Axios Capital

February 25, 2021

1 big thing: The NFT frenzy

Illustration: Aïda Amer/Axios

2. Why it's happening now

Illustration: Eniola Odetunde/Axios

3. Payments failures

Illustration: Aïda Amer/Axios

Modern capitalism runs on a smooth global electronic payments system that works in an efficient and predictable manner. That system is beginning to show cracks.

Driving the news: The majority of the U.S. payments infrastructure came to a shuddering halt on Wednesday when a "Federal Reserve operational error" caused a whole slew of services to stop working.

- ACH went down, which covers most transfers in and out of bank accounts, along with Check21, which covers checks; FedCash; and more.

- Fedwire — the self-described "premier electronic funds-transfer service that banks, businesses and government agencies rely on for mission-critical, same-day transactions" — also went down.

Between the lines: The Fed is unlikely to give much public explanation of what went wrong. CNBC's David Faber, however, reported that the Fed did try turning the system off and on again — and that didn't work.

Flashback: One layer up from the public payments infrastructure are private payments protocols, which are also brittle and prone to error.

- Last August, Citibank accidentally wired $894 million to a group of Revlon creditors. Adding insult to injury, a judge ruled this month that the creditors who didn't voluntarily return the money were allowed to keep it.

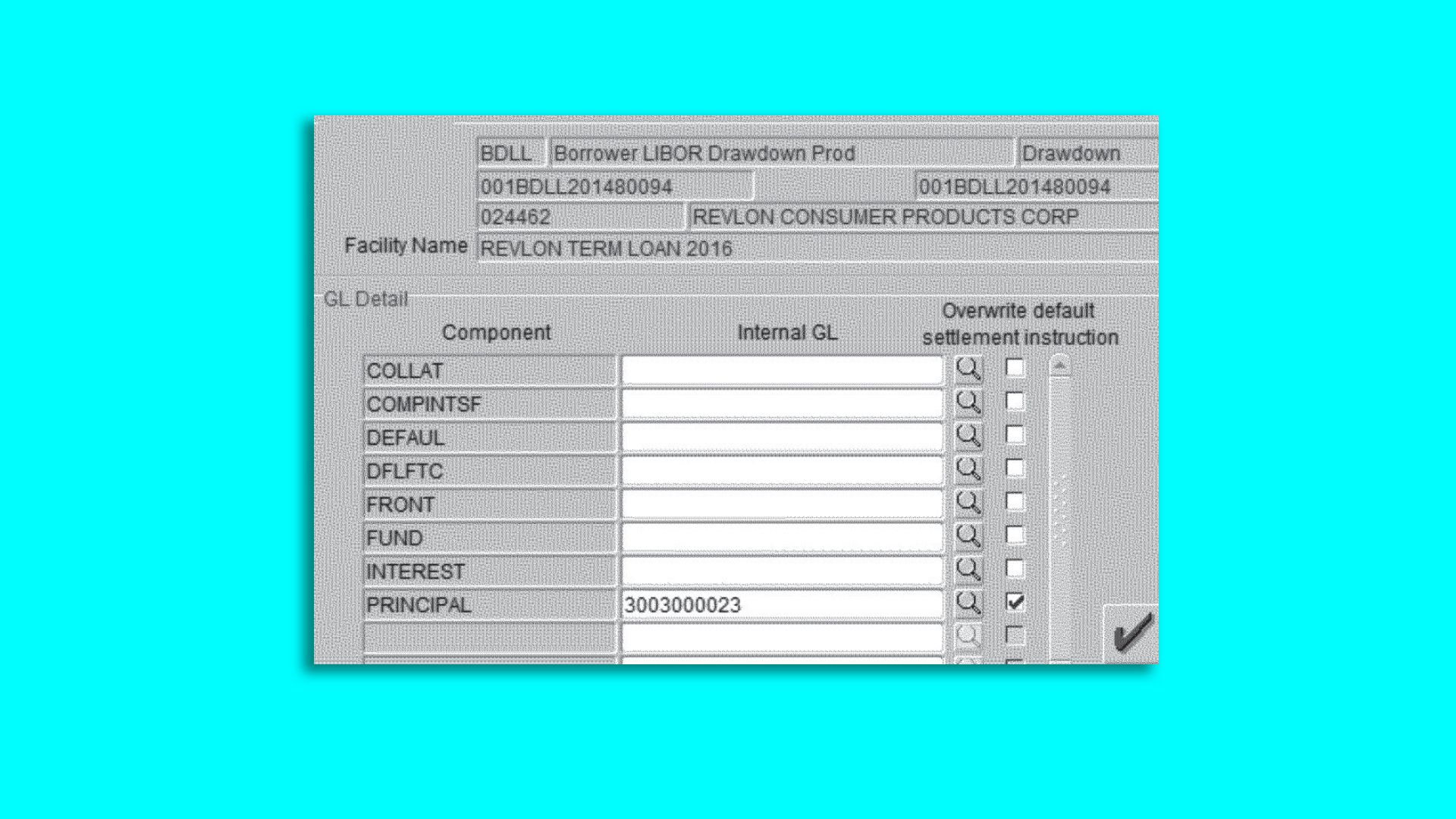

The judge's ruling sheds a lot of light on just how old and creaky Citibank's Flexcube payments infrastructure is.

- The software is incapable of sending principal and interest payments to just one creditor, as was intended in this case. Instead, it needs to be programmed to send principal and interest payments to all creditors, but with most of that principal diverted to an internal "wash account."

- The diversion to the internal account requires three different boxes to be ticked on this screen.

In reality, while the "principal" overwrite box was ticked, the "fund" and "front" boxes were not, which meant that the principal ended up leaving the bank.

The big picture: While the Federal Reserve has chided Citibank for its inadequate internal controls, no one has similar oversight over the Fed.

