Axios Crypto

August 16, 2022

Hello! The Tornado Cash saga continues to play out. We look at one small case and the door to crypto companies cracking open at the Fed.

- How much do you care about financial privacy? Tell us: [email protected].

This newsletter was edited by Pete Gannon and is 1,136 words, a 4-minute read.

🕊 1 big thing: Two crypto donations, one protest

Photo illustration: Sarah Grillo/Axios. Photo courtesy Omid Malekan

A business professor, Omid Malekan, made donations to Planned Parenthood and Russians secretly aiding Ukrainian refugees to protest the U.S. Treasury.

- He made them using Tornado Cash, the recently sanctioned privacy application that runs autonomously on the Ethereum blockchain. He logged both donations on Twitter, Brady writes.

Driving the news: Since the application has been sanctioned, Malekan, as a resident and citizen of the U.S., may have broken the law by using the service.

- Tornado Cash hides who the sender and receiver are in an Ethereum transaction.

Why it matters: The right to transact freely is personal to Malekan. "I am originally Iranian. One of the reasons my family immigrated to America was because of the kinds of rights here that you don't get many other places," he says.

- Go deeper: In his book, "Re-Architecting Trust," released in July, Malekan argues that by using the financial system to advance its foreign policy goals, the U.S. could be driving crypto adoption in many other places.

What they're saying: Financial companies have to "assume everyone is a money launderer, drug dealer or tax evader. And then they have to go through this risk-based process and make sure you are not," Malekan explains.

- Rules around anti-money laundering have turned finance "into one of the few industries that is built on a presumption of guilt," he says.

- No one checks to make sure you never shoplifted before letting you enter the supermarket, he says.

Yes, but: As we all know, Chainalysis estimated that something like $14 billion in illicit funds moved over the blockchains in 2021.

- Meanwhile, the UN estimates that there could be $2 trillion in money laundering crossing traditional networks annually.

To Malekan, the cost of fighting this losing battle is shutting people out of the financial system. It's the poorest and the most marginalized who can't get approved to use it, he said.

- "To me, it's like the war on drugs. We spent a lot of money, but we didn't stop people from getting drugs," he says.

In the weeds: Malekan didn't retain an attorney in advance of making his protest, but he did talk to a couple of attorney friends informally.

- "They agreed that the chances of the government actually prosecuting me for anything were low, but also they weren't zero," he says.

What he's watching: "I think the ramifications for non-crypto people is actually bigger than for crypto people because we have now crossed the line from people who deal with sanctioned companies or governments to criminalizing the act of seeking privacy," Malekan says.

