Private equity lards on the debt in 2017

Add Axios as your preferred source to

see more of our stories on Google.

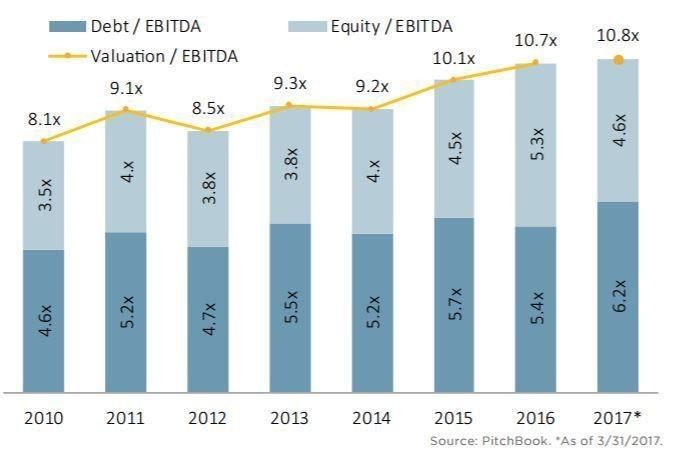

Private equity multiples breached Fed guidelines in Q1, according to new data published on Thursday by PitchBook. It shows debt-to-equity multiples hit a whopping 6.2x in Q1, compared to 5.4x for the entirety of last year and a 5.19x average between 2011 and 2016.

What the Fed says: Four years ago, America's central bank issues guidelines that debt-to-EBITDA ratios (for most industries) shouldn't exceed 6x.

What happened: For a while, most everyone played by these rules ― largely because banks were scared of crossing the Fed. Then a bunch of one-off transactions began breaching the threshold, particularly in tech. Then "baskets" of deals began to breach. All the while, the Fed did little more than send the occasional letter of reprimand. The takeaway for banks was: You can do it, just don't flout it.

Should the Fed care more? It's tough to argue that companies benefit from being over-leveraged but, from a public policy standpoint, private equity-backed deals don't pose a systemic risk. Namely because the failure of one PE portfolio company shouldn't impact the fortunes of another PE portfolio company, even if held in the same fund.

Caveat: It can be very difficult for data providers like PitchBook to accurately gauge market-wide leverage multiples, given that so many LBO values and debt breakdowns are kept private. Thus the average is prone to being weighted toward take-private transactions, which tend to be larger (and, historically, have higher leverage multiples). It's also worth noting that PitchBook also reported a mark in excess of 6x for Q1 2016, but the overall year settled much lower.