The bottom line: There's something wrong with America's payments infrastructure, which is still years away from the kind of real-time payments that are commonplace in countries from Sweden to India.

- Cryptocurrency is not the solution, however. As the Citibank and Fed stories demonstrate, mistakes will always happen. That means there has to be some kind of way to reverse transactions — something that remains impossible by design with most cryptocurrencies.

4. Confusing SPACs, Lucid edition

Illustration: Annelise Capossela/Axios

5. The gyrations of CCIV

At the beginning of this year, CCIV was valued at $10 per share, like most other SPACs — just the value of the cash it held.

- When rumors started circulating that CCIV was going to become Lucid Motors, the stock began to rise.

- At modest levels in the $10 to $15 range, that trade made a certain amount of sense.

- The logic: CCIV was probably going to get private equity companies to invest fresh money into Lucid, and private equity companies' valuation algorithms are generally more conservative than the stock market as a whole, when it comes to electric vehicles. So if PE was going to buy in at $10 per share, maybe it made sense to front-run the merger by buying CCIV at say $15 per share.

Things got out of hand, however, with CCIV stock trading at more than $60 per share before the valuation of the merger deal was announced. That price had no implied valuation for Lucid; it was simply a momentum trade that a stock that was rising sharply would continue to rise.

Once the valuation was announced, the stock fell to a magnificent level for Lucid shareholders but a disappointing level for anybody who had bought CCIV shares at the peak. The momentum trade was over, disgusted traders sold out of their positions, and that selling drove the price of the stock down even further.

The bottom line: Once the merger is finalized and CCIV starts trading under its new ticker symbol of LCID, it will be possible to look to the stock as a reflection of what's going on with the car company. For the time being, however, it's trading mostly on technical factors.

6. GameStop: It's back

¯\_(ツ)_/¯

7. Coming up: Buffett's annual letter

Photo: Ankit Agrawal/Mint via Getty Images

8. Building of the week: Stanley Mosk Courthouse

Photo: Frazer Harrison/Getty Images

Axios Capital

Learn about all the ways that money drives the world