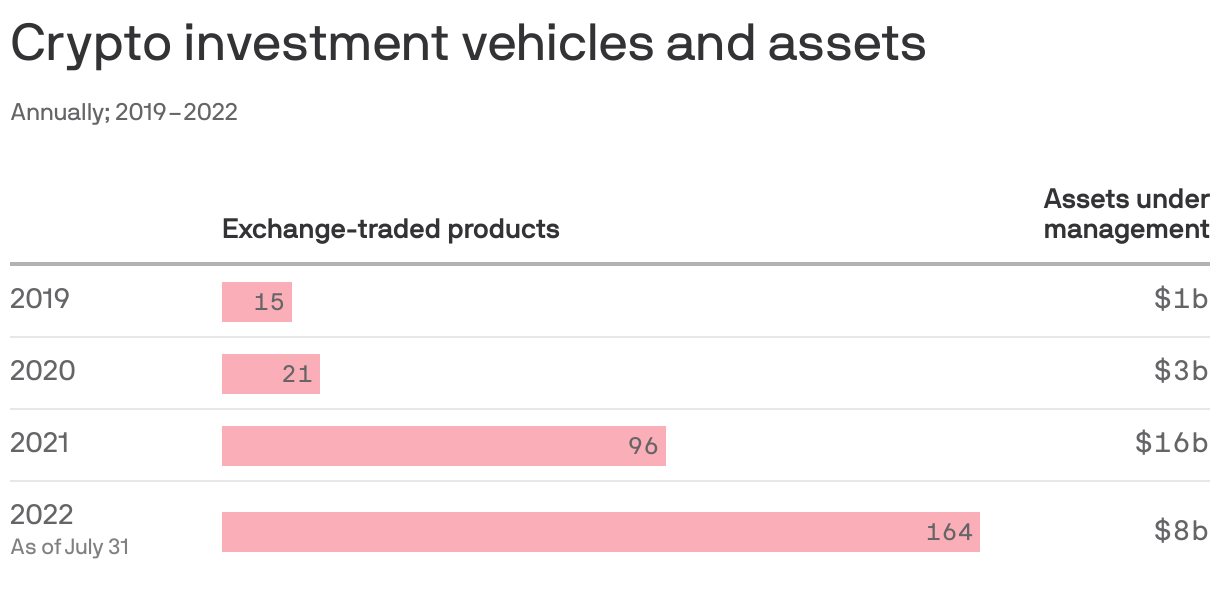

🌊 2. Charted: Money moves

Total assets invested in crypto funds globally rose 38.7% in July for the year, to $8.4 billion, according to data research firm ETFGI, Crystal writes.

The big picture: Net inflows of $727 million this year are a fraction of last year's $4.07 billion over the same period. But they are also the second highest inflows the industry has seen, ever.

- Money is flowing into crypto amid the winter.

The intrigue: Total assets across investment funds have been cut in half from 2021 amid price drops, yet the number of access points to crypto has spiked to 164 at July end from 96 at the end of last year, ETFGI data show.

📏 3. The Fed beckons

Illustration: Shoshana Gordon/Axios

The Federal Reserve Board yesterday announced final guidelines that could open a path for institutions peddling new types of financial products, or those with novel charters, to tap into the banking system, Crystal writes.

Why it matters: The guidelines seek to clarify a longstanding question critical to the crypto industry — who is allowed to have a master account.

- Such accounts would allow crypto banks and fintech platforms to access the central bank's rails (payments and services) without partnering with a traditional bank.

Of note: Wyoming-based Custodia Bank sued the Federal Reserve Board of Governors and the Federal Reserve Bank of Kansas City in June for what it called "Kafkaesque" delays to its application for one.

- Their response is due today (Tuesday).

The big picture: There has been a pressure cooker of activity as of late related to the issue of master accounts.

- Sen. Pat Toomey (R-Pa.) sent a letter in June asking about Colorado fintech firm Reserve Trust, which received a master account that was later revoked.

- When the guidelines were first proposed, the customary comment period drew an outsized response — 46 individual comment letters and 281 duplicate form letters — that generally fit two buckets, according to the Fed, for and against.

- A crypto bill proposed by Senators Cynthia Lummis (R-Wyo.) and Kirsten Gillibrand (D-NY) included a provision that would entitle any depository institution with a state charter to an account at the Federal Reserve, a detail that struck a nerve with banks.

What they're saying: "The new guidelines provide a consistent and transparent process to evaluate requests for Federal Reserve accounts and access to payment services in order to support a safe, inclusive, and innovative payment system," Federal Reserve vice chair Lael Brainard said in a statement.

Details: The new guidelines include a tiered review framework that reserve banks will apply to different types of institutions with varying degrees of risk, according to a statement.

- The guidelines originally proposed include six principles for reserve banks to evaluate requests for master accounts, otherwise, each application will be considered on a case-by-case basis.

The bottom line: The Federal Reserve Board doesn't lay out what to do for specific charters, rather, they establish tiers indicating the level of scrutiny an entity in that tier can expect.

- For those in the third tier — those not federally insured and not subject to supervision by a federal banking agency — the level of scrutiny described is "highest."

⛵️ 4. Catch up quick

🚨 Singapore-based crypto lender Hodlnaut filed for judicial management, a mechanism for distressed companies there to rehabilitate their businesses. (Hodlnaut)

⚖️ Celsius Network is expected to present its path forward during its second-day hearing to take place at 2pm ET today.

