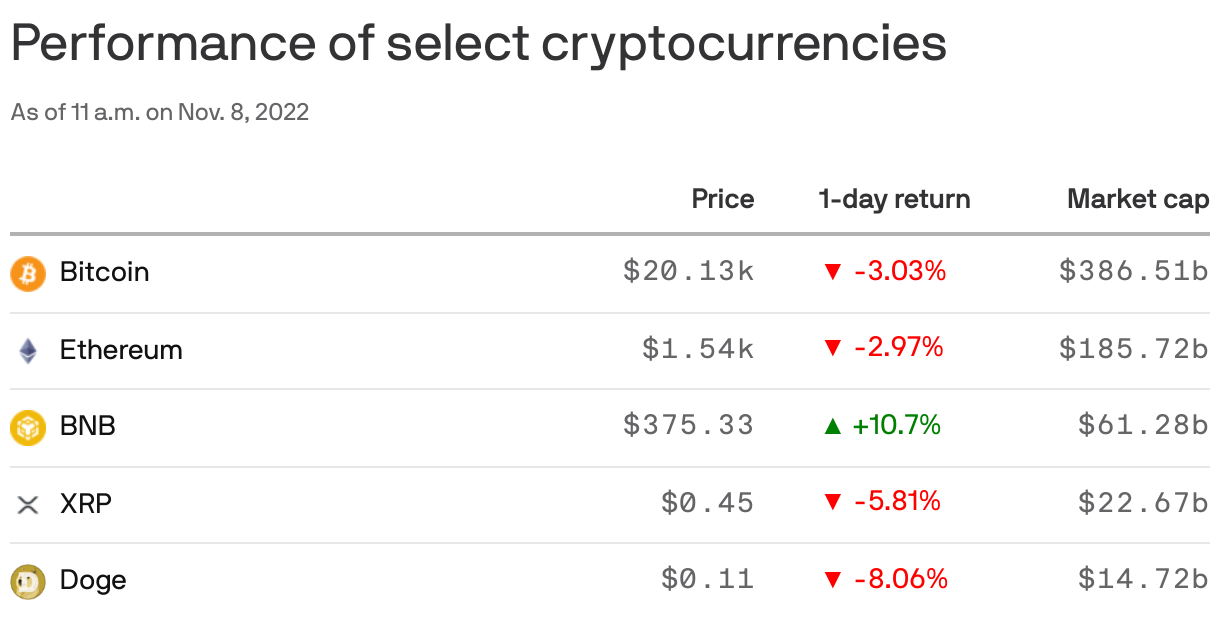

🐇 4. Catch up quick

Top coins

🌒 5. Culture hash: FTX's blood moon

Source: Twitter @gegelsmr4

Axios Crypto

Brady Dale covers crypto and blockchain impacts on markets and regulation.