Axios Capital

June 03, 2021

1 big thing: Your inflation may vary

Illustration: Aïda Amer/Axios

2. The return of the storytellers

Illustration: Annelise Capossela/Axios

Bonus: The AMC rocketship

More than 760 million AMC shares were traded on Wednesday, with a total volume of $47.6 billion.

- Context: AMC hasn't had a profitable quarter since Q2 2019, when it made $49 million. It only has 500 million shares in total outstanding.

- Its market value at the beginning of the year was less than $500 million. That number rose to more than $30 billion at market close on Wednesday, or about 200 times its first-quarter revenues.

3. The perils of financial advice

Illustration: Aïda Amer/Axios

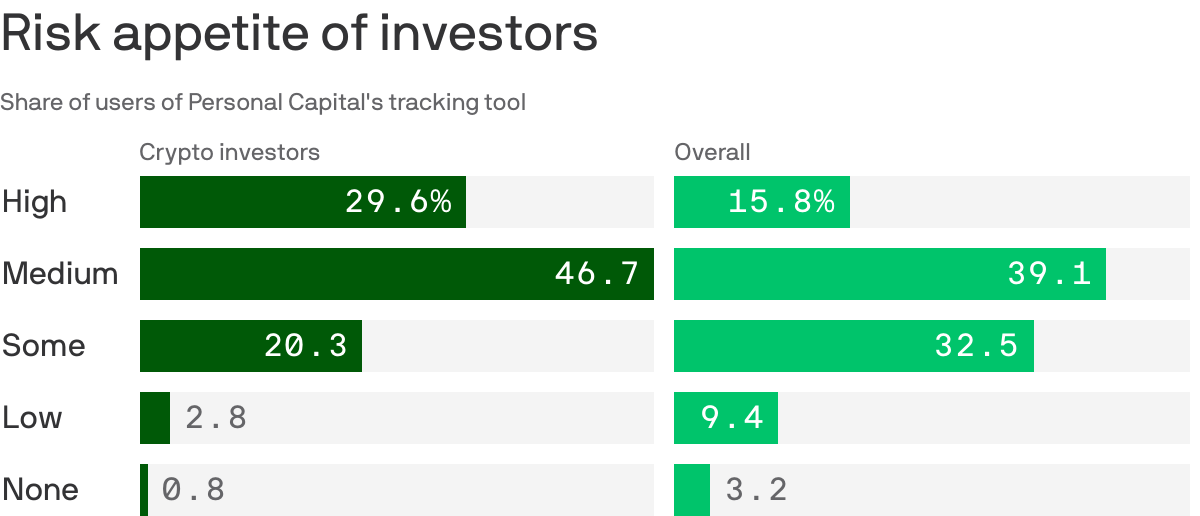

4. What crypto investors look like

Crypto isn't just for high-risk YOLO traders any more.

How it works: Of the 2 million or so investors who have signed up to track their portfolios at Personal Capital, about 17,000 have also taken advantage of a trial program that allows them to manually input their crypto holdings.

- By the numbers: The median amount of crypto held is $7,000, which works out to about 3.5% of the users' total investments.

- Crypto holders do have slightly riskier investments overall, but not massively. While 30% are high-risk investors, another 20% fall into Personal Capital's relatively conservative "some risk" bucket.

The bottom line: At least some crypto investors seem to have embraced the idea that bitcoin and its digital brethren are conservative inflation hedges, rather than high-risk speculative investments.

5. The post-Libor mess

Illustration: Sarah Grillo/Axios

6. Thrifty gateway

The global used-clothes market is worth $40 billion per year, according to Boston Consulting Group, and is growing at more than 15% per year. Like all other retail, it's moving increasingly online.

- Driving the news: Etsy announced this week that it was buying UK-based Depop, a fashion reseller beloved by #teens, for $1.6 billion.

Etsy itself, now boasting a market valuation of more than $20 billion, has no shortage of secondhand clothing, although its audience skews older.

- American fashion resellers Poshmark, ThredUp, and RealReal have all now gone public; European rivals Vinted and Vestiaire have both recently raised money at unicorn-level valuations.

Be smart: All of these platforms have benefited to some extent from speculative activity — people buying items in the hope that they will be able to resell them at a higher price. Another unicorn, StockX, specializes in such trades.

- Depop, however, is mostly an app for the discovery and purchase of items that don't look like they were found at a chain store in the local shopping mall. It's less about collectible handbags, and more about enabling self-expression.

- Used clothes, and items hand-made by influencers, are also much more socially and environmentally responsible than fast fashion.

7. Coming up: The May jobs report

Illustration: Brendan Lynch/Axios

8. Building of the week: Highfield House, Dorsington

Photo via Savills

Axios Capital

Learn about all the ways that money drives the world