🛑 China internet giant Tencent halted digital collectible releases on its NFT platform amid heightened regulatory scrutiny. (Reuters)

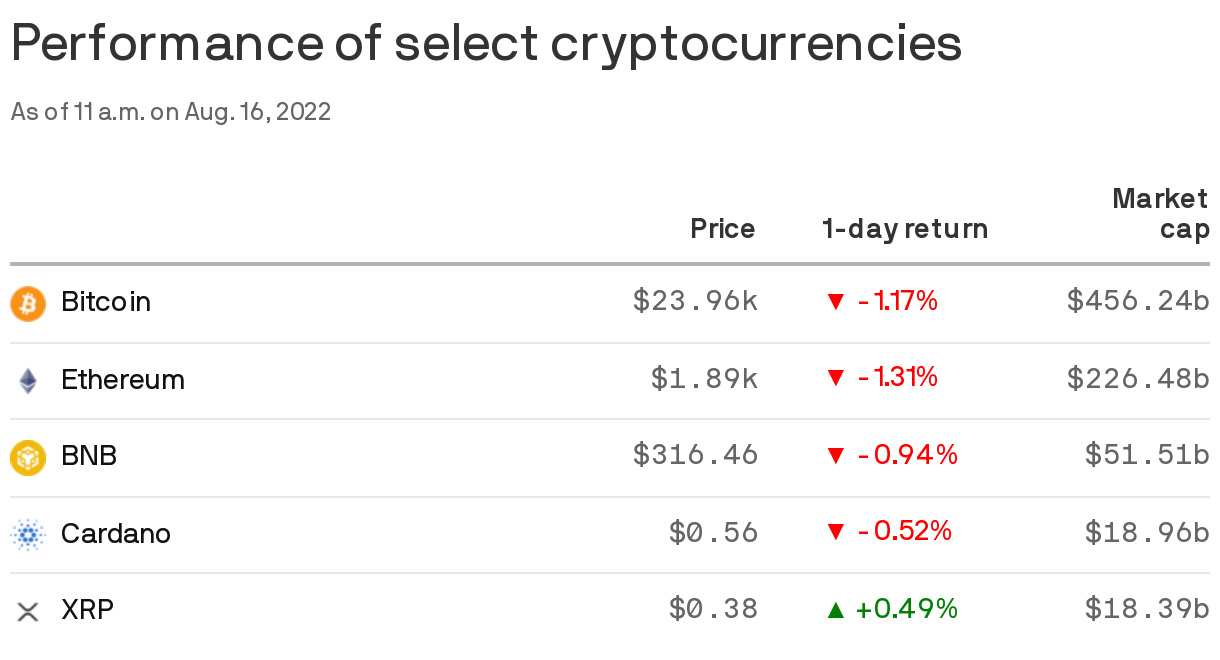

Top coins

🇦🇷 5. Culture hash: Black-market exchanges

Illustration: Sarah Grillo/Axios

Where the state-backed currency's decline is all but certain, and strict capital controls prevent easy flow of U.S. dollars across borders, crypto is proving to be a saving grace, Crystal writes.

- That's why people in Argentina appear to be embracing crypto, even if some don't know that they are.

Context: The ARS, or Argentinian peso, has a pegged exchange rate set by government mandate, so its value is almost always overstated.

How it works: Some enterprising folks hold bitcoin outright to avoid government-backed money, others use cuevas, or "caves" in Spanish, that function as underground currency exchanges.

- These exchanges sometimes use stablecoins to move and transfer currencies across borders, bypassing government scrutiny as well as thieves.

The bottom line: In places where distrust of financial systems reigns supreme, the utility of crypto shines.

What's more noteworthy: folks bringing crypto into established banking systems or folks using crypto to break from them? —C & B

Sign up for Axios Crypto

Brady Dale covers crypto and blockchain impacts on markets and regulation.