Cost of car insurance in California spikes in 2024

Add Axios as your preferred source to

see more of our stories on Google.

The cost of car insurance in California has spiked this year, surpassing the national average, as rates increase across the U.S.

Why it matters: Fast-rising insurance rates are contributing to a transportation affordability crisis, especially in the many parts of the country where people have few alternatives to car ownership.

- And they come alongside all sorts of other rising consumer costs in recent years, like groceries.

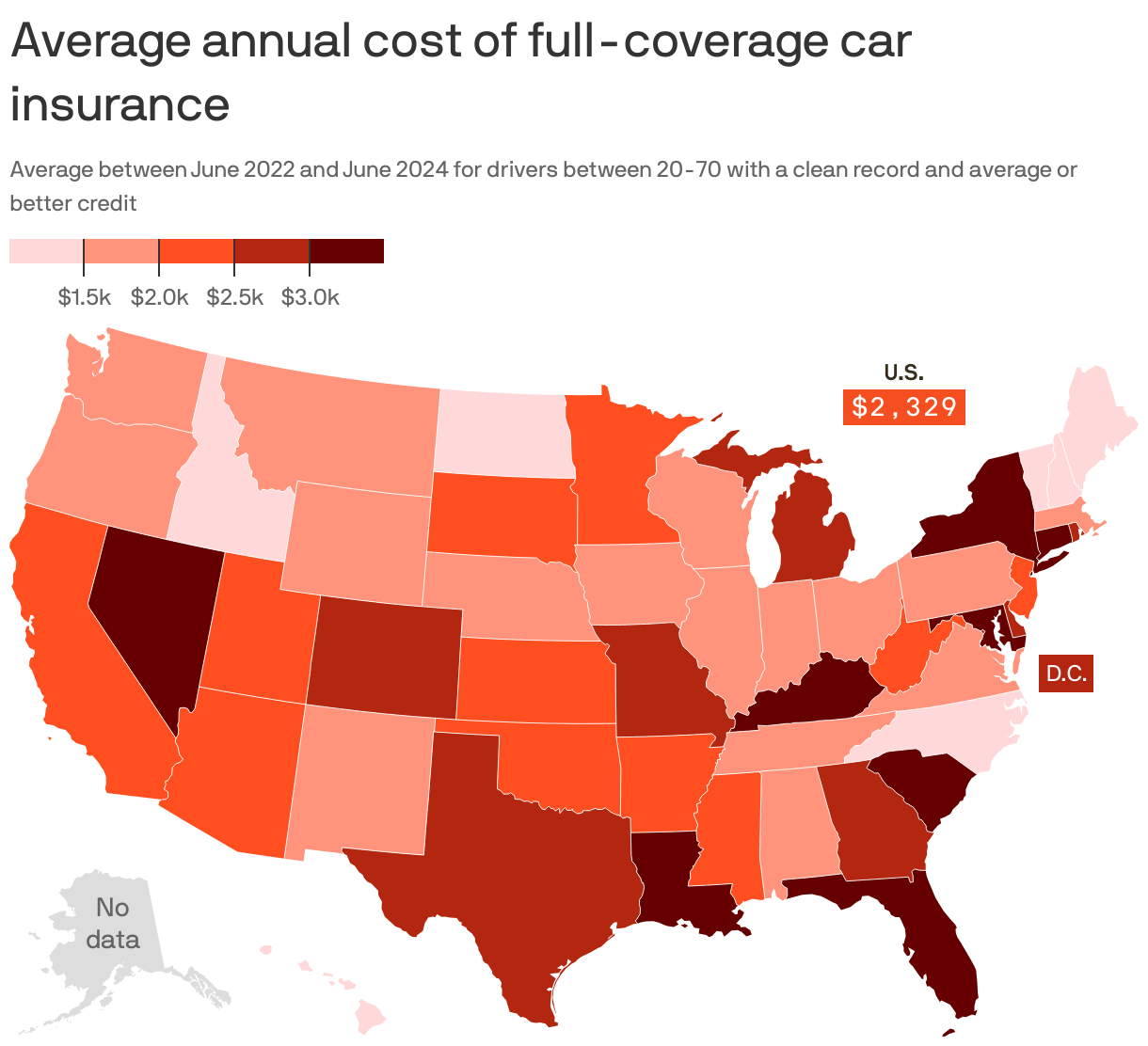

Driving the news: The nationwide average annual cost of full-coverage car insurance hit $2,329 in June, per Insurify, a digital insurance agent that helps users collect quotes from multiple insurers.

- That's up from $1,601 in January of 2021.

Zoom in: California car insurance rates rose from $1,738 in December 2023 to $2,417 in June 2024.

- That's a nearly 40% jump in six months.

What they're saying: "Rate increases this year are largely a continuation of hikes in 2023, a year that saw full-coverage premiums rise by 24% in response to insurers' record underwriting losses the year prior," Cassie Sheets, data journalist at Insurify, told Axios via email.

- "California froze insurance rates during the pandemic. To try and overcome substantial losses, some insurers are requesting double-digit rate hikes," she said.

Zoom out: Rates are highest in Connecticut ($3,598), Maryland ($3,400) and South Carolina ($3,336), while they're lowest in New Hampshire ($1,000), Maine ($1,209) and North Carolina ($1,403).

How it works: Insurify's monthly figures are two-year rolling medians to account for "extreme market volatilities" in recent years, the company says.

- And they're based on rates for drivers between ages 20-70 with clean driving records and at least average credit scores.

The big picture: Several factors play into the difference in rates between states, including road conditions, accident rates and whether a state requires no-fault coverage (meaning plans must cover medical expenses regardless of who's at fault in an incident).

- Individual people's quotes, meanwhile, also take into account their age, gender, driving record, etc.

The intrigue: Insurers are increasingly using data about people's actual driving behavior to inform their rates — sometimes with drivers' explicit knowledge and sometimes less so, per the New York Times.

- In March, General Motors quit sharing details about drivers' behavior with data brokers that worked with insurers to create "risk profiles" following the Times' reporting on the practice.

The bottom line: If you're looking to save on insurance, try shopping around — sometimes you're more likely to get a deal with a new provider.

- And if you're a homeowner, look into bundling your home and auto coverage to save on both.